The WPJ

Commercial Real Estate News

Global Commercial Property Investment Flattens in 2019

Slowdown driven by fewer ultra-large transactions, Brexit and trade policy uncertainties

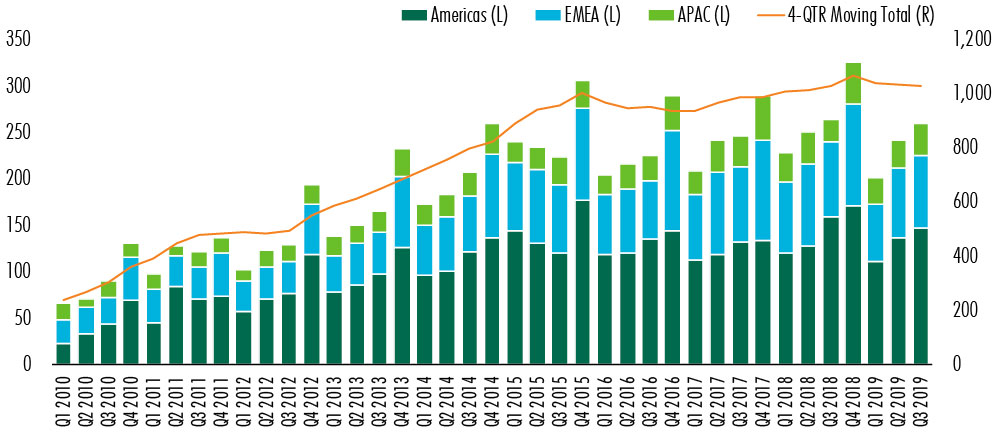

According to new report from CBRE, global commercial real estate investment volume, including entity-level deals, rose by 7% quarter-over-quarter but fell by 2% year-over-year in Q3 2019.

Year-to-date volume was down by 5% from the same period last year. On a regional level, APAC reported an impressive 49% year-over-year increase in Q3 that offset the sluggishness in H1 and lifted year-to-date growth to 6%. The Americas and EMEA recorded a relatively soft third quarter due to political uncertainty, low yields and some recession fears.

Richard Barkham, CBRE's Global Chief Economist & Head of Americas Research comments, "CBRE's full-year outlook for global commercial real estate investment is for a single-digit percentage point decline from 2018's record level. Despite uncertainties over Brexit and multiple trade disputes, a major downturn has been kept at bay by lower interest rates, tight labor markets and confident consumers. The trend of fewer mega-deals will likely continue into 2020 until business sentiment picks up."

Key report highlights include:

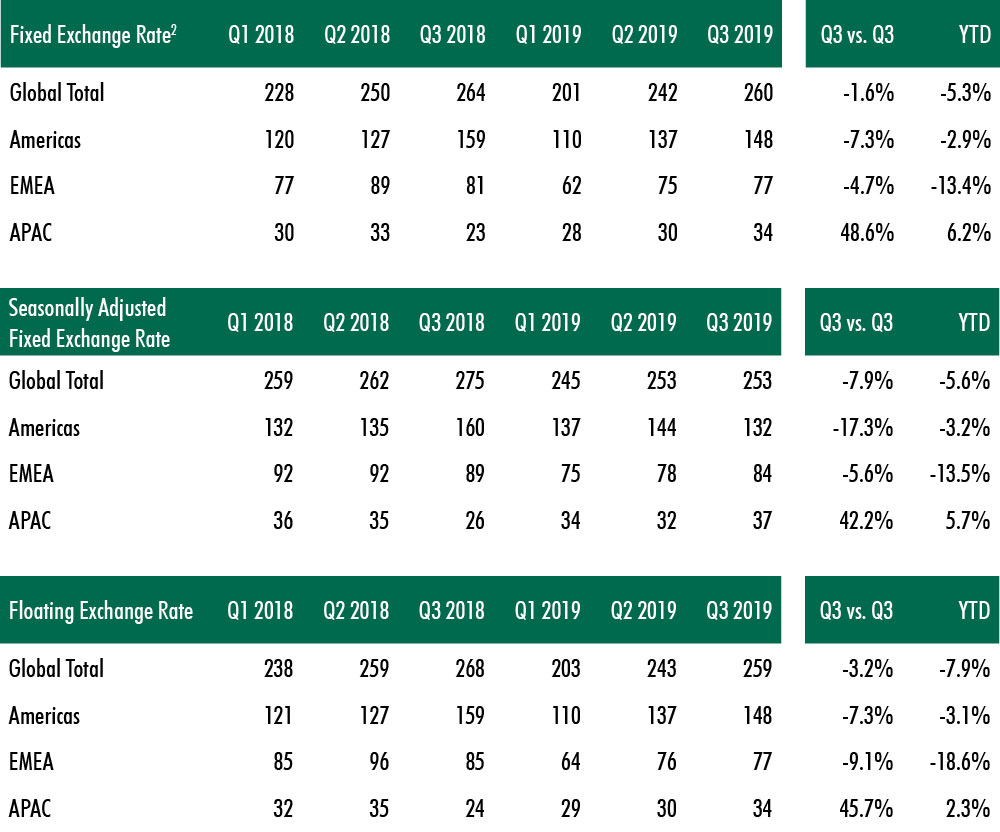

- Global commercial real estate (CRE) investment, including entity-level deals, totaled US$260 billion in Q3 2019, up by 7% over the previous quarter but down by 2% from Q3 2018.

- Seasonally adjusted Q3 investment volume matched that of the previous quarter but was down by 8% year-over-year.

- U.S. investment volume was slightly down year-over-year in Q3 but is up mildly year-to-date after adjusting for seasonality, entity-level transactions and Blackstone's acquisition of GLP's U.S. logistics portfolio.

- APAC had a nice rebound in investment activity, while uncertainties around Brexit continued to dampen investor sentiment in EMEA. Nevertheless, investment volume improved from the weak first half of 2019 in EMEA, led by robust activity in France, Sweden and Germany.

- Recent interest rate cuts have widened yield spreads, which has revived investor interest.

- Paris replaced London as the No.1 destination for foreign capital worldwide for the first time on record. The percentage of cross-border investment hit a six-year low globally in Q3.

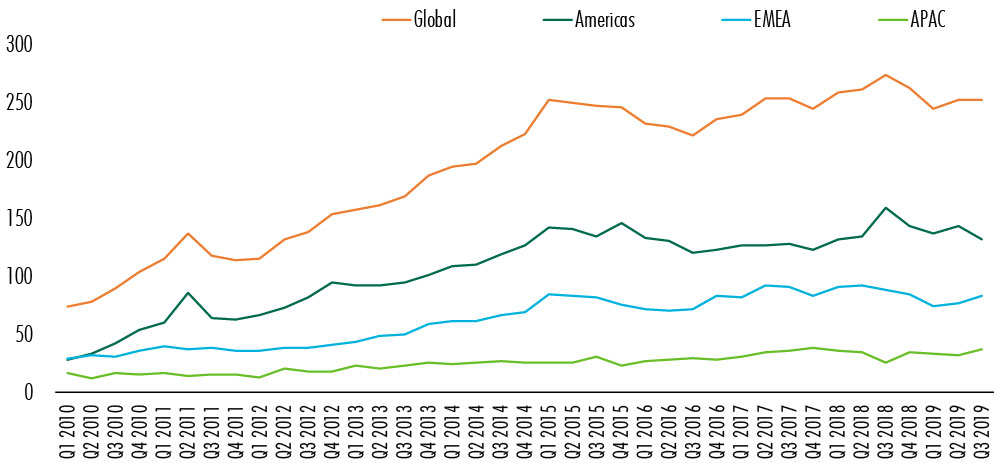

Seasonally adjusted Americas investment volume decreased by 17% year-over-year and 3% year-to-date, mainly driven by lower volumes in Canada and the U.S. Accounting for more than half of global activity, U.S. investment volume (seasonally adjusted) fell by 7% year-over-year and 1% year-to-date. But if just a single transaction were excluded--Blackstone's $18.7 billion acquisition of GLP's U.S. industrial portfolio--the U.S. would have registered only a 2% decline year-over-year and a 3% increase year-to-date (seasonally adjusted). Decreased U.S. investment volume was almost entirely due to fewer entity-level transactions in Q3 2019. Excluding entity-level deals, U.S. investment volume increased by 14% year-over-year and 8% year-to-date after seasonal adjustment.

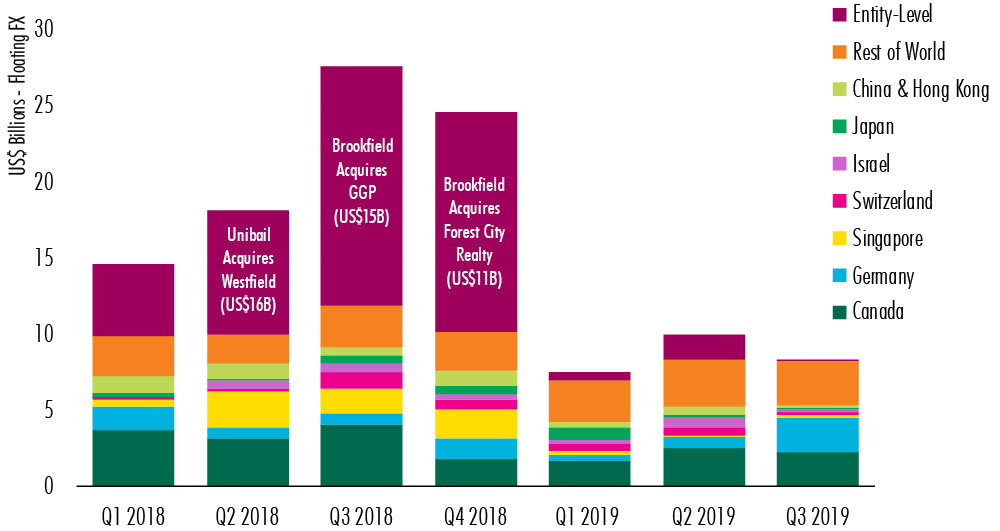

The percentage of cross-border investment hit a six-year low globally in Q3. This was a result of fewer ultra-large transactions and an absence of big-ticket retail REIT acquisitions. While the valuation of retail REITs has partially recovered and made them more expensive, Asian investors who have been big cross-border players turned to more domestic and intra-regional investment, in addition to capital controls in China.

The downturn was especially evident in the U.S., where cross-border investment has fallen by 57% year-to-date compared with the same period last year (Figure 3). The sharp decrease in entity-level transactions contributed to 75% of the decline, while less inbound investment from Singapore, Japan, China and Hong Kong contributed another 15%.

EMEA investment volume fell by 6% year-over-year in Q3 (seasonally adjusted). Investment activity stalled in the U.K. (-28%) and Spain (-44%), while France (44%) and Sweden (307%) recorded strong year-over-year growth. Notably, Paris replaced London as the No.1 destination for foreign capital for the first time on record. Germany's Q3 investment rebounded strongly and leveled with the same period last year. Year-to-date, EMEA investment volume fell by 14% (seasonally adjusted), of which the U.K. and Germany accounted for 61% and 20%, respectively. As in the Americas, the fall in investment was a result of low availability of quality product and fewer mega-deals, particularly in the top five European markets.

Office and residential properties remained the most attractive investment assets in EMEA. Investors concentrated on income growth, capitalizing on steady leasing activity and rent growth, but uncertainty over the EU's rent control polices weighed on the residential sector. In the U.K., uncertainty about Brexit has kept investors cautious despite ample liquidity and relatively high yields. We remain optimistic for an orderly Brexit, which should revitalize the market.

Investment volume in APAC surged 49% year-over-year, or 42% after seasonal adjustment. The increase is partially attributable to a low base effect, as 2018 had the lowest Q3 investment volume since 2013 due to escalation of the U.S.-China trade dispute. This applies especially to China, where year-over-year growth reached 68% in Q3 (seasonally adjusted). Investor sentiment in Australia (42%), Japan (31%) and Singapore (62%) improved from lower interest rates leading to more attractive yield spreads and an overall uptick in big-ticket transactions. Australia had the highest quarterly office investment volume since 2005. Hong Kong (-9%) continued to record declines in investment volume due to social unrest. APAC's year-to-date total of US$92 billion was up by 6% (seasonally adjusted) from the same period last year.

Overall, Asia continues to provide comparatively high yields and income growth potential for global investors. In the first three quarters of 2018, only 8% of Asia's investment sourced cross-border capital. In the first three quarters of 2019, this has risen to 13%, largely from U.S., Canadian and German capital.

Real Estate Listings Showcase

{kind=link}

{kind=link}

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More