The WPJ

Vacation Real Estate News

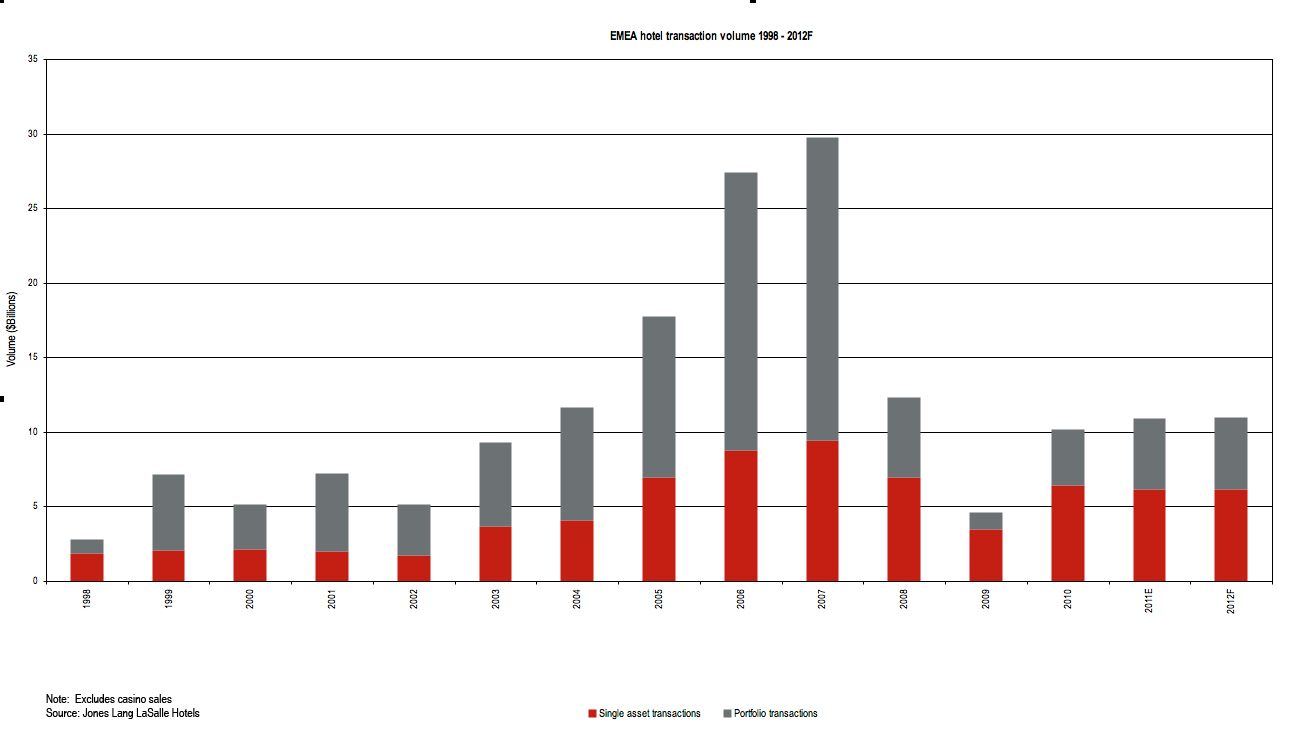

Middle East, Europe, Africa Hotel Investments to Top $11 Billion in 2012, Bank Restructurings Drive Market

Based on Jones Lang LaSalle Hotels' latest Hotel Investment Outlook report, hotel investment activity is expected to remain stable across Europe, the Middle East and Africa (EMEA) during 2012 with $11 billion worth of deals forecast for the year, reflecting transaction volumes similar to 2011 levels of $10.9 billion.

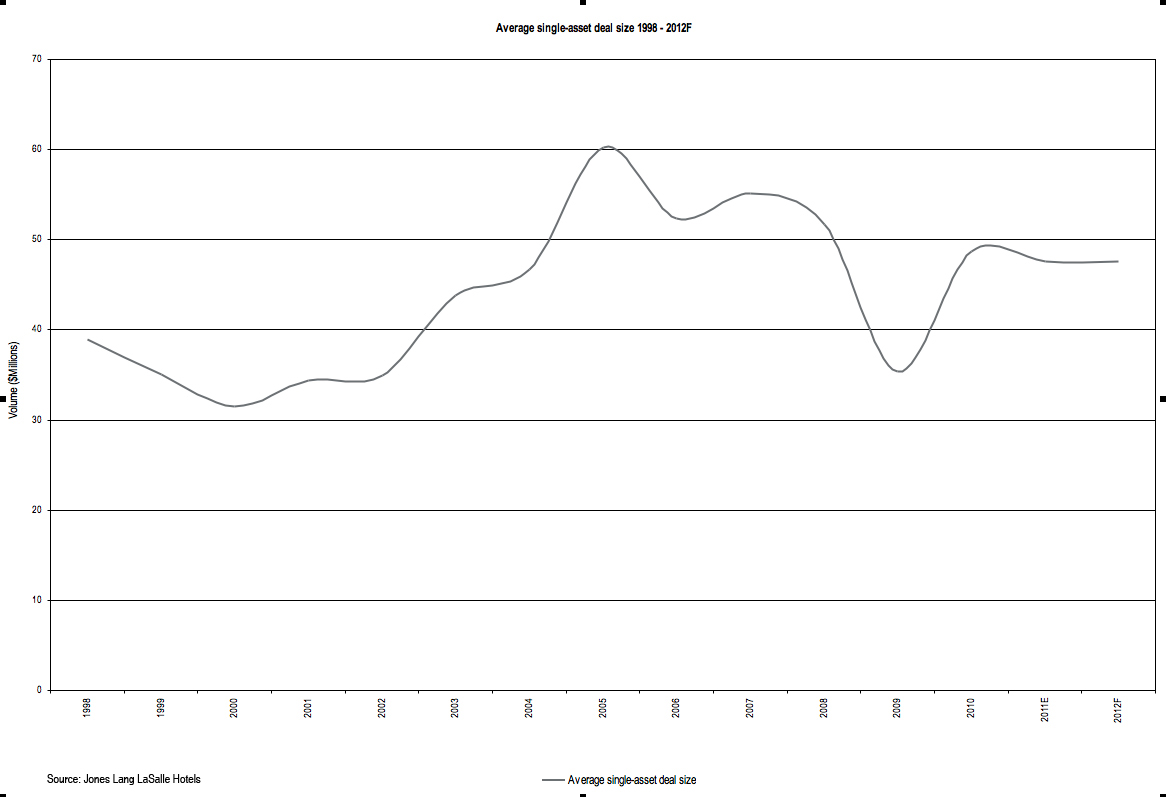

Much of this activity will be driven by debt restructuring deals. Jones Lang LaSalle Hotels' anticipates that single asset transactions will continue to drive the majority of activity for 2012.

Jon Hubbard, CEO Northern Europe for Jones Lang LaSalle Hotels tells World Property Channel, "The enduring theme in 2012 in EMEA will be the increasing pricing gap between primary and secondary assets and the narrowing bandwidth of what constitutes a prime asset. The prime market will continue to see high net worth individuals (HWNIs) and sovereign wealth funds buying trophy hotels in key gateway cities. Such assets are regarded as a source of long term investment, despite their low yields and high cost per key. Equity rich investors will be primarily from the Middle East and Asia and will continue to pay record prices for quality assets."

The UK is expected to remain the most liquid market and is predicted to see a slight increase in transaction activity in 2012. This will be driven by distressed capital structure deals as banks have to meet stricter capital requirements and uncertainty increases around the pace of a recovery in capital values causing the hold option to become less attractive.

"Similarly transaction activity in France and Germany is expected to be steady, with a potential increase on 2011 levels. Like London, Paris will remain the primary driver for investment activity in all sectors. In Germany investors are expected to continue focus on assets in key cities with less inherent risk, but they will also consider secondary assets or secondary cities that present higher yielding investment opportunities", added Christoph Härle, CEO Continental Europe for Jones Lang LaSalle Hotels.

Conversely, following the sale of the Ritz-Carlton Moscow by Jones Lang LaSalle Hotels, Russia will suffer from a lack of trophy sales which will reduce total transaction volumes compared to last year, while Dubai is expected to benefit from being a safe haven and attract some investor interest given that its occupancy has recovered to 2008 levels this year.

As developments continue to be constrained by a lack of financing, hotel operators are expected to become more active buyers on unencumbered assets in 2012, jointly investing with other investors. As these operators move away from an "asset light strategy" to an "asset right strategy", they will continue to purchase hotels in key locations to gain market entry, increase their market share or establish new brands.

Hubbard continued, "Softening yields will also encourage more private equity firms onto the playing field. The growing amount of distressed assets coming on the market, selling at discounted prices with higher yields, will offer opportunities for those investors. Private equity funds will also be in disposition mode, with expiring debt on their books that will need to be refinanced in 2012."

Banks will also continue to play a major role on the sell side, taking hotels into receivership and placing distressed assets on the market. Bank enforced and receivership sales are expected to increase in 2012 with the UK Marriott portfolio of 42 assets, the Hyatt in Birmingham and the famous Belfry Hotel & Golf Resort amongst those hotels which are currently being marketed and expected to transact in 2012.

The main constraint of the market will continue to be the lack of debt and this will persist in 2012 with loan to value ratios between 50% and 60% and loan to construction cost ratios of about 50% for developments. Thus, smaller lot sizes will continue to attract more interest with lower capital requirements.

"The Sovereign debt crisis will continue into 2012 and despite government pressure to increase lending, realistically there is no prospect of significant fresh debt emerging in 2012. Many countries will implement further austerity measures to regain confidence in the financial markets. The high private savings rates and the poor bank credit availability will limit growth in Western Europe, which is forecast to slow to 0.3% in 2012. Investors will be expected to be more selective in their buying behavior due to the broad choice of stock available", concluded Härle.

Real Estate Listings Showcase

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More