Commercial Real Estate News

Tokyo Office Demand Spills into Non-Core Wards in 2025

Tokyo's office market is undergoing a notable geographic shift in 2025, as rising rents and limited availability in the city's central business districts push companies to relocate to outer wards.

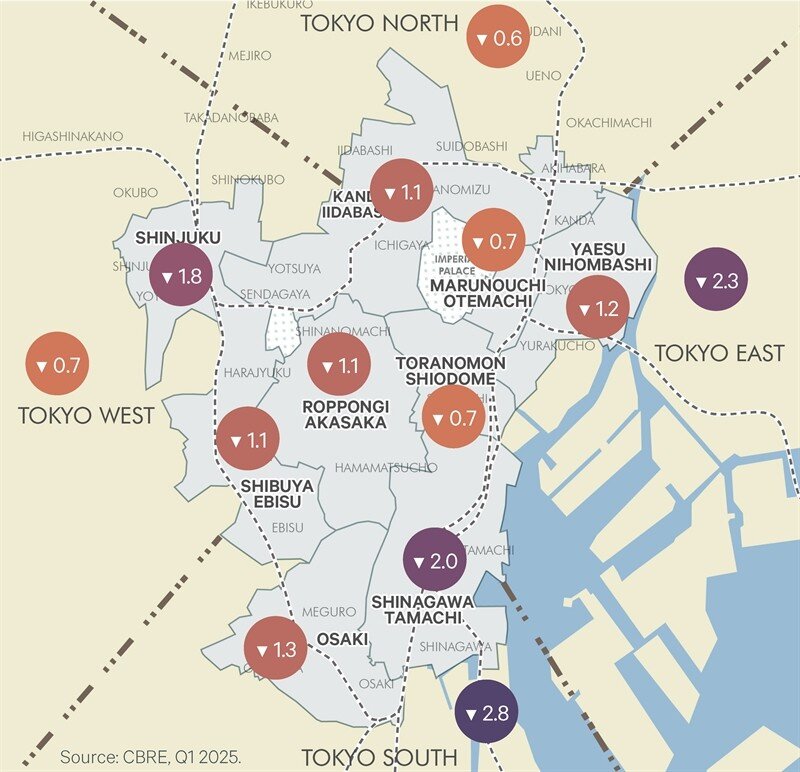

According to CBRE, vacancy rates in Tokyo's non-core areas--comprising 18 outer wards--declined by 1.8 percentage points year-over-year in the first quarter of 2025. By comparison, core areas--made up of five central wards--saw a smaller drop of 1.2 points over the same period. While vacancy remains higher in the periphery at 5.8% versus 2.4% in central districts, the narrowing spread reflects accelerating demand beyond traditional business hubs.

CBRE reports the steepest vacancy declines were recorded in Tokyo South and Tokyo East, which posted respective year-on-year drops of 2.8 and 2.3 percentage points--making them the most active among the city's 13 submarkets.

Large office spaces in the core market are becoming increasingly scarce. CBRE data show that vacancy for units between 3,000 and 9,999 tsubo has fallen below 2%, while spaces above 10,000 tsubo are only slightly more available at 2.4%. This limited inventory has led to sharp increases in asking rents and pushed many companies to look further afield for suitable space.

Peripheral markets are also attracting demand for specialized facilities that require unique infrastructure--such as reinforced flooring, higher ceilings, or open layouts. These include R&D centers, studios, showrooms, and test kitchens. The core districts often cannot accommodate such requirements affordably, making non-core areas more appealing for operational efficiency and cost control.

Construction delays and rising material costs are exacerbating the supply shortage in central Tokyo, postponing the delivery of new Grade A buildings. At the same time, strong pre-leasing activity in upcoming projects is restricting near-term availability and applying further upward pressure on core rents.

Despite six consecutive quarters of rent increases in non-core markets, they remain considerably more affordable than their central counterparts. This pricing dynamic, combined with renewed business expansion and the continued return to office post-pandemic, is sustaining momentum outside the city center.

Companies are adapting their real estate strategies to better align with new workplace norms, often blending centrally located headquarters with decentralized secondary offices in less expensive zones. While access to transit remains critical, flexible work arrangements are enabling firms to prioritize value and functionality over centrality.

Historically, Tokyo's office market has followed a similar pattern during prior tightening cycles, including those after the dot-com bust and the 2008 financial crisis. In each case, demand in non-core areas lagged behind the core by six to eight quarters--suggesting that the current trend may still have room to run.

Vacancy patterns in older properties--those built more than five years ago--further highlight the structural nature of the shift, as absorption spreads beyond the city's traditional business centers.

As Tokyo's office market rebalances, the outer wards are no longer just fallback options--they are emerging as strategic destinations for a wide range of occupiers, says CBRE.