The WPJ

Commercial Real Estate News

U.S. Commercial Market to Benefit from EU's Recent Brexit Vote

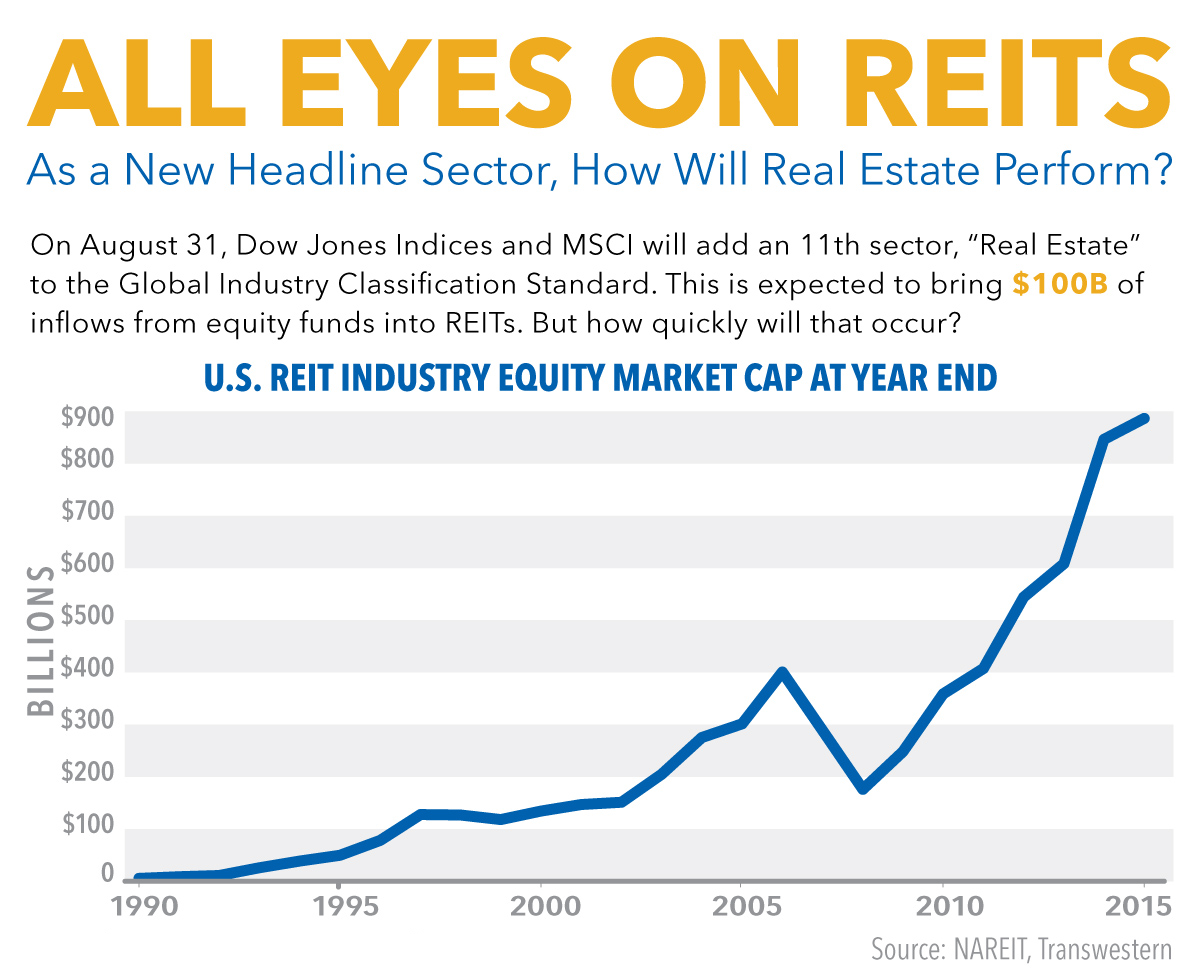

New Global Industry Classification to Bring $100 Billion of New Capital to REITS

According to a new report by Transwestern, the impact of Brexit will be long and protracted, which will likely result in increased volatility in the capital markets.

In the short term, the impact has been generally positive for the U.S. with the flight to safety driving down 10-year treasury notes to a new historic low of 1.39%.

In addition, a new headline sector under the Global Industry Classification Standard (GICS) for Real Estate, effective Sept. 1, 2016 bodes well for the industry, as it speaks to the sector's growth over the last two decades. The change is expected to bring $100 billion of inflows from equity funds into the REIT sector.

Transwestern reports these positive indicators for commercial real estate even as the U.S. economy loses some steam. April and May sales and consumption numbers were strong, but corporate profits, business investment and job growth continue to decline, leading to an underwhelming second-quarter GDP growth of 1.2%. Commercial real estate has enjoyed positive fundamentals and ample liquidity on the equity side, but the debt side saw some contraction in the first half of 2016, primarily in CMBS and bank financing.

20 'Big-Picture' Fast Facts:

- Average monthly job growth rebounded in June and July, coming in at 287,000 and 225,000, respectively.

- The Federal Reserve reported that all large banks passed the stress test with flying colors, meaning they can withstand $400 billion in losses.

- Standard & Poor's expects U.S. corporate default rate to rise to 3.3% by September 2016 from 2.6% a year ago.

- Junk bond average yields are currently at 7.4%.

- The Wall Street Journal reported that 20 of the world's largest banks lost 25% market value in the first half of 2016.

- The Japanese 20-year note slipped below 0% for the first time; 10-year note yields dropped to negative 0.295%.

- In July, the ISM index of manufacturing activity hit 52.7, down slightly from 53.2 in June, a 16-month high.

- On June 26, the first ship passed through the Panama Canal after a $5.4 billion expansion.

- Auto sales increased 1.5% to 8.65 million vehicles in the first half of 2016, but there are some signs that sales have peaked after six years of gains with sliding sales in July at GM, Ford and Toyota.

- The 85,000 cap on H1-B visas was reached in less than five days - evidence that skilled labor is still in very short supply.

- In 2015, nearly 1 million international students came to the U.S., a 10% increase over 2014.

- First-half 2016 commercial real estate sales declined 16% year over year; however, record sales in 2015 were expected to moderate.

- Personal consumption spending remained healthy with 0.4% gains in both May and June.

- Online sales are up 10.2% year over year; department store sales are down 1.7% year over year.

- Closed-end commercial real estate private equity available funds, or dry powder, reached a record $236 billion in June.

- CalPERS reported earnings of 0.6% for year-end June 2016 versus an investment target of 7.5% for its $295 billion in assets. Real estate returned 7.1% but was 5.6 points below its target.

- The U.S. apartment sector is still healthy, with 49 of the 50 top markets posting rent growth in second quarter.

- In the first half of 2016, the average current pension fund investment in real estate was 8.5% versus an average target allocation of 9.8%, according to Prequin.

- High-flying FinTech firms hit a soft patch with layoffs of 5-40% as flight to safety trims loan portfolios.

- On August 31, 2016, Dow Jones Indices and MSCI will add an 11th sector, "Real Estate" to the Global Industry Classifications Standards, moving it out of the Financials sector.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More