The WPJ

Residential Real Estate News

Miami, Moscow and Dubai to be Strongest Performing Global Markets in 2013

According to London-based Knight Frank, 2013 will be a year of continued growth in many prime cities around the globe despite continued economic uncertainty.

Since the Lehman Brother's collapse the world's luxury markets have come full circle. The global downturn meant luxury prices tumbled as market confidence ebbed away but within 12 months key markets such as London, Hong Kong and Shanghai were rallying once more recording prime quarterly price growth of 5.5%, 5.6% and 9.8% respectively.

In 2006 Knight Frank established the Prime Global Cities Index to measure the performance of luxury housing markets in some of the world's most important city markets. The index now stands 18.7% above its financial crisis low in Q2 2009. But it is the speed of the re-bound that is impressive; by Q1 2010 the index had regained its pre-crisis high.

2013 Highlights include:

- In 2013, expect prime residential prices across the 14 cities included in our forecast to rise by 2.5% on average, with Miami, Moscow and Dubai being the strongest performers.

- A sharp slowdown in the global economy is the highest risk for the world's prime residential markets closely followed by government cooling measures.

- However, the current economic uncertainty is also considered a key driver of demand in prime cities as HNWIs seek the shelter of 'safe-haven' investments.

- Supply, or the lack of it, will be a key determinant of price performance in cities such as New York, Moscow and Miami in 2013.

- Government-imposed regulatory measures will keep a lid on price growth in Asia in 2013 but the west-east shift in the economic balance of power suggests more promising prospects in the medium term.

Prime property has done more than just weather the economic storm and outperform its mainstream counterparts; it has prospered as a direct result of the uncertain economic climate. The protracted Eurozone debt debacle, the geopolitical tensions surrounding the Arab Spring and the absence of alternative strong-performing asset classes have heightened its appeal.

But aside from the climate of uncertainty, the rapid transition from 'crisis' to 'safe haven' was assisted by low interest rates, the preference amongst HNWIs for accessible and transparent markets and the unprecedented scale of wealth creation that was simultaneously occurring in the world's developing economies.

Between 2006 and 2011 the number of centamillionaires (those with disposable assets of $100m+) increased by 29% globally. The number of centa-millionaires in Latin America, South-East Asia and South-Central Asia rose by 67%, 80% and 200% respectively over the same period.

Cross-border investment flows have risen significantly as HNWIs in these emerging markets have looked beyond their national boundaries for double-digit annual returns. Miami has delivered for wealthy Brazilian, Venezuelan and Argentinean buyers while Dubai is the location of choice for an increasing number of Indian and Iranian HNWIs.

What will be trending in 2013?

In Knight Frank's 2012 Forecast we envisaged there would be three global trends that would be increasingly influential on the world's luxury residential markets; wealth creation, the growth of 'safe-haven' investments and the widening gap between East and West.

In 2013 Knight Frank expects a continuation of the same trends but currency movements will have an increasing bearing on the flow of wealth from city to city. Prime prices in New York have slipped 2.6% since 2008 but taking currency movements into account this translates into a 17.6% discount for Chinese buyers.

The search for unique "trophy" homes will gather pace in 2013 due in part to the increasingly high standard of new projects. Tall towers in the main gateway cities are already capturing the attention of an expanding number of HNWIs and we expect this trend to intensify.

In the coming year the world's wealthy will continue to micro-manage their property portfolios weighing up lifestyle gains against tax benefits and currency movements but central to most decisions will be price performance, both historic and forecast.

The forecast

Barring a collapse of the euro, the US toppling off its fiscal cliff or Asian protectionism being ramped up, the outlook for luxury homes in the world's key cities is one of quiet optimism.

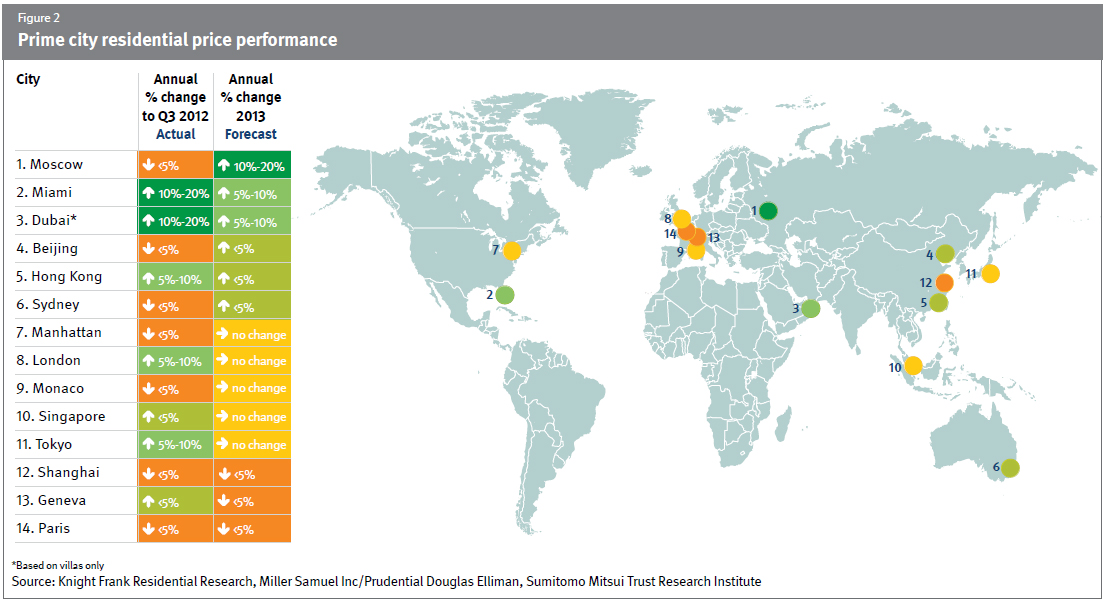

The Knight Frank forecasts shown in the map below represent our view as to where we consider prime prices are headed in 2013; for comparison purposes we have also shown each city's actual price performance in the year to September 2012. In 2013 we expect prime prices across the 14 cities surveyed to rise on average by 2.5%. In 2012 we predicted average price growth of 0.6%.

In 2013, we expect prices to rise or remain flat in eleven of the 14 cities included in our forecast. Moscow is expected to record the strongest price growth of all 14 cities (we forecast annual growth of 10%) due to tight prime supply and the expected release of a number of superprime projects.

Dubai provides another good news story; here we expect prices in the luxury villa market to rise by between 5% and 10% in 2013. The volume of enquiries from professionals relocating from the UK and Asia is rising while the supply of high quality family homes is largely static.

Prices are expected to fall in only three cities - Paris, Geneva and Shanghai - but in each case by less than 5%.

In Paris, the market has been sluggish in the second half of 2012 but we expect greater clarity to emerge in 2013 once President Hollande's austerity measures have bedded in. New development is still limited in markets such as Paris which may help sales absorptions in spite of political dampening measures.

Geneva has seen foreign demand fluctuate in 2012 and borrowing power has been affected by new lending legislation.

Shanghai meanwhile is set to see a continuation of the home purchase restrictions that came into force this year. This includes preventing single persons that are non-resident from buying property in the city.

In 2013 supply constraints are expected to be a determining factor for a number of cities. The shortage of top-end homes in Moscow and Miami is expected to support price growth. But in Monaco and New York although the lack of luxury homes is also evident there is not enough of an imbalance to drive prices significantly higher in 2013.

Mainstream housing market forecasts are arguably more straightforward than prime. By scrutinizing key indicators such as house prices to income ratios, house prices to rent ratios, interest rates and disposable incomes it is possible to gauge levels of affordability. The prime market however operates according to a different set of dynamics.

Instead, hard-to-quantify factors such as lifestyle, market confidence and the ease with which HNWIs can exit a market are often the critical factors under consideration. The current situation in Asia where markets are increasingly being controlled by government regulatory measures also make it harder to take a true reading of a prime markets' capacity for growth.

Measuring risk

While the forecasts we have presented represent what we believe to be the most likely outcome for 2013, there remains a number of derailing factors which have the potential to knock our forecasts off course.

With no solution to the ongoing crisis in the Eurozone on the horizon, it is no surprise that both global and domestic economic factors remain the biggest risk to property prices in 2013.

While international locations such as Geneva, Monaco, Dubai and Hong Kong rank the slowing global economy as the biggest risk, there are more insular concerns surrounding the health of domestic economies in the growth cities of Kuala Lumpur, Mumbai, Ho Chi Minh City and Sydney.

Government intervention has become increasingly important both in mature real estate markets, such as London and Paris, but also in rapidly expanding ones, such as Singapore where the government has recently introduced tighter measures for foreign workers and placed restrictions on home loans. Figure 4 provides a ranking of the degree of risk posed by the main cooling measures.

Further regulatory controls in prime cities around the world, most notably a 15% additional stamp duty for foreign buyers in Hong Kong and an increase in stamp duty for homes worth over £2m in the UK, could have an impact at the very top end of the market.

Interestingly, given their proximity to the problem and wider concerns about the health of the global economy, not one of the European cities surveyed ranked the Eurozone crisis as the highest risk adding further weight to the idea that prime locations have benefitted from their 'safe haven' status and continue to attract investment against the backdrop of sovereign debt concerns and geo-political uncertainty.

However, the lack of available finance, shrinking job markets and low consumer confidence in the region could weaken demand, even at the luxury end of the market.

Knight Frank has ranked interest rates, high inflation and low household income growth and the introduction of large scale housebuilding programs as low risks for the majority of locations.

Beyond the core risks examined above, there are countless factors such as currency fluctuations, tax changes and the revision of planning rules which could change the patterns of demand and supply in the world's prime markets. But the fundamentals are likely to remain unaltered; the supply of luxury homes is tight in most cities and global demand is rising exponentially.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More