The WPJ

Residential Real Estate News

U.S. Home Sales Soften Further in August, Says NAR

According to the National Association of Realtors, U.S. existing-home sales eased up in August 2016 for the second consecutive month despite mortgage rates near record lows as higher home prices and not enough inventory for sale kept some would-be buyers at bay. Only the Northeast region saw a monthly increase in closings in August, where inventory is currently more adequate.

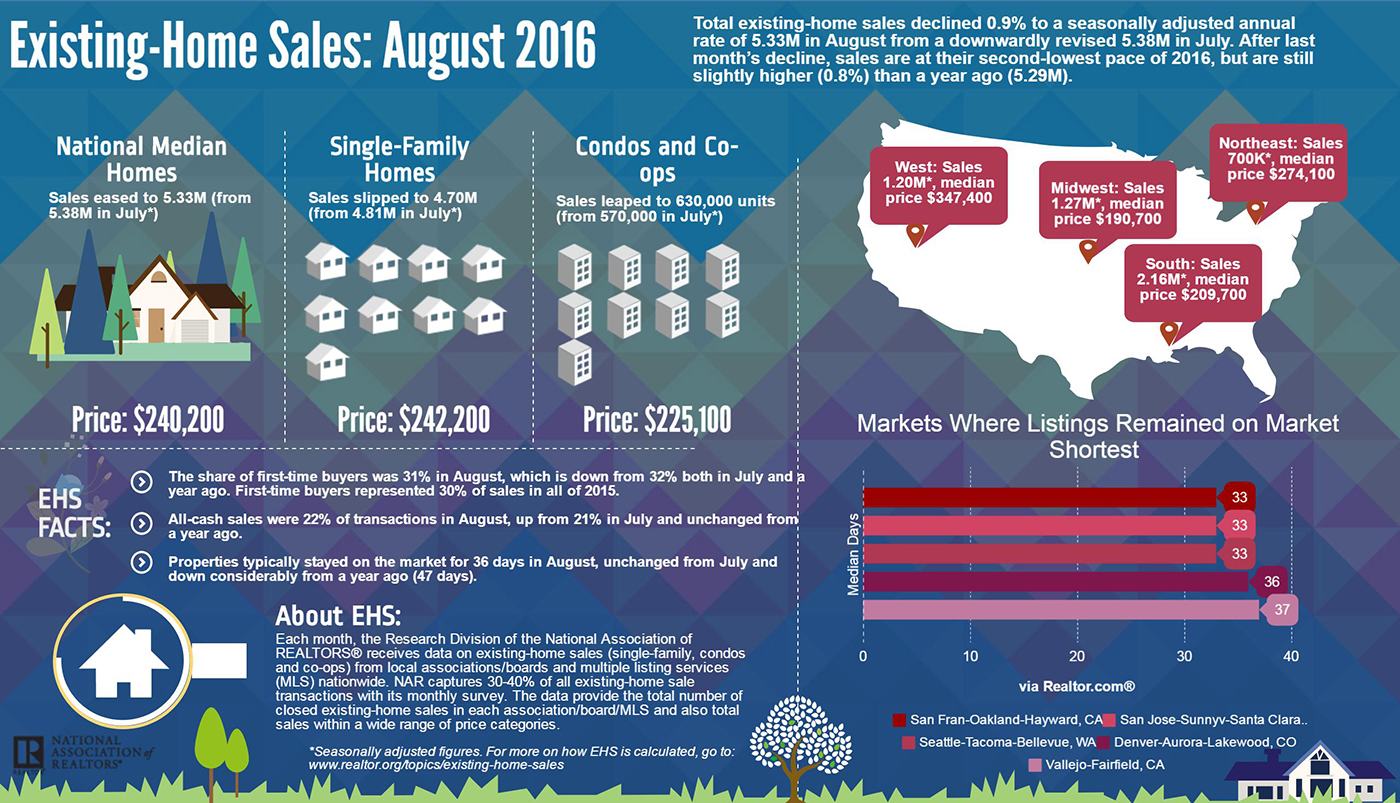

Total existing-home sales, which are completed transactions that include single-family homes, townhomes, condominiums and co-ops, declined 0.9 percent to a seasonally adjusted annual rate of 5.33 million in August from a downwardly revised 5.38 million in July. After last month's decline, sales are at their second-lowest pace of 2016, but are still slightly higher (0.8 percent) than a year ago (5.29 million).

Lawrence Yun, NAR chief economist, says recent job growth is not yielding higher home sales. "Healthy labor markets in most the country should be creating a sustained demand for home purchases," he said. "However, there's no question that after peaking in June, sales in a majority of the country have inched backwards because inventory isn't picking up to tame price growth and replace what's being quickly sold."

Added Yun, "Hopes of a meaningful sales breakthrough as a result of this summer's historically low mortgage rates failed to materialize because supply and affordability restrictions continue to keep too many would-be buyers on the sidelines."

The median existing-home price for all housing types in August was $240,200, up 5.1 percent from August 2015 ($228,500). August's price increase marks the 54th consecutive month of year-over-year gains.

Total housing inventory at the end of August fell 3.3 percent to 2.04 million existing homes available for sale, and is now 10.1 percent lower than a year ago (2.27 million) and has declined year-over-year for 15 straight months. Unsold inventory is at a 4.6-month supply at the current sales pace, which is down from 4.7 months in July.

The share of first-time buyers was 31 percent in August, which is down from 32 percent both in July and a year ago. First-time buyers represented 30 percent of sales in all of 2015.

"It's very concerning to see that inventory conditions not only show no signs of improving but have actually worsened in recent months from their already suppressed levels a year ago," added Yun. "While recent data from the U.S. Census Bureau shows that household incomes rose strongly last year, home prices are still outpacing incomes in many metro areas because of the persistent shortage of new and existing homes for sale. Without more supply, the U.S. homeownership rate will remain near 50-year lows."

According to Freddie Mac, the average commitment rate for a 30-year, conventional, fixed-rate mortgage was 3.44 percent in August for the second consecutive month and remained at its lowest rate since January 2013 (3.41 percent). The average commitment rate for all of 2015 was 3.85 percent.

Properties typically stayed on the market for 36 days in August, unchanged from July and down considerably from a year ago (47 days). Short sales were on the market the longest at a median of 144 days in August, while foreclosures sold in 42 days and non-distressed homes took 35 days. Forty-six percent of homes sold in August were on the market for less than a month.

Inventory data from Realtor.com reveals that the metropolitan statistical areas where listings stayed on the market the shortest amount of time in August were San Francisco-Oakland-Hayward, Calif., San Jose-Sunnyvale-Santa Clara, Calif., and Seattle-Tacoma-Bellevue, Wash., all at a median of 33 days; Denver-Aurora-Lakewood, Colo., 36 days; and Vallejo-Fairfield, Calif., at a median of 37 days.

All-cash sales were 22 percent of transactions in August, up from 21 percent in July and unchanged from a year ago. Individual investors, who account for many cash sales, purchased 13 percent of homes in August, up from 11 percent in July and 12 percent a year ago. Sixty-two percent of investors paid in cash in August.

Distressed sales - foreclosures and short sales - were 5 percent of sales in August (lowest since NAR began tracking in October 2008), unchanged from last month and down from 7 percent a year ago. Four percent of August sales were foreclosures and 1 percent were short sales. Foreclosures sold for an average discount of 12 percent below market value in August (18 percent in July), while short sales were discounted 14 percent (16 percent in July).

Single-family and Condo/Co-op Sales

Single-family home sales declined 2.3 percent to a seasonally adjusted annual rate of 4.70 million in August from 4.81 million in July, but are still 0.6 percent above the 4.67 million pace a year ago. The median existing single-family home price was $242,200 in August, up 5.3 percent from August 2015.

Existing condominium and co-op sales leaped 10.5 percent to a seasonally adjusted annual rate of 630,000 units in August from 570,000 in July, and are now 1.6 percent above August 2015 (620,000 units). The median existing condo price was $225,100 in August, which is 3.7 percent above a year ago.

Regional Breakdown

August existing-home sales in the Northeast jumped 6.1 percent to an annual rate of 700,000, which is unchanged from a year ago. The median price in the Northeast was $274,100, which is 0.8 percent above August 2015.

In the Midwest, existing-home sales decreased 0.8 percent to an annual rate of 1.27 million in August, but are still 0.8 percent above a year ago. The median price in the Midwest was $190,700, up 5.5 percent from a year ago.

Existing-home sales in the South in August fell 2.7 percent to an annual rate of 2.16 million, but are still 0.9 percent above August 2015. The median price in the South was $209,700, up 6.7 percent from a year ago.

Existing-home sales in the West lessened 1.6 percent to an annual rate of 1.20 million in August, but are still 0.8 percent higher than a year ago. The median price in the West was $347,400, which is 9.2 percent above August 2015.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More