The WPJ

Residential Real Estate News

Negative Equity Declines in 2Q, 8 Million Upside Down Owners Have Above Market Mortgage Rates

According to CoreLogic's negative equity data for 2Q, 2011, over 10.9 million, or 22.5 percent, of all residential properties in the U.S. with a mortgage were in negative equity at the end of the second quarter of 2011, down very slightly from 22.7 percent in the first quarter.

According to CoreLogic's negative equity data for 2Q, 2011, over 10.9 million, or 22.5 percent, of all residential properties in the U.S. with a mortgage were in negative equity at the end of the second quarter of 2011, down very slightly from 22.7 percent in the first quarter.An additional 2.4 million borrowers had less than five percent equity, referred to as near-negative equity, in the second quarter. Together, negative equity and near-negative equity mortgages accounted for 27.5 percent of all residential properties with a mortgage nationwide. The new report also shows that nearly three-quarters of homeowners in negative equity situations are also paying higher, above-market interest on their mortgages.

Negative equity, often referred to as "underwater" or "upside down," means that borrowers owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in value, an increase in mortgage debt or a combination of both.

Report Highlights Include:

- Nevada had the highest negative equity percentage with 60 percent of all of its mortgaged properties underwater, followed by Arizona (49 percent), Florida (45 percent), Michigan (36 percent) and California (30 percent) (Figure 2).

- The negative equity share in the hardest hit states has improved. Over the past year, the average negative equity share for the top five states has declined from 41 percent to 38 percent. Nevada had the largest decline over the last year, with the negative equity share dropping from 68 percent to 60 percent. The reason for the Nevada decline is the high number of foreclosures that led to lower numbers of remaining negative equity borrowers.

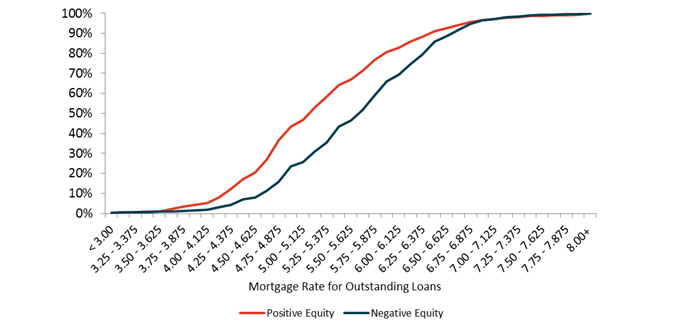

- Negative equity significantly limits the ability of borrowers to capture the benefit of the low-rate environment. There are nearly 28 million outstanding mortgages that have above market rates and are in theory refinanceable. Twenty million borrowers with positive equity, or 53 percent of all above-water borrowers, have above market rates. Eight million borrowers with negative equity, or nearly 75 percent of all underwater borrowers, have above market rates (Figures 3 & 4). The disparity is even greater for those with severe negative equity. More than 40 percent of borrowers with 125 percent or higher loan-to-value (LTV) ratios have mortgages with rates at 6 percent or above, compared to only 17 percent for borrowers with positive equity.

- Negative equity not only restricts refinancing, but also sales. Since the 2005 sales peak, non-distressed sales in zip codes with low negative equity have fallen 61 percent, compared to an 83 percent sales decline in high negative equity zip codes[1]. The typical seasonal changes in sales volume in high negative equity zip codes is very muted, which indicates that non-distressed sales are being heavily impacted by the high levels of negative equity in their neighborhood, even if sellers have equity.

- The federal homebuyer tax credit that expired last year contributed to a spike in high LTV loans (Figure 6). As the housing market collapsed, underwriting began to tighten in 2008 and the share of high LTV loans (90 percent to 100 percent LTV) began to decline. However, the federal homebuyer tax credit helped propel home sales in 2009 and 2010 and led to minor spikes in high LTV FHA lending centered near the expiration of the tax credit initially in November 2009, which was then extended to April 2010. In the span of six months in 2009, the high LTV share increased from 13 percent to 18 percent, which is large given such a small time period.

"High negative equity is holding back refinancing and sales activity and is a major impediment to the housing market recovery. The hardest hit markets have improved over the last year, primarily as a result of foreclosures. But nationally, the level of mortgage debt remains high relative to home prices," said Mark Fleming, chief economist with CoreLogic.

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More