The WPJ

Commercial Real Estate News

Foreign Real Estate Investment in Japan Spikes 61 Percent Over Last Year

According to CBRE's Quarterly Survey on Japanese Real Estate Investment for Q3, 2015, a significant increase of foreign real estate investment capital is now flowing into Japan in 2015.

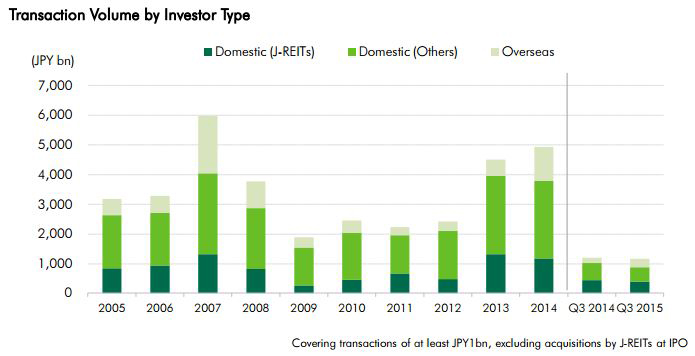

The total value of real estate investment transactions (transactions of JPY1 billion or more) in Japan in Q3 2015 decreased 2.7% y-o-y to JPY 1.2 trillion. Acquisitions by J-REITs declined 10% y-o-y to JPY 394.1 billion, those by other Japanese investors fell 17% to JPY 487.9 billion, but acquisitions by overseas investors rose 61% to JPY 292.7 billion. J-REITs were somewhat subdued in terms of purchasing activity this quarter as share prices weakened. In contrast, overseas investors continued to be very active, completing several large acquisitions, including a number of office portfolios and retail malls.

Cap rates remained on a downward trend due to the lack of investment opportunities, while rents continued to rise, particularly for offices. It is no longer unusual to see transactions of prime offices and retail properties in central Tokyo at cap rates under 3%. Here onwards, however, yields are likely to decline further for assets in regional cities.

Expected yields hit record lows for Tokyo office, retail, and industrial sectors

CBRE's latest quarterly survey (October 2015) found that average1 expected yields (based on NOI2) have further declined for Tokyo office, retail, and industrial properties. Offices in Otemachi fell by 3 bps q-o-q to 3.75%, continuing the trend of a new low every quarter in 2015. In the Ginza Chuo Dori retail sector, expected yields dropped 14 bps to 3.80%, a record low. Yields for industrial properties also hit a record low (down 5 bps to 5.0%). However, yields were flat q-o-q for rental apartments (4.65% for studio-type and 4.75% for family-type) and for hotels (5.25%).

CBRE's latest quarterly survey (October 2015) found that average1 expected yields (based on NOI2) have further declined for Tokyo office, retail, and industrial properties. Offices in Otemachi fell by 3 bps q-o-q to 3.75%, continuing the trend of a new low every quarter in 2015. In the Ginza Chuo Dori retail sector, expected yields dropped 14 bps to 3.80%, a record low. Yields for industrial properties also hit a record low (down 5 bps to 5.0%). However, yields were flat q-o-q for rental apartments (4.65% for studio-type and 4.75% for family-type) and for hotels (5.25%).As they did in Tokyo, expected NOI yields also declined for office properties in regional cities. Osaka saw a 5 bps fall q-o-q to 5.50% and Nagoya a 3 bps fall to 5.80%. Yields in both cities are approaching the same levels as the last cyclical bottom in January 2008 (5.20% for Osaka and 5.33% for Nagoya). Yields also declined in other regional cities: Fukuoka was down 2bps to 5.63%, Sapporo was down 5bps to 6.10%, and in Sendai, where the market saw the transaction of the landmark AER building, and yields fell 10 bps q-o-q to 6.05%.

Investors continue to display a healthy appetite for office and industrial assets

CBRE's October 2015 Tankan survey asked respondents to compare current conditions to three months ago (with results collected as Diffusion Indices). Topics were: 1) trading volume, 2) sales price, 3) NOI (or rents and vacancy rates for logistics facilities), 4) expected yields, 5) lending attitude of financial institutions, and 6) strategies for investment and loans. For Grade A office buildings, the DI decreased for respondents' stance on investment and loans (down 4 points q-o-q) and trading volume (down 2 points), whereas the lending attitude of financial institutions remained constant, and the remaining three questions showed improvement in DI figures. While there is still a shortage of investment properties and expected yields are falling, the funding environment is favorable. However, some investors have stated that for the first time this year, their stance on investment and loans are "cautious." The external environment has changed significantly during the quarter, with growing uncertainty on how China's economic slowdown will impact the Japanese economy. Although they accounted for only a small number of responses, some core investors displayed a rather cautious attitude.

The DI for logistics facilities (multi-tenant-type) in October improved only for respondents' stance towards investment and loans (up 2 points q-o-q); the remaining five questions showed a decrease. This was due to a significant number of respondents answering "no change." For the one area where the DI improved, investment and loans, the number of positive responses show that investors' appetite remains healthy. One concern is the large volume of pipeline supply, but the number of respondents who expect worsening conditions in six months' time was flat. For investment and loans in particular, the average forward-looking DI improved from 33 to 37. Although respondents' expect rise in vacancy rate on the back of increase in new supply, sentiment remains positive thanks to solid demand for warehouses.

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More