The WPJ

Commercial Real Estate News

Moscow's Office Vacancy Rates at Lowest Point Since 2014

Flexibility of landlords declines as new supply decelerates

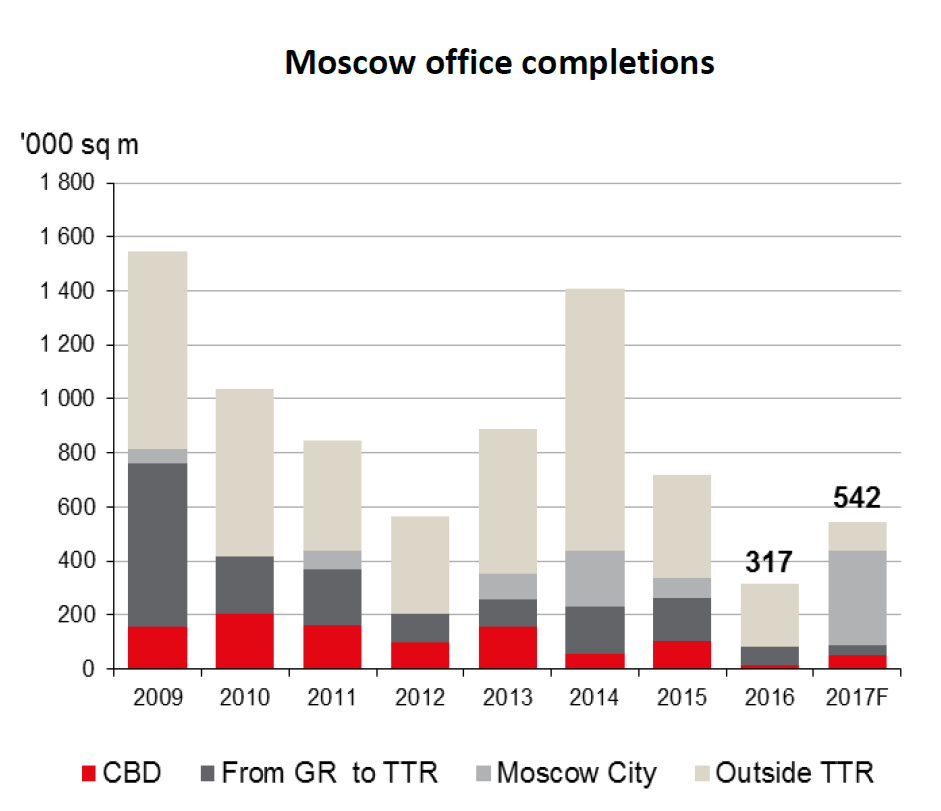

According to JLL, office completions in Moscow in Q1 2017 dropped to 21,143 square meters, 63% down Year-over-year. The delivery of 63,000 square meters of future office space was postponed.

Notwithstanding the delays, our 2017 completions forecast remains unchanged: the delivery of 542,000 sq. m in total is expected until the end of 2017, which will be 71% higher than the record low level of 2016. The delivery of 349,000 sq. m is expected in the Moscow City submarket (with no completion in 2016), and 65,000 sq. m is expected in the Central Business District (CBD), which will be five times higher than in 2016. Among the projects expected in 2017, we highlight Federation Tower East (205,000 sq. m) and IQ quarter (123,192 sq. m) in Moscow City, Oasis BC (29,000 sq. m) in the CBD and Fili Grad BC (25,500 sq. m) located outside the TTR.

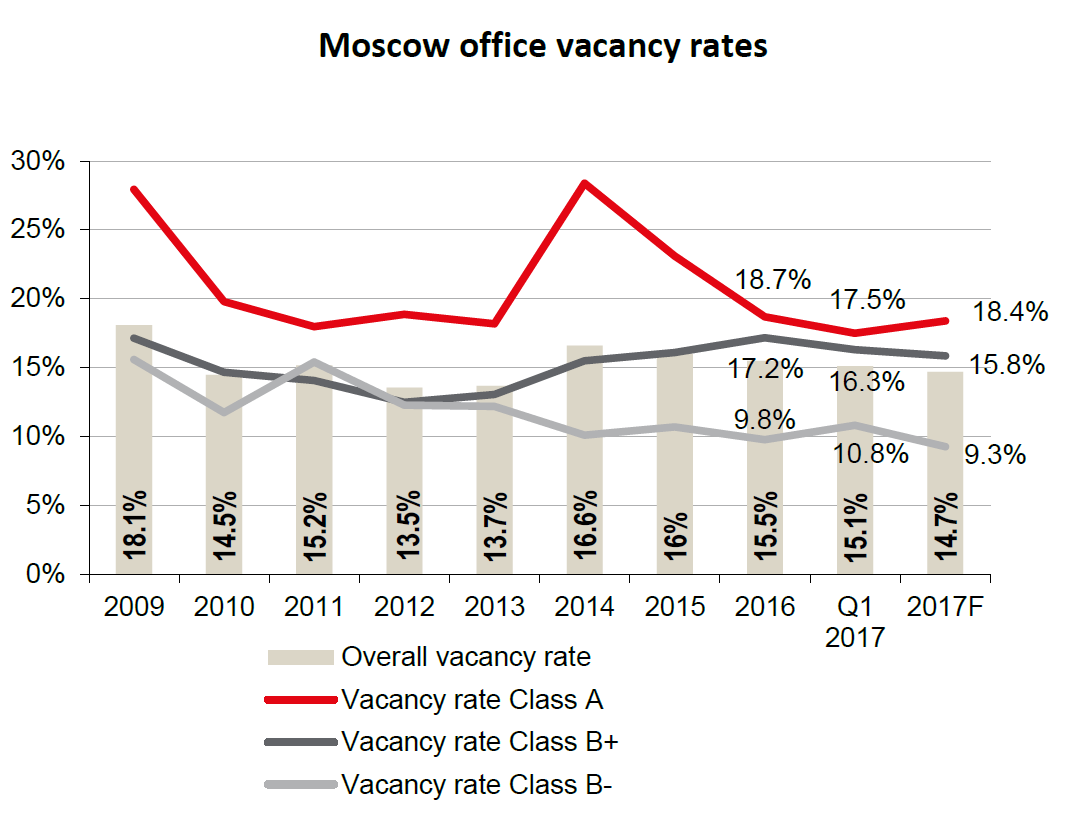

On the back of low developer activity, the vacancy rate continued to decline, to 15.1% in Q1 2017 (the lowest level since Q2 2014) from 15.5% in Q4 2016. The Class A vacancy rate shrank by 0.6 ppt and reached 17.5% from 18.1% in Q4 2016; the Class B+ vacancy rate declined by 1 ppt to 16.3%. On the contrary, the Class B- vacancy rate increased by 1 ppt QoQ to 10.8%.

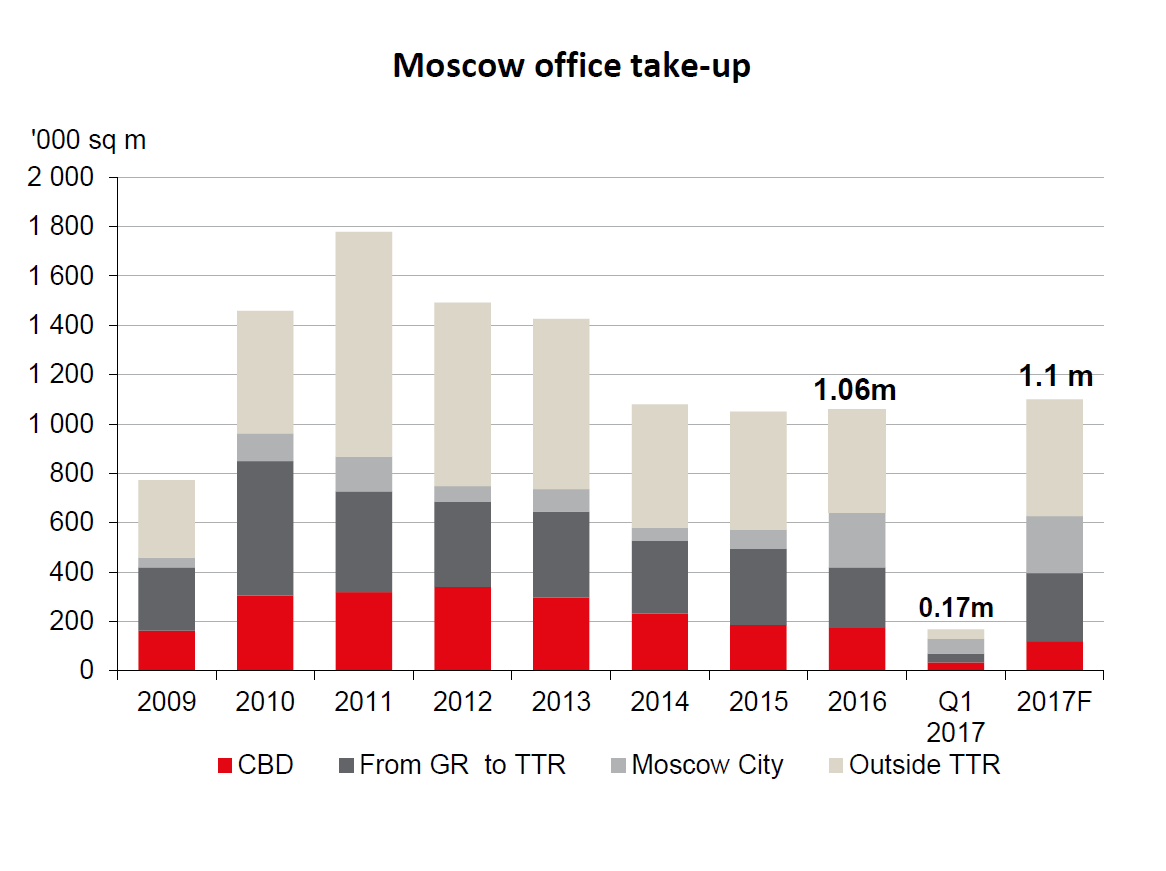

The Q1 2017, the take-up declined 37% YoY, to 167,000 sq. m. The demand structure has shifted in favor of new transactions, with a 73% share (compared to 44% in Q1 2016). The average deal size showed divergent trends: for new transaction it dropped to 1,000 sq. m from 2,400 sq. m in Q1 2016, whereas for renewal/renegotiation transactions it increased to about 3,000 sq. m from 2,700 sq. m.

According to JLL experts, these trends are the consequence of higher activity of large occupiers in 2012-2014, which are renegotiating the terms of their leasing agreements now. Smaller tenants are active in moving from low-quality offices to quality premises. These occupiers have a variety of options, as the premises of 1,500 sq. m and less comprise about 53% of the total market supply. The Q1 results should not be taken to imply the lack of activity of large occupiers. Several large transactions are on-going and are likely to be completed this year.

The demand for decentralized quality premises is still significant: 36% of the new leases (61,000 sq. m) have been signed in Class A objects outside the CBD. The occupier activity in the CBD has also picked up in Q1, to 22,400 sq. m compared to 6,900 sq. m in Q1 2016.

"Low new completions and stable rental rates attract growing tenant demand for quality premises. This lowers the flexibility of landlords and reduces the gap between asking and closing rental rates", says Elizaveta Golysheva, National Director, Head of Office Agency, JLL, Russia & CIS. Golysheva continued, "Asking rental rates in Q1 remained stable, with buildings offering rouble denominated leases with CPI annual indexation or fixed RUB indexation as the dominant type."

At the end of Q1 2017, asking prime rental rates were at USD600 - 750 /sq. m/year (or RUB33,000 - 42,000 /sq. m/year), Class A asking rents were at USD400 - 670 /sq. m/year (RUB22,000 - 38,000 /sq. m/year), and Class B+ at RUB2,000 - 20,000 /sq. m/year. Asking rents in Moscow City were at USD360 - 750 /sq. m/year (or RUB20,000 - 42,000 /sq. m/year). There were individual instances of increases in rental rates in certain locations, although such occurrences remain rare.

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More