The WPJ

Featured Columnists

Vacation Investment Impacts U.S. Tax Returns

The allure of a 'home away from home' has enticed many expats to purchase a vacation home. And renting the home while you aren't there is certainly a nice way to earn a little extra money! But how does this property (and possible rental income) affect your U.S. income tax return?

What is a tax home?

First off, it's important to identify how the U.S. defines a 'home.' It is generally defined as a property that includes your basic living accommodations, such as sleeping quarters, cooking facilities and restrooms. For tax purposes, a home can be several different kinds of properties:

- Boat

- Mobile home

- Condominium

- House

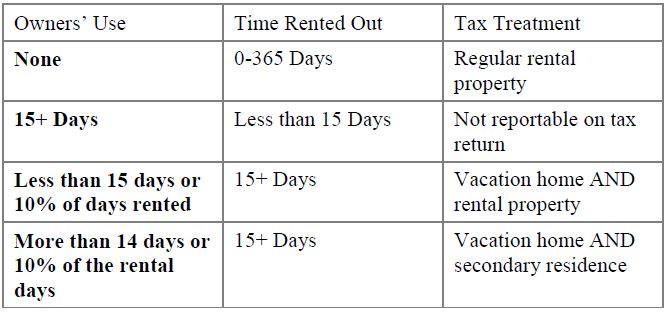

How your vacation home is classified for tax purposes makes all the difference when it comes to filing your U.S. income tax return. Here are the four possible classifications, which are based on the amount of time an owner uses the home and how much time the home is rented.

If you haven't actually purchased the home yet, there may be advantages to establishing a separate business structure under which you would manage this investment. There are many different types of structures to consider. Why is the classification important?

Simply put, how the property is classified will determine what expenses you can and cannot deduct on your tax return. If your property is a regular rental property, 100% of the home's activity must be reported on a U.S. income tax return. While all the income will be taxable, you can also take 100% of the allowable expenses as deductions to offset your tax. This may result in a net loss--it is recommended that you speak with a tax advisor in this situation, who can help you identify how much you can deduct on your individual tax return.

What if I rent my property less than 15 days a year?

This situation may be the most advantageous from a tax perspective. If you spend more than 15 days in the home yet rent it out less than 15 days, the rental income is not reportable on your tax return--that means it's tax-free income! In addition, the mortgage interest and real estate taxes are deductible (reported as an itemized deduction on your Schedule A). However, you should be aware that none of the operating expenses associated with this type of property would be deductible since there is no reportable income to offset. But that may only be a small drawback compared to the windfall of tax-free rental income!

What if I have rented my property more than 15 days this year?

This is a much more common situation, as expats often rent their vacation properties for larger portions of the year. If you have personally spent less than 15 days in the property and rented it out for more than 15 days, the property is classified as a vacation home used as a rental property. This makes your tax return a bit more complicated. The rental income earned would need to be reported on your tax return (on Schedule E) but all allowable deductions can also be taken. Expenses such as mortgage interest, depreciation and real estate taxes can be taken as deductions, but must be prorated based on the number of days the property was rented. If you paid management or advertising fees or did any repairs to the property, those expenses are 100% deductible against the rental income.

What are deductible expenses?

It may help to further clarify which expenses are deductible, and which ones aren't. Repairs to your property are deductible--think of repairs as work on your home that restores the property to its original state. Improvements, however, are not deductible. Improvements include work done on the property that increases its value and prolongs its life.

For example: A pipe bursts and results in water damage to the flooring in your kitchen. You repair the pipe and replace your flooring. This is a deductible expense as a repair. However, if you took this opportunity to replace all the appliances and cabinets while the flooring was ripped out, this is no longer deductible. This is considered an improvement that increases the value of your home. The cost would be capitalized and depreciated over a 27.5 year period.

What if I stay in the home more than 14 days and rent it out more than 14 days?

In this scenario, the home is considered a vacation home used as a residence. All rental activity is reportable on your tax return (on Schedule E) and any allowable deductions prorated based on number of days it was rented. Itemized deductions (such as mortgage interest and real estate taxes) can be taken on a Schedule A and any expenses associated with this property will be limited to the amount of rental income (i.e. no losses are allowable).

There are many things to consider when investing in a vacation home and making a decision to rent it out. The IRS is quite specific about the rules of vacation properties and you must take great care to understand the specific regulations that apply to your property's use. To maximize your tax breaks, spend as little time in the property as possible and carefully note the number of days you rent the property and the days you spend there. Finding the right balance is key--you can enjoy your vacation home and reap the tax benefits if you plan wisely!

David McKeegan is the co-founder of Greenback Expat Tax Services, a firm specializing in preparation of U.S. expat taxes for Americans living abroad.

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More