The WPJ

Commercial Real Estate News

Office, Industrial Markets in U.S. Strengthen in Q3

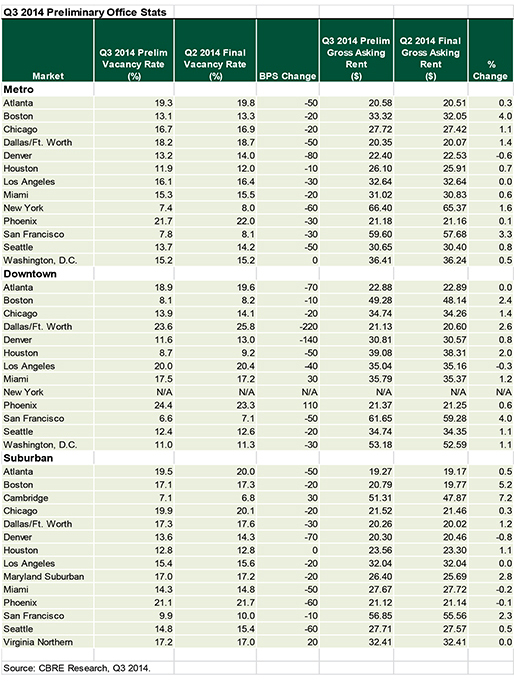

According to data from CBRE Group, office vacancy rates declined in most major U.S. markets during Q3 2014. Twelve out of 13 major metro office markets saw vacancy fall and 11 markets saw average asking rents increase as tenants' appetite for space continues to grow.

"Office space demand is expected to remain strong with continued improvement in the U.S. economy and steady expansion in office-using employment. Demand growth, coupled with the subdued national development cycle, bodes well for vacancy declines and sturdy rent growth," said Sara Rutledge, Director of Research and Analysis, CBRE.

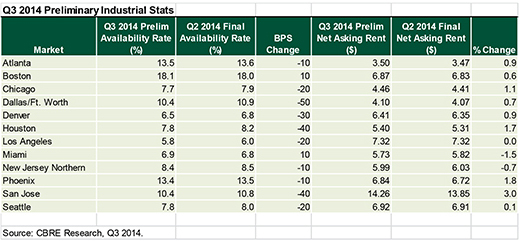

The U.S. industrial market also had healthy activity in Q3 2014, according to CBRE, with availability declining in 10 of the 12 major markets. Third-party logistics firms continued to expand nationally, with many markets reporting robust demand driven by that sector.

"The U.S. economy continues to expand, with employment rising and exports growing faster than expected. Q3 is predicted to be a strong quarter. This will help drive industrial space demand nationally," said Jared Sullivan, CBRE Senior Economist.

U.S. Office Data:

- Denver, which has seen steady demand from energy and business services firms, led the way in vacancy declines, with a vacancy rate drop of 80 basis points (bps) during Q3 2014. Despite this, asking rents slipped over the quarter as occupancies were taken in high-quality space, which has yet to be replenished with new deliveries.

- New York saw its vacancy rate drop 60 basis points.

- Atlanta, Dallas/Ft. Worth and Seattle all posted 50 basis points declines in Q3 2014.

- Washington, D.C. was the lone market with flat vacancy over the quarter, holding at 15.2 percent since Q2 2014.

- Boston posted the strongest quarterly average asking rent growth, at 4.0 percent on a dearth of availability in quality space and continued strong demand from tech and life sciences firms. San Francisco was second, with 3.3 percent growth in Q3 2014.

- Office development remains subdued nationally, but many of the strongest markets are seeing increased pipeline activity. Houston continues to lead the pack, with 17.3 million sq. ft. underway to-date in Q3 2014.

U.S. Industrial Data:

- The Texas markets posted the largest quarter-over-quarter availability rate decreases, with Dallas/Ft. Worth and Houston down 50 bps and 40 bps, respectively. Dallas/Ft. Worth benefited from expanding logistics companies, which are taking advantage of the strong local infrastructure, while Houston continued to ride the expanding energy boom occurring throughout the nation.

- Although rents still remain below prerecession levels in most markets, rents increased in nine of the 12 major markets during Q3 2014, a reflection of improving market fundamentals.

- Construction activity picked up pace in the major markets, led by Dallas/Ft. Worth, with 16.7 million sq. ft. under construction, followed by Chicago and Atlanta, with 10.9 and 6.2 million sq. ft. under construction, respectively.

- Free rent and other concessions are being scaled back in many of the nation's major industrial markets.

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More