The WPJ

Commercial Real Estate News

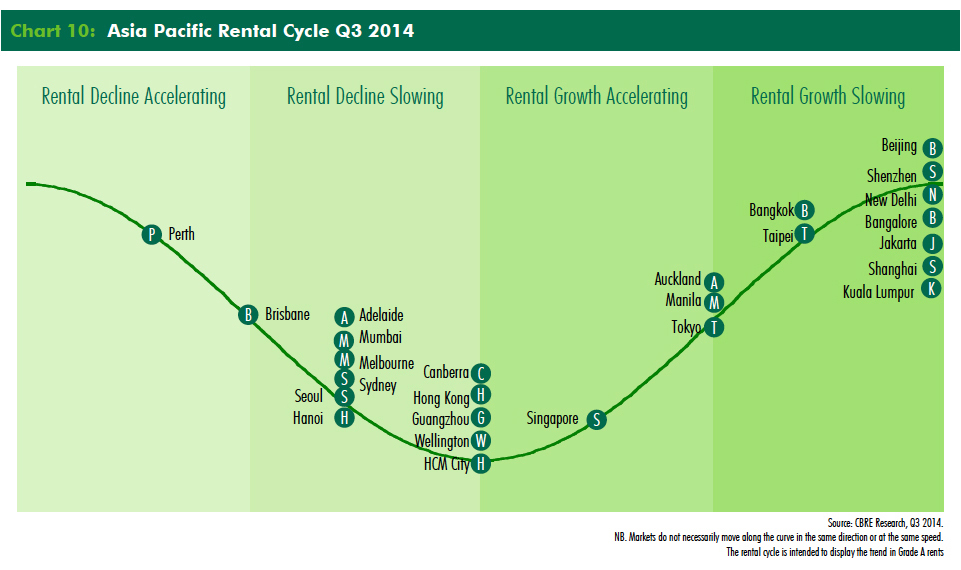

Asia Pacific Office Market Post Gains in Q3, Singapore Top Performer

According to a new regional office market report by CBRE, office leasing momentum generally remained steady across the Asia-Pacific (APAC) region in Q3, 2014.

CBRE's APAC Office Rental Index increased by 0.93% quarter-on-quarter, a slightly faster rate of growth compared to the 0.8% quarter-on-quarter recorded the previous quarter in Q2. Annual growth stood at 2.9% year-on-year, the fastest rate since Q1 2012, with Manila and Singapore seeing strong growth in the region.

As the year comes to an end, office leasing activity will remain stable. The APAC Office Rental Index is projected to strengthen by 4.0% this year, and growth is set to continue into 2015. Singapore will continue to stand out as one of the top performers in the region along with strong growth expected in Japan.

Other key APAC office market highlights in Q3 include:

- Manila -- up 6.5% quarter-on-quarter -- and Singapore -- up 3.3% quarter-on-quarter--retained their position as the top performers in the region on the back of continued lack of prime space in central business districts. Several markets including Sydney, Melbourne and Shanghai, all of which have been trending down for over a year, recorded rental growth this quarter, suggesting that market demand is gradually improving. Weaker markets in Q3 include Seoul and Mumbai, which saw slow office demand, resulting in further rental declines. A noteworthy decline was also reported in Beijing, where rents fell for the first time since the market entered the upcycle in 2010/11. Despite this, market fundamentals remain solid and landlords retain the upper hand in negotiations.

- Net absorption in Asia fell by 17% quarter-on-quarter to 8.5 million sq. ft., but this should not be an indication of a slowdown in office leasing momentum, as the total net absorption rose 34% year-on-year to 27.9 million sq. ft. Tokyo, which recorded the strongest demand of any market in Q2, saw net absorption temporarily turn negative in Q3 due to the addition of backfill space; Seoul also recorded negative net absorption for the second consecutive quarter.

- Q3 saw new supply in Asia increase by 12% quarter-on-quarter to 8.9 million sq. ft. China and India continued to dominate new office supply, accounting for 83% of total space completed this quarter. New completions in Beijing surged to 1.3 million sq. ft., a figure just under the total in the city for the whole of 2013.

- Office vacancy in Asia continued to decline, falling by 27 bps to 8.4%, the lowest level recorded since Q2 2008; however a few markets, including Hanoi and Beijing, reported sizable increases. In the Pacific, vacancy stabilized at 10.1% for the past year, yet due to a decline in sublease space and steady occupier demand, Q3 saw Sydney and Melbourne record an unexpected decline. With limited availability of prime space in Asia Pacific, occupiers are finding it difficult to secure space meeting their requirements, even in markets facing oversupply such as Jakarta and Ho Chi Minh City.

CBRE's Head of Brokerage Services and Regional Managing Director Manish Kashyap commented, "The office sector will continue to witness moderate expansionary demand, driven by domestic companies or Asian-based occupiers replacing multinationals as tenants in core areas. This can be seen in Hong Kong where firms from Mainland China are taking up space vacated by foreign occupiers. Even though they still see Asia Pacific as their key focus for business growth in the long term, multinationals are generally implementing cost effective solutions by moving to decentralized areas or outsourcing. We expect to see steady activity in the traditional banking sector but demand from the Technology, Media and Telecoms (TMT) sector will also remain strong."

Kashyap continued, "Looking ahead, a significant increase in new office supply will lead to more focus on tenant retention. Emerging markets such as Jakarta and Beijing will see a supply peak, forcing landlords to be more flexible towards rental negotiations. Elsewhere, an increasing number of large new projects are expected to be completed in 2015 in Brisbane, Melbourne and Sydney, ensuring they remain tenant markets. These trends will put tenant retention as a top priority for landlords in the near future."

CBRE's Director of Research Jonathan Hsu commented, "In Q3 2014, Manila and Singapore saw continued strong growth as a result of limited prime space in central business districts--in particular driven by the growth of business process outsourcing in the Philippines and the expectation of rent increases in Singapore. Tokyo saw the strongest demand of any market year-to-date, and will continue to grow in 2015, but this growth rests strongly on current market sentiment and the success of Japan's government policies. Whilst growth is currently strong, there is some risk that this may be derailed in 2015 if the 'third arrow' of Abenomics, structural reform fails to materialize or have its intended effect."

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More