Commercial Real Estate News

Commercial Mortgage Lending in U.S. Shows Signs of Stabilization in Late 2023

According to new data from CBRE, commercial real estate lending in the U.S. demonstrated signs of stabilization at the end of 2023, with borrowing costs appearing to have peaked, even as transaction activity remains subdued.

The CBRE Lending Momentum Index, which tracks the pace of CBRE-originated commercial loan closings in the U.S., increased by 1.0% from Q3 2023--marking the first quarterly increase since Q1 2022. The index still saw a decline of 38.1% compared to the strong loan volume of Q4 2022. The index closed Q4 2023 at a value of 189.

"While the capital markets continue to present challenges, we are seeing more constructive lending conditions for specific asset classes," stated James Millon, U.S. President of Debt & Structured Finance for CBRE. "We are experiencing a material decline in credit spreads in the liquid markets, lower trading band for benchmarks and a reset of cap rates at higher levels. Additionally, as the Federal Reserve has indicated interest rate cuts on the horizon, these factors combined have created a more favorable transactional environment in the first quarter."

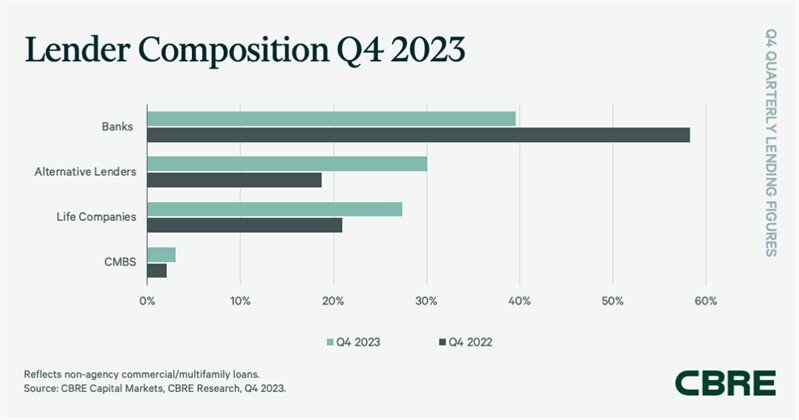

Banks maintained their position as the largest contributors to CBRE's non-agency loan closings for the seventh consecutive quarter, accounting for 39.5% of the total in Q3 2023--an increase from 38.4% in the previous quarter. Floating rate loans contributed about one-third of the loan volume in Q4 2023, with 38% allocated to refinancings and the remainder supporting property acquisitions.

Alternative lenders, such as debt funds and mortgage REITs, represented 30% of the Q4 2023 loan volume, up from 27.4% in Q3 2023, with multifamily assets remaining the preferred property type. Collateralized loan obligations (CLO) totaled $672 billion in Q4 2023, resulting in a significant decrease from the $30.3 billion recorded in 2022, with the 2023 annual total reaching just $6.67 billion.

Life insurance companies accounted for 27.4% of origination volume in Q4 2023, down from 33% in the previous quarter, predominantly in fixed-rate acquisition and refinancing loans for industrial and retail assets.

CMBS conduits accounted for less than 3% of non-agency loan volume in Q4 2023. Industrywide CMBS origination in Q4 2023 reached $12.86 billion, showing improvement compared to the previous quarter. Overall, CMBS volume for 2023 totaled $39.33 billion, representing a 44% decline from 2022.

Underwriting criteria changed slightly in Q4 2023. The average underwritten cap rate increased by 16 basis points (bps) to 5.68%, while the average loan-to-value (LTV) ratio rose to 61.4% from 58.3% in Q3 2023. Higher interest rates translated to loan constants averaging 6.72% in Q4 2023, representing a 79-bps increase year-over-year.

Government agency lending on multifamily assets slowed to $27.1 billion in Q4 2023, down from $29.8 billion in Q3 2023. CBRE's Agency Pricing Index, reflecting average fixed agency mortgage rates on 7-10-year permanent loans, rose 40 bps in Q4 2023 and 83 bps year-over-year to 6.04%.