The WPJ

Commercial Real Estate News

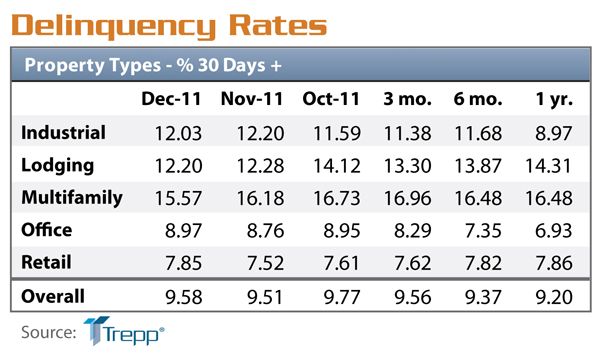

CMBS Delinquency Rates Uptick in December

According to a new report by Trepp, after a positive November delinquency report, CMBS delinquency rates reversed course and moved higher in December.

According to a new report by Trepp, after a positive November delinquency report, CMBS delinquency rates reversed course and moved higher in December.Trepp views this as the first of a six to twelve month stretch where the rate could increase by 75 basis points in aggregate. This will come as a result of the first wave of 2007 originated loans reaching their balloon dates over the next few months.

Report Highlights:

- Overall U.S. delinquency rate increases to 9.58%--up seven basis points in December.

- Percentage of loans 30+ days delinquent or in foreclosure: December: 9.58%, November: 9.51%, October: 9.77%.

- If defeased loans were taken out of the equation, the overall delinquency rate would be 10.03%--up eight basis points.

- Percentage of loans seriously delinquent (60+, in foreclosure, REO or non-performing balloons) is at 9.06%--up 18 basis points.

Losing Year for CMBS

2011 will be remembered by tremendous peaks and valleys.

The CMBS market rallied smartly from January until March. At that point, concerns about the impact of the Japanese tsunami and unrest in the Middle East took the winds out of the sails of the CMBS market.

The market resumed its ascension in late April and May. The GG10 bond hits its post-credit crisis best level of about 170 basis points over swaps around this time.

The rally was short-lived, however, as worries over a weakening U.S. economy and the possibility of a Greek default weighed on all the financial markets. This triggered a three month losing streak for CMBS paper, which pushed spreads out to wide levels that had not been seen since August 2010.

As noted above, the market found its sea legs late in the year, but not without some collateral damage from the volatility. Many issuers pulled back or closed their doors entirely, leading many CMBS prognosticators to reduce their forecasts for 2012 issuance

By year's end, spreads were wider but not by nearly as much as one might have feared over the summer. Legacy super seniors were wider by 30 to 50 basis points on average. The GG10 A4 bond was off by 35 basis points over the course of the year.

December Numbers

- Legacy 10-year super senior spreads were 20 to 25 basis points tighter in December in aggregate.

- Average 2007 super seniors are now about 250 basis points over swaps.

- One year ago the average 2007 super senior was 213 basis points over swaps.

- Six months ago the average 2007 super senior was 186 basis points over swaps.

- Eighteen months ago the average 2007 super senior was 351 basis points over swaps.

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More