The WPJ

Residential Real Estate News

To Keep Up with Rising U.S. Home Prices, Buyers Need to Save $600 a Month

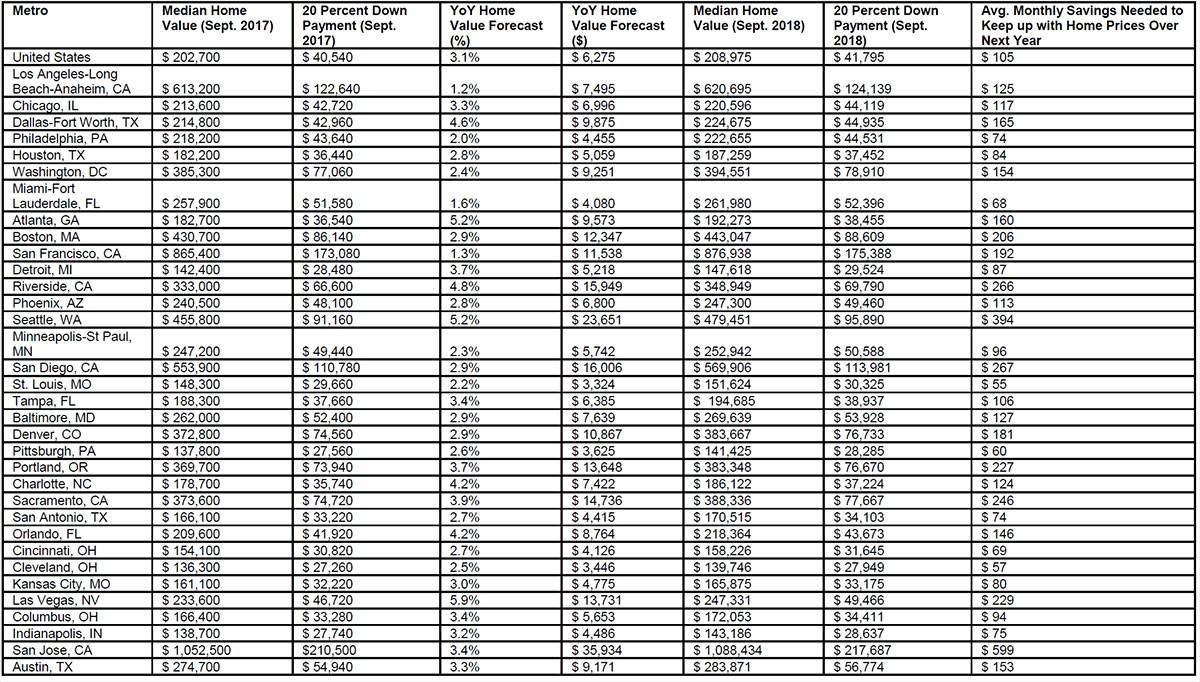

According to Zillow, saving for a down payment is a moving target for many first-time buyers, especially in pricey markets like Seattle and San Jose, where home values are expected to rise as much as $36,000 over the next year.

For future U.S. homebuyers wondering when to stop saving and get into the housing market, the math is clear: the sooner the better. With home values forecasted to rise in every major U.S. metro over the next year, a 20 percent down payment on the median-priced home today will cost thousands of dollars more just one year from now.

Nationally, the median home will be worth $6,275 more a year from now, according to Zillow's home value forecasts. That means the average U.S. buyer will need to save an additional $105 a month - $1,260 total over the next year - just to account for how much more a 20 percent down payment will cost a year from now.

In hot coastal markets like San Jose, home values are expected to rise as much as $35,934 by this time next year, the highest annual dollar increase of the metros analyzed. A buyer in 2018 will then need $7,188 more for a down payment on the median home than they would today. For those saving on a monthly basis for a future home purchase, that equates to putting away an additional $599 a month just to keep up with home value appreciation, let alone whatever else is needed for the down payment itself. Future home buyers in Seattle, San Diego and Riverside, Calif. can also expect to spend thousands of dollars more on down payments for the median home a year from now.

Saving for a down payment is one of the biggest hurdles to homeownership. That may be why more than half (59 percent) of all first-time buyers today put less than 20 percent down on their home purchase, according to Zillow Group's Consumer Housing Trends Report 2017. However, a small down payment does not come without risks. The report also found that buyers with larger down payments are more likely to get their offer accepted, averaging just 1.9 total offers before winning their house compared to 2.4 for buyers with lower down payments. When time is money, a low down payment can be costly.

"Sky-high rents and rising home prices are putting first-time buyers in a bit of a catch-22," says Dr. Svenja Gudell, Zillow chief economist. "Buying now with a low down payment can be riskier, and the offer may not be considered as competitive by the seller. However, a renter who saves for another year to reach a larger down payment may find that the home they love today is outside their budget a year from now. For those considering buying in the next year, getting into the market today may make more financial sense than they think."

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More