The WPJ

Commercial Real Estate News

France's Retail Property Market to Uptick in Q2

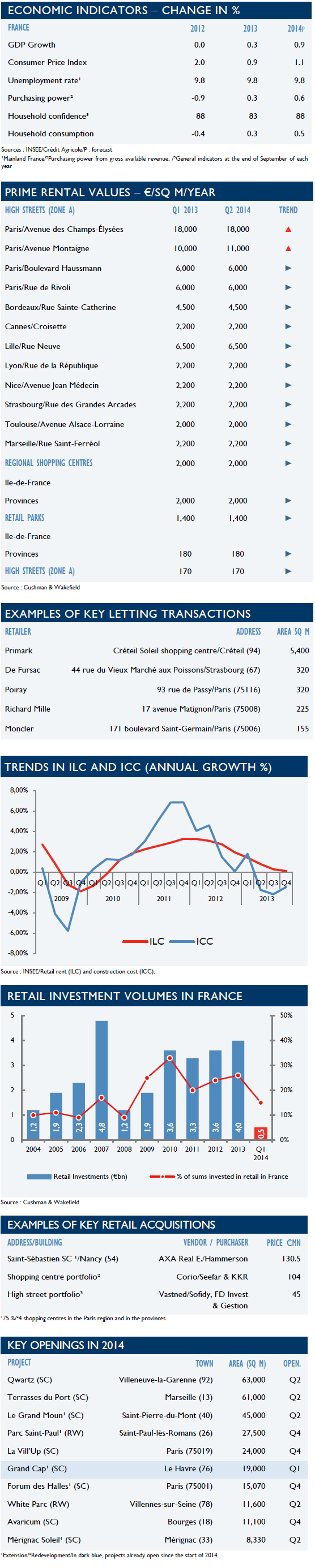

Cushman and Wakefield reports today that after a decline of 0.3% in Q1, France's consumer spending is expected to increase by 0.6% in Q2. While headline inflation is likely to be pushed upwards, consumer spending will be sustained thanks to a stable unemployment rate, a modest increase in purchasing power and a decline in savings.

In this context, several indicators reveal a retail market that is still in a recovery phase. Consumer spending on textiles and clothing items fell by 0.3% yoy but furniture sales grew by 1.2%. Winter sales figures are also mixed: although positive for the shopping center industry, they are generally disappointing for Parisian retailers.

The Rental Market

The Rental MarketCushman and Wakefield says the upturn in consumer spending will, however, not benefit the entire French retail real estate market in 2014. Secondary sites and retail units and developments that lack optimum configuration will, therefore, continue to suffer from retailers' wait-and-see stance.

Aware of the risks associated with opening new shops, some are slowing down their expansion or closing their poorer performing outlets. This trend explains the longer letting periods for certain sites and increased tenant incentives granted, in the context of the legal uncertainty due to the upcoming implementation of the Pinel law.

However, these risks have failed to deter many stakeholders from continuing their developments, thus demonstrating the potential of the French market in the eyes of large national groups developing new upmarket concepts (e.g., Minelli, Intersport) or foreign brands that have recently arrived in France (e.g., Primark, Aldo). The market also remains animated due to the continued arrival of new entrants in various sectors targeting different markets (e.g., Ecco, Rituals, Del Pozo), as well as variations of labels from well-known brands (e.g., H&M Home / Cheap Monday) and the continued rise of designer boutiques (e.g., Bellista / Nocibé, Lego, K-Way).

These various stakeholders tend to focus on the busiest or best known sites in France, be it the largest shopping centers - existing or newly created, or the best high-street locations in Paris and provincial towns. However, some medium-sized cities are also being targeted by big brands looking to boost their nationwide presence by opening franchises (e.g., Desigual, Fnac, and Darty).

The Investment Market

Cushman and Wakefield further reports that only â¬514 million was invested in the retail market in Q1 2014, half of that recorded over the same period in 2013 and with only two transactions greater than â¬100 million (acquisition by Hammerson of 75% of Saint-Sébastien shopping center in Nancy, purchase by KKR/Seefar of a portfolio of four centers). Although retail only represented 15% of total investment in France over the first quarter, in the coming months it is expected to reach levels closer to those of recent years (26% on average over the past five years). In fact, investment volumes will soon be boosted by the completed sale of regional shopping centers (Beaugrenelle) and large portfolios of mixed assets (Risanamento portfolio) and shopping centers (Klépierre portfolio).

French Retail Stock

880,000 m² of retail space was opened in 2013, which represents a slight decrease of 4% compared to 2012. This volume is expected to decrease in 2014 due to a sharp decline in retail park openings. The supply of shopping centers, on the other hand, will continue to renew at a fast rate despite the fact that few projects have opened since the start of the year - the most significant of which being the expansion of Grand Cap in Le Havre, a development showcasing restaurant chains and brands that are new to the local market (Shana, Calzedonia).

This trend of improving existing assets will continue in the coming months with the expansion of regional centers (Forum des Halles, Mérignac Soleil) as well as those of a smaller size. For example in 2014, Mercialys will complete ten extension-redevelopment projects totaling 25,000 sq. m. The most significant new-build projects will be announced in spring. After it is opened, Qwartz will become one of the largest French shopping centers and the first to feature Marks & Spencer and Primark under the same roof. Next to follow will be Les Terrasses du Port, an upmarket center intended to limit the retreat of commercial activity from Marseille's town center.

Current Legislation and Regulation

Following a cabinet reshuffle and the promise of major territorial reform, news on regulations remains highly topical. Published in the Journal Officiel on the 26th March 2014, the ALUR Law includes some important provisions, which force newly opened 'click & collect stores' to request authorization for commercial activity; require owners of vacant and unlet properties to refurbish if no letting takes place within three years; and limit the car parking ratios for retail properties.

That being said, Cushman and Wakefield comments that many issues are left outstanding such as evening and Sunday shop opening times, reform of commercial leases and changes to the law on urban retail planning. These last two issues are among the main elements of the Pinel Bill, which was passed by MPs in February and then referred to the Senate (extended short-term leases, ILC indexation, preferential right given to the tenant in the event of a sale of the premises, investigation of the CNAC for reviewing projects ⥠30,000 m², etc.).

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More