The WPJ

Residential Real Estate News

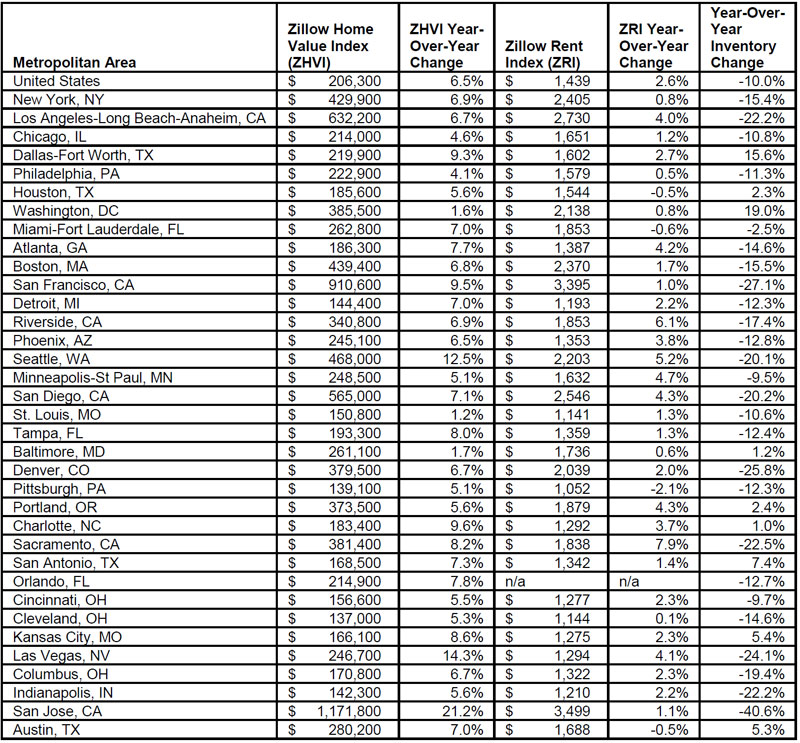

Inventory at Crisis Level in Many Top U.S. Housing Markets

According to Zillow's December 2017 Real Estate Market Report, U.S. home shoppers looking to buy in 2018 will have 10 percent fewer homes to choose from than a year ago.

For-sale inventory is stuck at crisis levels in some of the nation's hottest housing markets where home values are appreciating fastest. In San Jose, Calif., there are 41 percent fewer homes on the market than a year ago - the annual percentage change in inventory has been falling at a double-digit pace for the past nine months. In Las Vegas, the second fastest appreciating housing market, there are 27 percent fewer homes on the market than a year ago.

The number of homes for sale nationwide has declined on an annual basis for the past 35 straight months, and just 16.7 percent of a panel of housing experts surveyed in December 2017 expect a meaningful increase of home building in 2018, a sign that limited inventory could continue to drive the housing market this year.

"Tight inventory fueled by a tight labor market and low interest rates propelled home values to record heights in 2017, but the outlook is now much less certain," said Zillow senior economist Aaron Terrazas. "Tax reform will put more money in the pocket of the typical buyer, but will limit some housing-specific deductions. Overall, this should increase demand for the most affordable homes and ease competition somewhat in the priciest market segments. On the supply side, the market is starving for new homes, but it won't be easy for builders struggling with high and rising land, labor and lumber costs. Aging millennials and young families may be able to find more affordable new homes for sale this year, but they'll most likely be in further-flung suburbs with more grueling commutes to urban job centers."

Lack of inventory, coupled with strong demand from home buyers, is one reason why home values across the country are reaching new peaks. The median U.S. home value rose 6.5 percent over the past year to $206,300, the highest it has ever been.

San Jose, Las Vegas, and Seattle reported the greatest home value appreciation over the past year. In San Jose, the median home value rose 21 percent to a $1,171,800. In Las Vegas, home values rose 14 percent, and in Seattle, they rose 12.5 percent.

Median rent across the nation rose 2.6 percent since last December, the fastest pace of appreciation since June 2016, to a median payment of $1,439 per month. Sacramento, Calif.,Riverside, Calif., and Seattle reported the strongest rent growth over the past year.

In Sacramento, rents rose almost 8 percent to a Zillow Rent Index of $1,838. Median rent in Riverside rose 6 percent over the past year, and in Seattle, rents rose 5 percent. This is the sixth month in row that Sacramento has led the nation in rent appreciation, having taken the top spot from Seattle in August 2017. Though still toward the top of the national rankings, Seattle reported its slowest rent appreciation in almost three years.

Mortgages rates on Zillow ended the month of December at 3.75 percent. The month high of 3.82 percent was hit during the last week of the month, and the low of 3.70 percent was hit during the first week of the month. Zillow's real-time mortgage rates are based on thousands of custom mortgage quotes submitted daily to anonymous borrowers on the Zillow Mortgages site and reflect the most recent changes in the market.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More