The WPJ

Residential Real Estate News

Pre-Coronavirus, U.S. Homeowners Enjoyed $6 Trillion Equity Gain Over Last Decade

Based on CoreLogic's latest Home Equity Report for the first quarter of 2020, U.S. homeowners with mortgages (which account for roughly 63% of all properties) have seen their equity increase by 6.5% year over year, representing a gain of $590 billion since the first quarter of 2019.

In the latter half of the first quarter of 2020, the coronavirus (COVID-19) began to spread across the country, with immediate economic impact not fully realized until the end of March. As the pandemic continued to unfold and shelter-in-place orders were extended, unemployment reached double digits within a few short weeks and left many homeowners scrambling to cover mortgage payments. However, home prices continued to rise, which added to borrower equity through March.

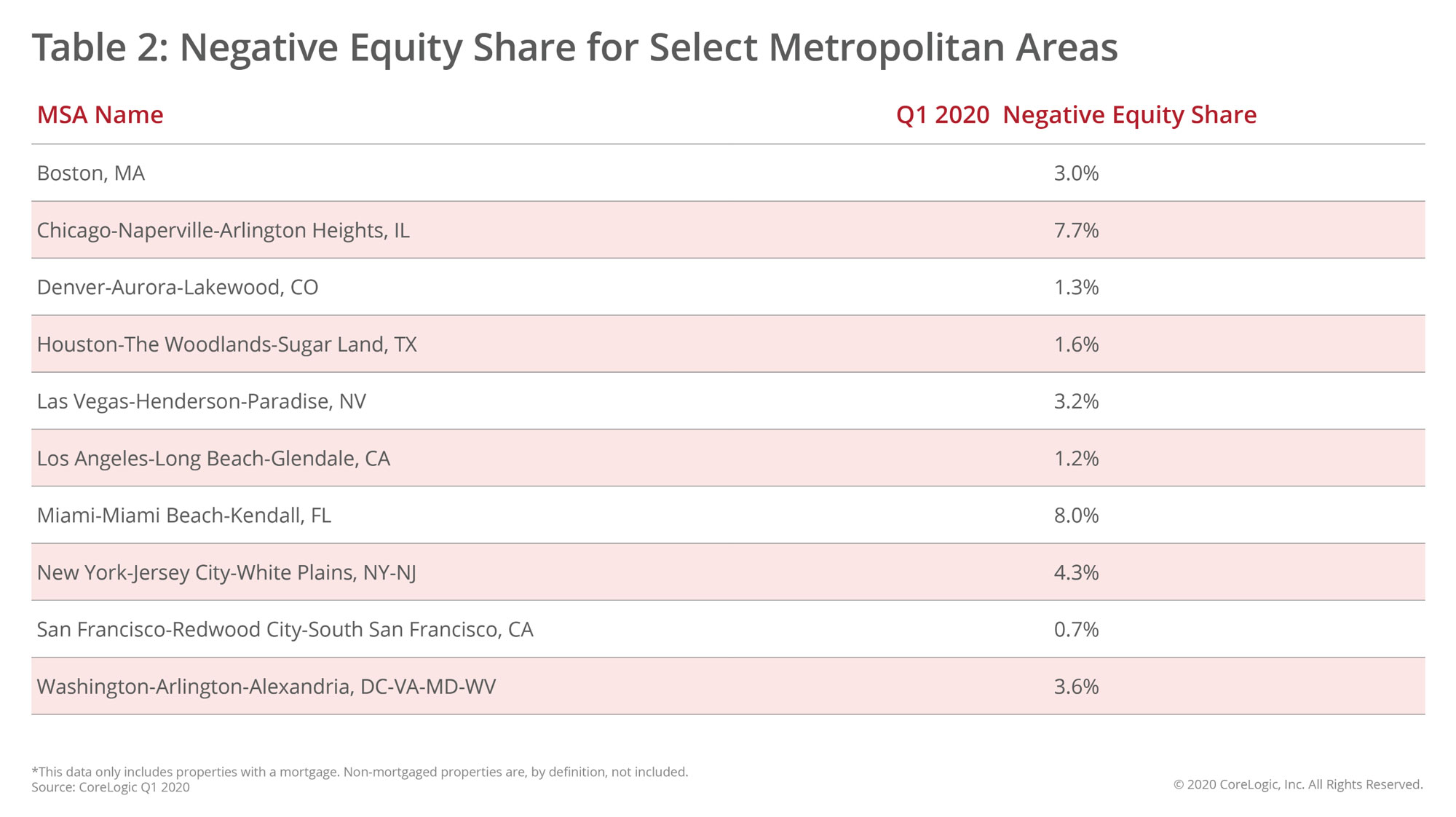

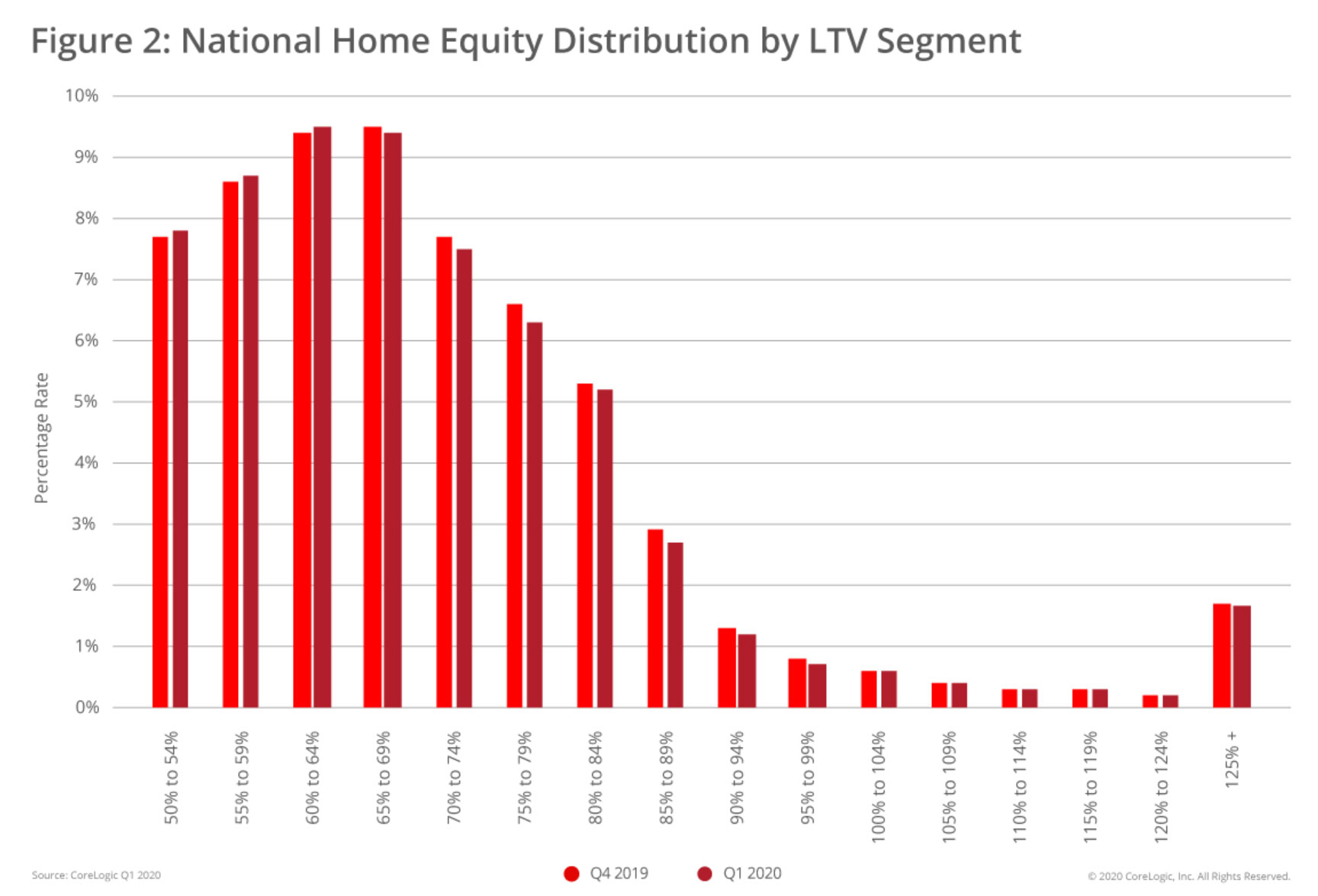

Negative equity, also referred to as underwater or upside down, applies to borrowers who owe more on their mortgages than their homes are worth. From the fourth quarter of 2019 to the first quarter of 2020, the total number of mortgaged homes in negative equity decreased by 3.1% to 1.8 million homes or 3.4% of all mortgaged properties. The number of mortgaged properties in negative equity in the first quarter of 2020 fell by 16%, compared to the first quarter of 2019, when 2.2 million homes, or 4.1% of all mortgaged properties, were in negative equity. Because home equity is affected by home price changes, the number of borrowers with equity positions near (+/-5%) the negative equity cutoff is most likely to move out of or into negative equity as prices change. Looking at the first quarter of 2020 book of mortgages, if home prices increase by 5%, 310,000 homes would regain equity, and if home prices decline by 5%, 420,000 would fall underwater.

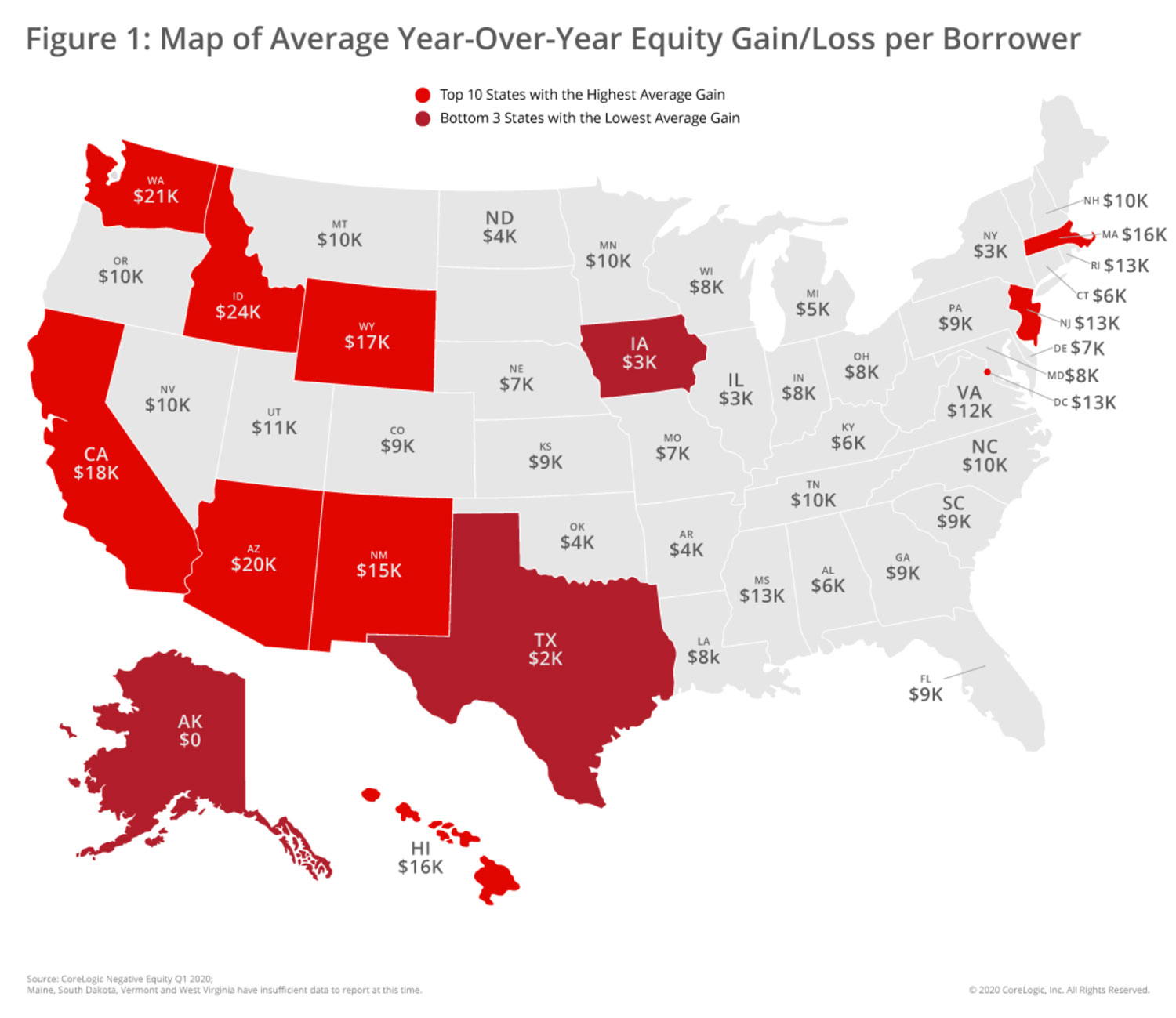

Homeowners gained an average of $9,300 in home equity between the first quarter of 2019 and the first quarter of 2020. States with the largest gains include Idaho, where homeowners gained an average of $24,400, Washington, where homeowners gained an average of $20,800 and Arizona, where homeowners gained an average of $19,900.

The national aggregate value of negative equity was approximately $284 billion at the end of the first quarter of 2020. This is down quarter over quarter by approximately $1.9 billion, or 0.7%, from $286 billion in the fourth quarter of 2019 and down year over year by approximately $22.6 billion, or 7.4%, from $307 billion in the first quarter of 2019.

"The pandemic recession will likely lead to price declines in many areas during the next year and weaken home equity gains," said Dr. Frank Nothaft, chief economist for CoreLogic. "However, price declines will be far less than those experienced during the Great Recession, when the national CoreLogic Home Price Index fell 33% peak-to-trough. Our latest forecast shows the national index to have a peak-to-trough decline of 1.5%."

"The pandemic recession will likely lead to price declines in many areas during the next year and weaken home equity gains," said Dr. Frank Nothaft, chief economist for CoreLogic. "However, price declines will be far less than those experienced during the Great Recession, when the national CoreLogic Home Price Index fell 33% peak-to-trough. Our latest forecast shows the national index to have a peak-to-trough decline of 1.5%."

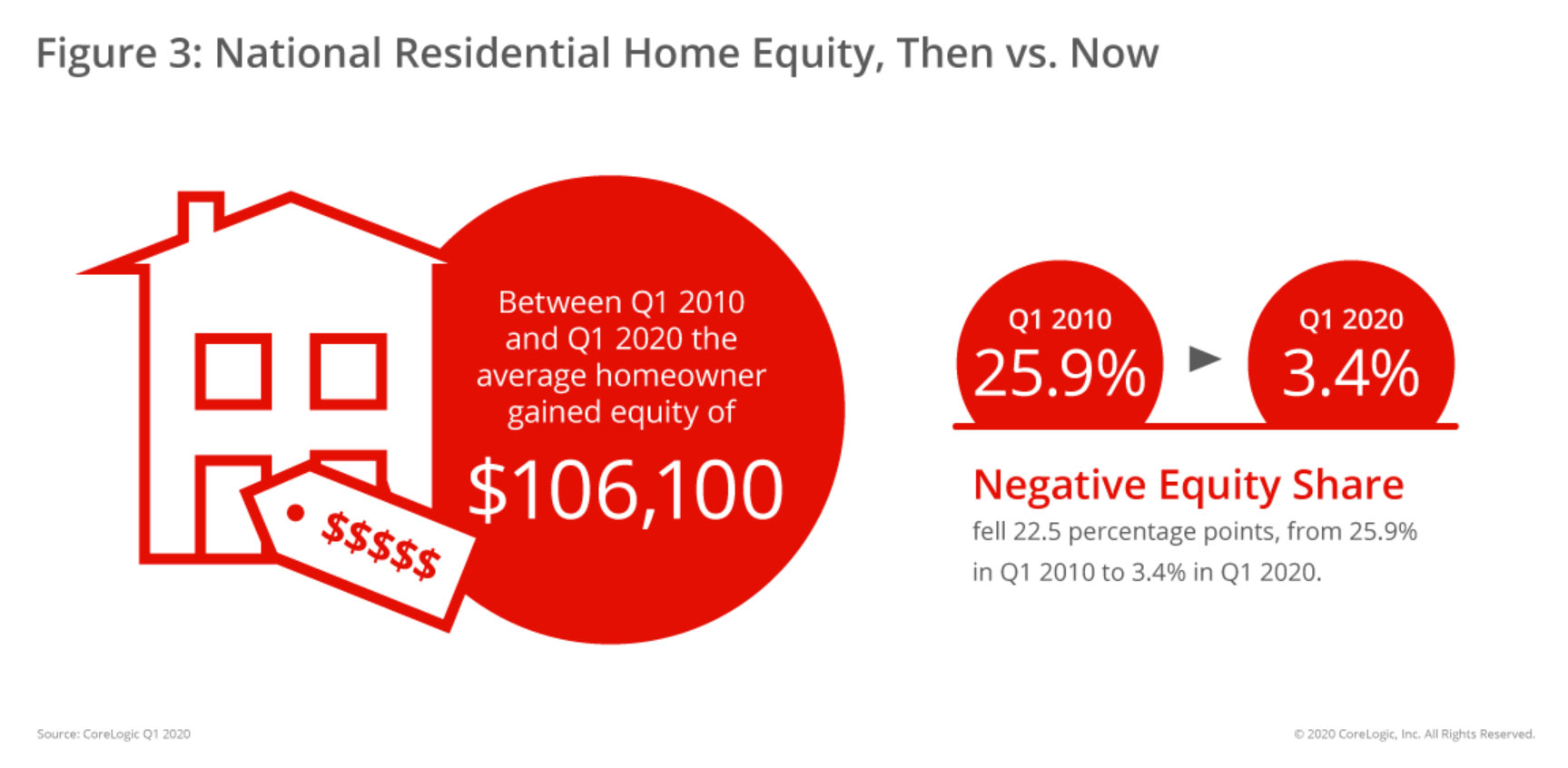

Over the past 10 years, the equity position of homeowners has positively changed as a result of more than eight years of rising home prices. As the economy climbed out of the recession in the first quarter of 2010, 25.9% or 12.1 million homes were still underwater, compared to the first quarter of 2020 when the negative equity share was at 3.4%, or 1.8 million properties. Borrowers have seen an aggregate increase of $6.2 trillion in home equity since the first quarter of 2010 and the average homeowner has gained about $106,100 in equity. Every state experienced a large reduction in the share of homes in negative equity, with Nevada posting the most significant drop in negative equity share, falling 70 percentage points between the first quarter of 2010 to the first quarter of 2020.

"Many homeowners will experience a recession during their lifetime, and it is reasonable to compare the current recession to those in the past," said Frank Martell, president and CEO of CoreLogic. "But the comparison is not apples to apples -- every recession is different. Primary drivers of the Great Recession were an overbuilt housing stock, risky mortgages and the collapse of home prices, creating a massive increase in negative equity that proved difficult to recover from. Today's housing environment has low vacancy and delinquency rates and a large home equity cushion. While the CoreLogic HPI forecasts a decline in home prices in the coming year, we can also expect the majority of homeowners to remain above water."

In the latter half of the first quarter of 2020, the coronavirus (COVID-19) began to spread across the country, with immediate economic impact not fully realized until the end of March. As the pandemic continued to unfold and shelter-in-place orders were extended, unemployment reached double digits within a few short weeks and left many homeowners scrambling to cover mortgage payments. However, home prices continued to rise, which added to borrower equity through March.

Negative equity, also referred to as underwater or upside down, applies to borrowers who owe more on their mortgages than their homes are worth. From the fourth quarter of 2019 to the first quarter of 2020, the total number of mortgaged homes in negative equity decreased by 3.1% to 1.8 million homes or 3.4% of all mortgaged properties. The number of mortgaged properties in negative equity in the first quarter of 2020 fell by 16%, compared to the first quarter of 2019, when 2.2 million homes, or 4.1% of all mortgaged properties, were in negative equity. Because home equity is affected by home price changes, the number of borrowers with equity positions near (+/-5%) the negative equity cutoff is most likely to move out of or into negative equity as prices change. Looking at the first quarter of 2020 book of mortgages, if home prices increase by 5%, 310,000 homes would regain equity, and if home prices decline by 5%, 420,000 would fall underwater.

Homeowners gained an average of $9,300 in home equity between the first quarter of 2019 and the first quarter of 2020. States with the largest gains include Idaho, where homeowners gained an average of $24,400, Washington, where homeowners gained an average of $20,800 and Arizona, where homeowners gained an average of $19,900.

The national aggregate value of negative equity was approximately $284 billion at the end of the first quarter of 2020. This is down quarter over quarter by approximately $1.9 billion, or 0.7%, from $286 billion in the fourth quarter of 2019 and down year over year by approximately $22.6 billion, or 7.4%, from $307 billion in the first quarter of 2019.

Dr. Frank Nothaft

Over the past 10 years, the equity position of homeowners has positively changed as a result of more than eight years of rising home prices. As the economy climbed out of the recession in the first quarter of 2010, 25.9% or 12.1 million homes were still underwater, compared to the first quarter of 2020 when the negative equity share was at 3.4%, or 1.8 million properties. Borrowers have seen an aggregate increase of $6.2 trillion in home equity since the first quarter of 2010 and the average homeowner has gained about $106,100 in equity. Every state experienced a large reduction in the share of homes in negative equity, with Nevada posting the most significant drop in negative equity share, falling 70 percentage points between the first quarter of 2010 to the first quarter of 2020.

"Many homeowners will experience a recession during their lifetime, and it is reasonable to compare the current recession to those in the past," said Frank Martell, president and CEO of CoreLogic. "But the comparison is not apples to apples -- every recession is different. Primary drivers of the Great Recession were an overbuilt housing stock, risky mortgages and the collapse of home prices, creating a massive increase in negative equity that proved difficult to recover from. Today's housing environment has low vacancy and delinquency rates and a large home equity cushion. While the CoreLogic HPI forecasts a decline in home prices in the coming year, we can also expect the majority of homeowners to remain above water."

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More