The WPJ

Residential Real Estate News

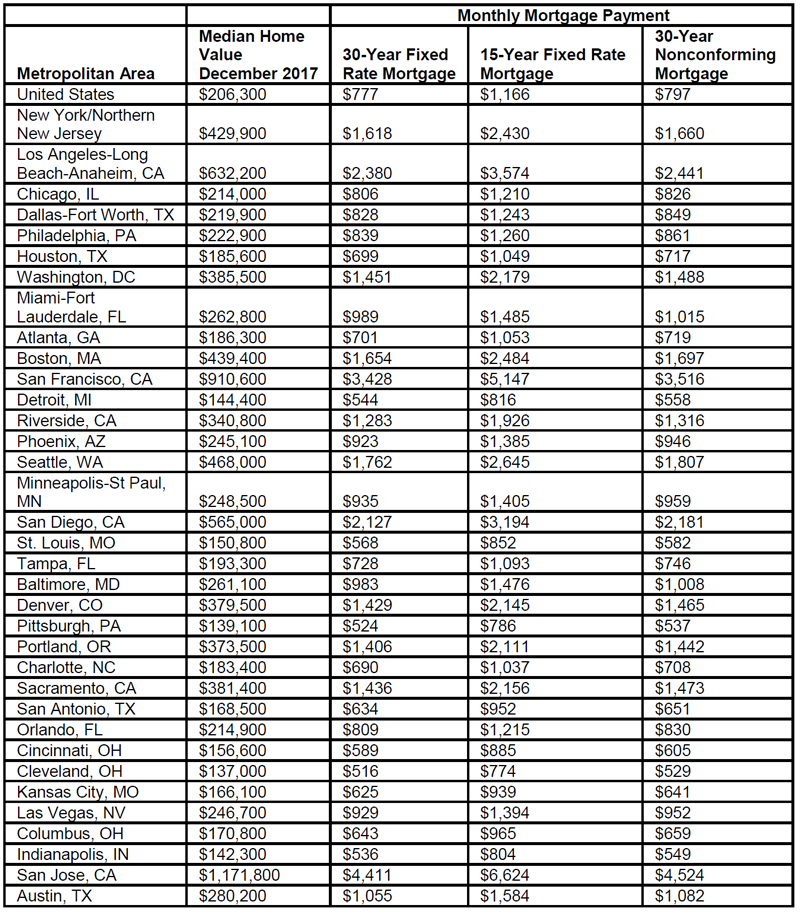

Changes to Freddie Mac, Fannie Mae Could Drive Mortgage Payments Up $400 a Month

According to Zillow, proposed reforms to the government-sponsored enterprises (GSEs) that guarantee the majority of U.S. home loans could drive up monthly housing costs and diminish housing affordability for many Americans.

Congress is considering changes to Fannie Mae and Freddie Mac to reduce the risk to taxpayers if the housing market crashes again. The GSEs, which guarantee a majority of all home loans against defaults, have been under government conservatorship since 2008, when they required more than $150 billion in taxpayer funds as a result of foreclosures during the housing crisis.

But a Zillow analysis shows that potential changes would cost borrowers as much as $400 a month in mortgage costs.

The guarantee from Fannie and Freddie is thought to keep interest rates for 30-year fixed-rate mortgages low, and housing relatively affordable. If that guarantee is changed, the typical American borrower could be facing shorter loan durations or higher rates. In this analysis, Zillow examined how alternatives to the traditional 30-year mortgage would affect borrowers' monthly costs, using current home values and mortgage rates.

- Shorter-term loans: The typical borrower would pay an additional $390 each month on the median U.S. home for a 15-year fixed-rate mortgage instead of a 30-year loan.

- Higher rates similar to current jumbo loans: A 30-year non-conforming loan would cost borrowers about $20 more per month for the typical U.S. home. Jumbo, or non-conforming, loans are currently not guaranteed by GSEs.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More