Residential Real Estate News

U.S. Mortgage Rates Rise Sharply Late September

The National Association of Realtors Senior Economist and Director of Forecasting, Nadia Evangelou, is reporting that U.S. mortgage rates rose sharply this past week following the trend of the 10-year Treasury yield. Specifically, according to the finance mortgage provider Freddie Mac, the 30-year fixed mortgage rate rose to 3.01% from 2.88% the previous week.

While rates were below 3% for the last nearly four months, it seems that rates at the 2% range are likely over. Inflation has risen above the 2% target since April 2021.

Nevertheless, rates were still near record lows as investors expected inflation to rise faster due to lower prices a year earlier. Meanwhile, the Fed recently pushed up its inflation estimates for this year, as inflation will likely be around for longer. The "grace" period for higher inflation seems to be coming to an end as the Fed may also raise interest rates by the middle of next year.

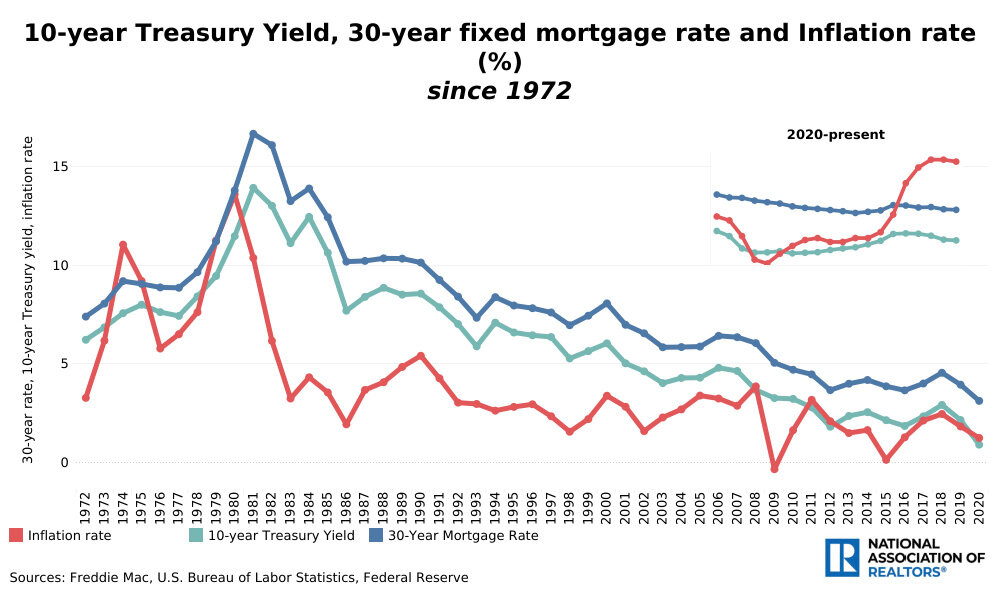

History shows us that rising inflation causes the 10-year Treasury yield to drift up as investors buy stocks instead of bonds. Particularly, higher inflation erodes the return that the investor of a bond or loan is holding over time and bonds are not any more attractive to investors. This in turn makes bond values go down and yields rise.

Consequently, mortgage rates move upward as they are tied to the 10-year Treasury yield. The relationship between inflation, the 10-year Treasury yield, and mortgage rates is shown clearly in the graph below. It's obvious that all these three indicators move roughly together.

Evangelou says consumers shouldn't panic. She reminds us that even though rates will increase in the following months, these rates will still be historically low. The National Association of Realtors forecasts the 30-year fixed mortgage rate to reach 3.5% by mid-2022.

Finally, remember that mortgages don't adjust for inflation. Thus, fixed-rate mortgage holders may even benefit from higher inflation since they are paying back money at a lower value than it was borrowed. To put it simply, homeowners will pay back less for their loan, concludes Evangelou.