The WPJ

Residential Real Estate News

3.6 Million Residential Properties in U.S. Remain in Negative Equity

Yet 548,000 U.S. Homeowners Regained Equity in Q2 of 2016

Irvine, Ca-based CoreLogic is reporting this week that 548,000 U.S. homeowners regained equity in Q2 2016 compared with the previous quarter, increasing the percentage of homes with positive equity to 92.9 percent of all mortgaged properties, or approximately 47.2 million homes. Nationwide, home equity grew year over year by $646 billion, representing an increase of 9.9 percent in Q2 2016 compared with Q2 2015.

In Q2 2016, the total number of mortgaged residential properties with negative equity stood at 3.6 million, or 7.1 percent of all homes with a mortgage. This is a decrease of 13.2 percent quarter over quarter from 4.2 million homes, or 8.2 percent, in Q1 2016 and a decrease of 19 percent year over year from 4.5 million homes, or 8.9 percent, compared with Q2 2015.

Negative equity, often referred to as "underwater" or "upside down," applies to borrowers who owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in home value, an increase in mortgage debt or a combination of both.

For homes in negative equity status, the national aggregate value of negative equity was $284 billion at the end of Q2 2016, decreasing approximately $20.4 billion, or 6.7 percent, from $305 billion in Q1 2016. On a year-over-year basis, the value of negative equity declined overall from $314 billion in Q2 2015, representing a decrease of 9.5 percent in 12 months.

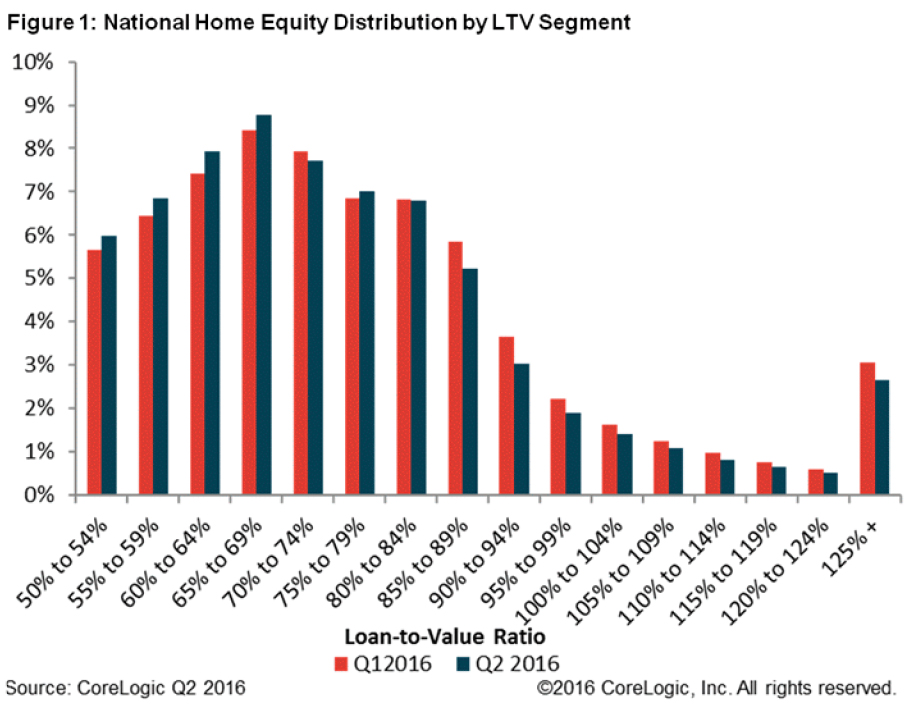

Of the more than 50 million homes with a mortgage, approximately 8.6 million, or 17 percent, have less than 20 percent equity (referred to as under-equitied) and approximately 965,000, or 1.9 percent, have less than 5 percent equity (referred to as near-negative equity). Borrowers who are under-equitied may have a difficult time refinancing their existing homes or obtaining new financing to sell and buy another home due to underwriting constraints. Borrowers with near-negative equity are considered at risk of shifting into negative equity if home prices fall.

"Home-value gains have played a large part in restoring home equity," said Dr. Frank Nothaft, chief economist for CoreLogic. "The CoreLogic Home Price Index for the U.S. recorded 5.2 percent growth in the year through June, an important reason that the number of owners with negative equity fell by 850,000 in the second quarter from a year earlier."

"We see home prices rising another 5 percent in the coming year based on the latest projected national CoreLogic Home Price Index," said Anand Nallathambi, president and CEO of CoreLogic. "Assuming this growth is uniform across the U.S., that should release an additional 700,000 homeowners from the scourge of negative equity."

U.S. Market Highlights as of Q2 2016:

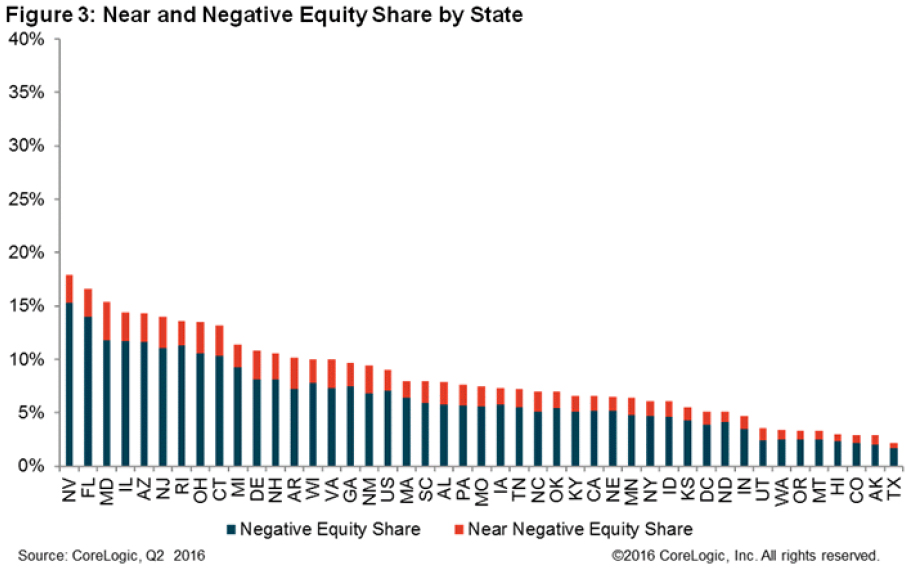

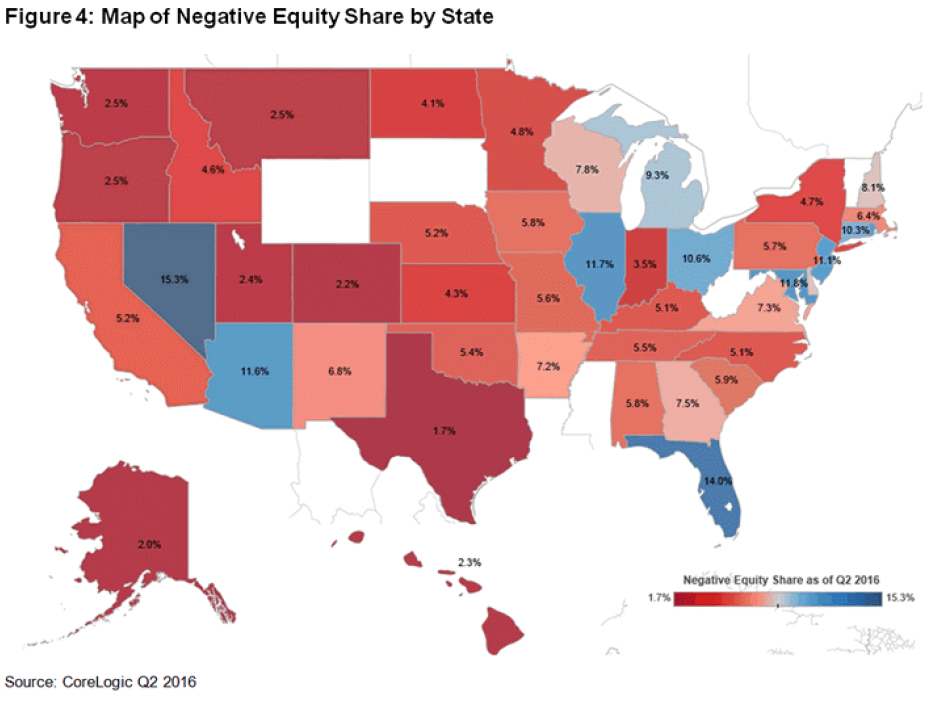

- Nevada had the highest percentage of mortgaged properties in negative equity at 15.3 percent, followed by Florida (14 percent), Maryland (11.8 percent), Illinois (11.7 percent) and Arizona (11.6 percent). These top five states combined accounted for 33.7 percent of negative equity in the U.S., but only 18.6 percent of outstanding mortgages.

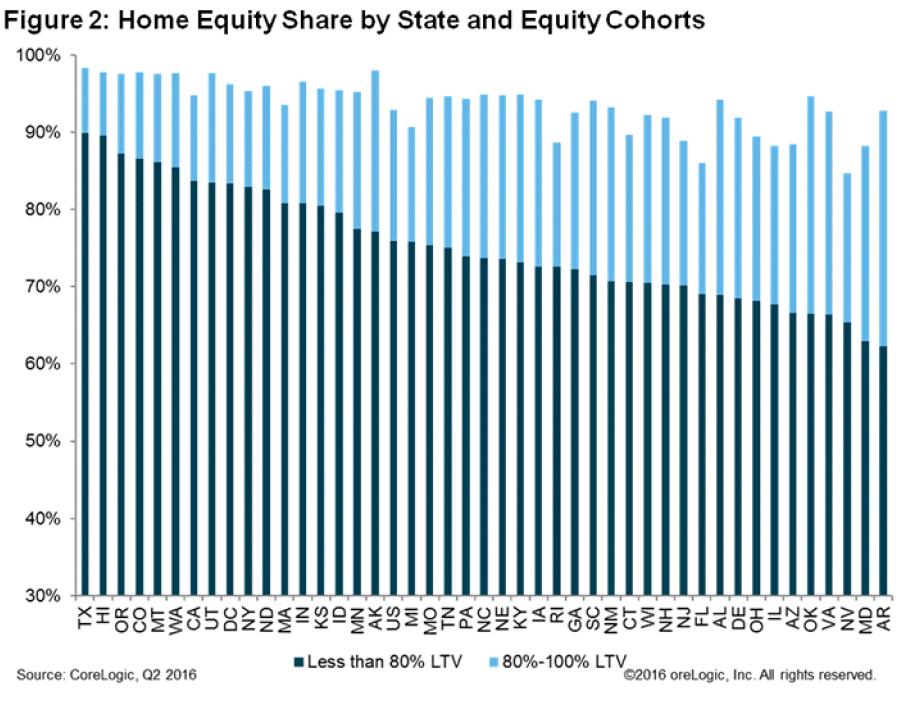

- Texas had the highest percentage of homes with positive equity at 98.3 percent, followed by Alaska (98 percent), Colorado (97.8 percent), Hawaii (97.7 percent) and Utah (97.6 percent).

- Of the 10 largest metropolitan areas by population, Miami-Miami Beach-Kendall, FL had the highest percentage of mortgaged properties in negative equity at 18.4 percent, followed by Las Vegas-Henderson-Paradise, NV (17.6 percent), Chicago-Naperville-Arlington Heights, IL (13.4 percent), Washington-Arlington-Alexandria, DC-VA-MD-WV (9.9 percent) and New York-Jersey City-White Plains, NY-NJ (5.9 percent).

- Of the same 10 largest metropolitan areas, San Francisco-Redwood City-South San Francisco, CA had the highest percentage of mortgaged properties in a positive equity position at 99.4 percent, followed by Denver-Aurora-Lakewood, CO (98.5 percent), Houston-The Woodlands-Sugar Land, TX (98.4 percent), Los Angeles-Long Beach-Glendale, CA (96.7 percent) and Boston, MA (95 percent).

- Of the total $284 billion in negative equity, first liens without home equity loans accounted for $159 billion aggregate negative equity, while first liens with home equity loans accounted for $125 billion.

- Among underwater borrowers, approximately 2.2 million hold first liens without home equity loans. The average mortgage balance for this group of borrowers is $252,000, and the average underwater amount is $73,000.

- Approximately 1.4 million of all underwater borrowers hold both first and second liens. The average mortgage balance for this group of borrowers is $314,000, and the average underwater amount is $88,000.

- The bulk of positive equity for mortgaged residential properties is concentrated at the high end of the housing market. For example, 96 percent of homes valued at $200,000 or more have equity compared with 89 percent of homes valued at less than $200,000.

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More