Residential Real Estate News

Global Home Price Growth Slows to Lowest Levels Since 2015

Home prices worldwide under pressure as central banks attempt to rein in inflation

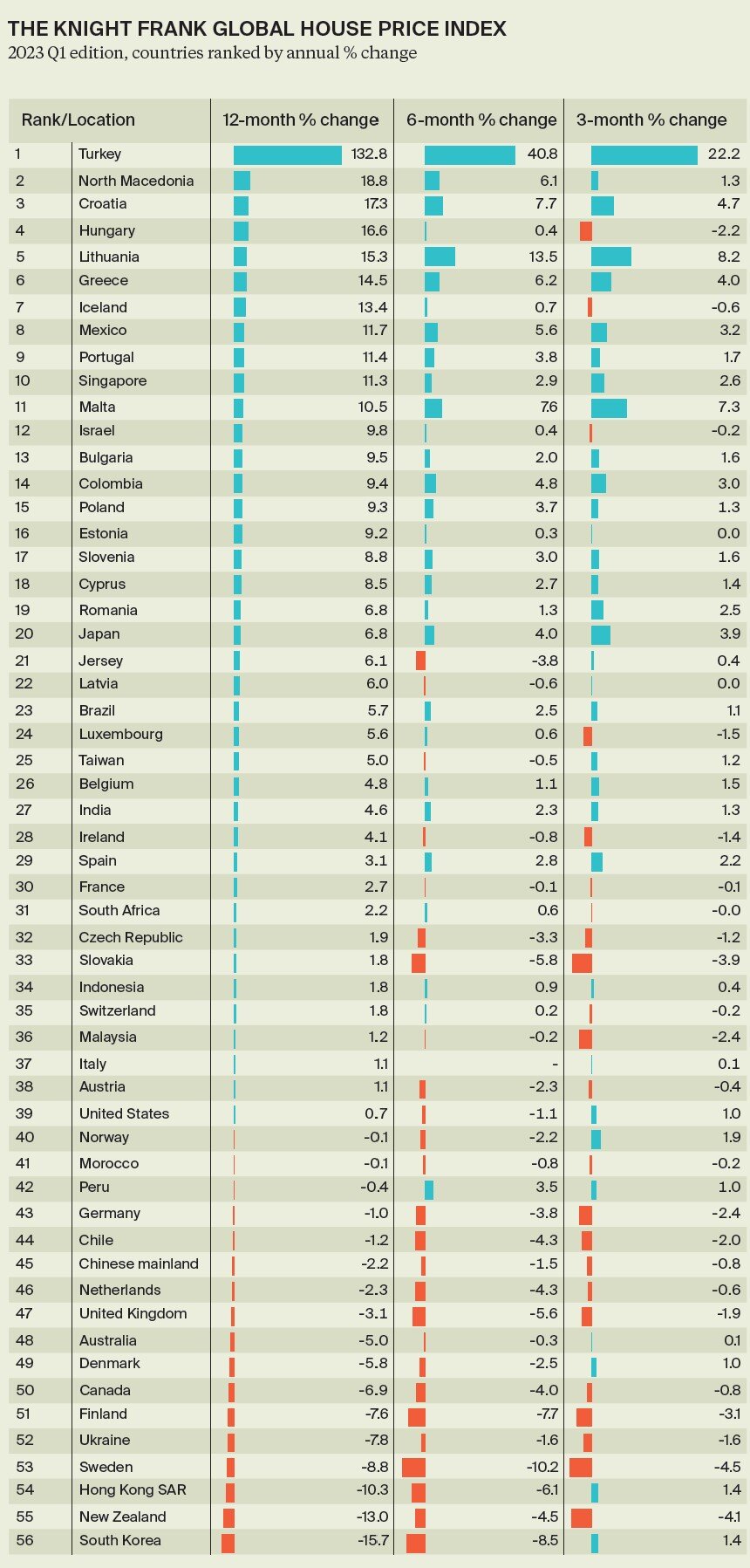

According to international property consultant Knight Frank, house prices across the world are under pressure as central banks attempt to rein in inflation. Average annual price growth across the 56 markets covered by the Knight Frank Global House Price Index slowed to 3.6% in the twelve months to Q1 2023, down from 5.7% in the previous quarter.

The index is rising at the slowest annual rate since the third quarter of 2015 and is down from a recent peak of 11.1% growth in the year to Q1 2022, when global markets were booming in the aftermath of the pandemic.

Of the 56 markets tracked, 17 recorded annualised price falls, eight of which saw a contraction of more than 5%. 23 of the markets covered saw prices fall over the most recent three-month period.

While the latest data reveals a substantial slowdown in annual price growth, quarterly growth improved. Global house prices contracted 0.6% in the final three months of 2022 yet saw a 1.5% rise in the first three months of 2023. On its own this reversal doesn't confirm that global markets are set to improve - rather, it does highlight that tight supply, limited new housing construction and strong household formation are acting to underpin prices in many markets.

Liam Bailey, global head of research at Knight Frank said, "While the latest data reveals a substantial slowdown in annual price growth, quarterly growth improved. Global house prices contracted 0.6% in the final three months of 2022 yet saw a 1.5% rise in the first three months of 2023. On its own, this reversal doesn't confirm that global markets are set to improve - rather, it does highlight that tight supply, limited new housing construction and strong household formation are acting to underpin prices in many markets."

MARKET LEVEL ANALYSIS

Turkey led the ranking again last quarter, but it's phenomenal growth of 132.8% is largely a consequence of rampant inflation. The recent move to a more orthodox approach to monetary policy is unlikely to lead to a rapid downward shift in inflationary pressures. A 22% quarterly rise in house prices there in Q1 suggests there is more to come this year.

Eastern and south-eastern European countries dominate the top of the rankings with North Macedonia (18.8%), Croatia (17.3%) and Hungary (16.6%) all showing strong annual growth.

Singapore is the standout performer in the Asia-Pacific region, with 11.3% annual growth. Recent changes to tax policy have mainly targeted overseas buyers to try to cool rising prices, though there were enough domestic buyers to push prices to new highs. The Urban Redevelopment Authority is releasing new sites for development as it seeks to increase housing supply.

US prices ticked up 1% in Q1. Supply is tight, which is underpinning price growth despite worsening affordability, particularly in the growth markets across the southeast and southwest states.

South Korea (-15.7%), New Zealand (-13%), Hong Kong (-10.3%) and Sweden (-8.8%) sit at the bottom of the table.

While substantial pressures remain due to rising debt costs, Hong Kong's market has begun to see a tentative revival, with positive quarterly growth of 1.4%. The late reopening of the economy after the Covid-19 pandemic limited overseas and mainland demand - which is now beginning to revive.

New Zealand has seen one of the biggest corrections in prices globally in this cycle. While prices are likely to fall further, the speed and depth of the correction suggest that an uptick in both demand and eventually prices will come earlier than in many other developed markets. ANZ Bank expects growth in both metrics before the end of the year.

MARKET OUTLOOK

While New Zealand may soon point to an exit route from the global housing slowdown, and the US is surprising on the upside, there are still several risks ahead for most markets. Inflation remains the main issue. Headline rates are falling in most locations, but core inflation remains stubbornly high in the UK, the US and Europe.

As several housing markets worldwide approach peak interest rates, the downward pivot may be further away than anticipated even a month or so ago. The first cuts in policy rates may be delayed to the second half of 2024 for several key markets, which would lower transactions and market liquidity for 12-months or more, concludes Knight Frank.