The WPJ

Commercial Real Estate News

Global Commercial Investment Dips 2 Percent Annually in 2019

Political Unrest, Brexit Impacted 2019 Investment Flows

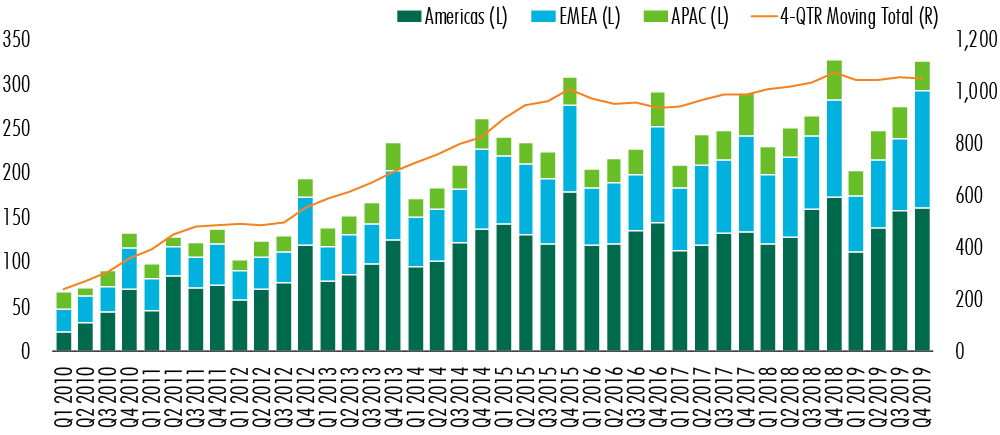

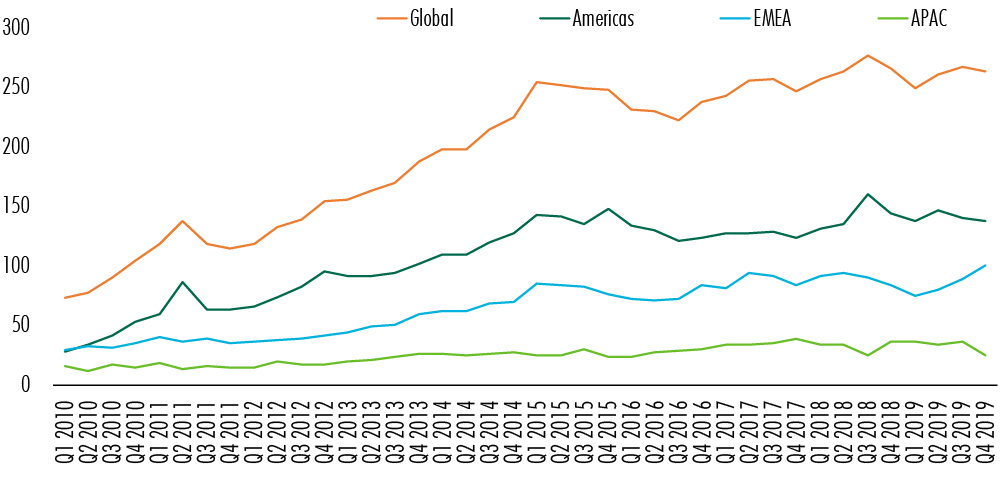

International property consultant CBRE is reporting this week that global commercial real estate investment volume in Q4 of 2019, including entity-level deals, was nearly level (-0.5%) with Q4 2018, while full-year volume fell by 2% from 2018.

Regionally, EMEA had substantial investment activity in Q4 of 2019, up by 19% year-over-year and compensating for subdued activity in the previous three quarters. Americas investment volume fell by 6% year-over-year in Q4, while APAC saw a 27% decrease.

2019 Global CRE Market FAQs:

The U.S. accounted for nearly half of global CRE investment volume in 2019. Despite constrained global market supply, low global bond yield expectations and falling hedging costs, investors should continue to favor U.S. CRE, as well as fuel a possible recovery of the mergers-and-acquisitions market.

EMEA investment volume grew by 19% year-over-year in Q4, while full-year volume fell by 2% to $352 billion. Q4 investment activity fell year-over-year in Spain (-44%) and France (-3%) but grew in the U.K. (27%) and Germany (55%). The U.K.'s full-year volume fell by 19%, largely due to prolonged political uncertainty regarding Brexit, while France (12%) and Germany (8%) saw their full-year volumes rise moderately and reach new highs. Other European markets continued to attract capital in 2019 despite historically low prime yields, with Ireland (58%), Sweden (56%), Austria (39%) and Italy (37%) all seeing double-digit full-year growth.

Big-ticket transactions and renewed investor confidence inflated investment volumes throughout Continental Europe, with deal sizes larger than $100 million increasing 9% year-over-year. Furthermore, office and residential assets remained the most attractive. Investment volumes throughout Europe remained high, with mergers-and-acquisitions deals remaining prevalent. Additionally, the European Central Bank's decision to lower interest rates and restart quantitative easing gave an added stimulus to investment volumes this quarter. In 2020, as Western European markets continue to return low yields, capital likely will look toward a recovering U.K. market and Central and Eastern Europe for higher returns on CRE investments.

APAC investment volume fell by 27% year-over-year in Q4, while full-year volume fell by 2% to $131 billion--above the five-year average of $125 billion. The decline in transaction volume was due to fewer big-ticket transactions than in Q4 2018 and a significant decline in Hong Kong investment volume due to ongoing political turmoil. Hong Kong's Q4 2019 volume was the lowest quarterly total since the global financial crisis in 2008.

Nevertheless, several key APAC markets had increased investment volume in H2 2019. Australia and China had increases from domestic investors, while investment volume in Korea reached a record high, with office and logistics assets in highest demand. Japan continued to attract capital in 2019 largely due to its attractive yield spread offering.

The outbreak of the Wuhan coronavirus poses negative risks to investment sentiment in the region, with Greater China expected to have a slow start in Q1 2020. Investors likely will reduce their pace of investment and wait to determine the full extent of the outbreak.

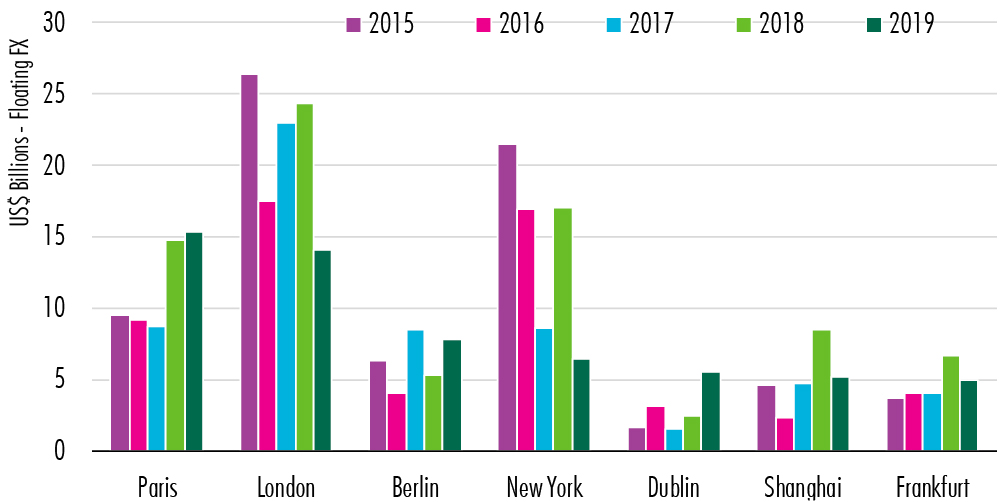

Global cross-border investment volume rebounded slightly in Q4, but still declined 7% year-over-year. Full-year cross-border investment fell by 20% from 2018--a banner year with three of the five largest quarterly cross-border volumes on record. All three regions had declines in cross-border investment, led by the U.S. (-54%) due to slowing mergers-and-acquisitions activity. In Q4 alone, EMEA saw sizeable growth of 21% in cross-border investment. Paris was the top EMEA destination for foreign capital, after replacing London for the first time on record in Q3 2019. Dublin gained significant investor interest, particularly in Q4, likely on investor optimism regarding the Brexit deal.

International property consultant CBRE is reporting this week that global commercial real estate investment volume in Q4 of 2019, including entity-level deals, was nearly level (-0.5%) with Q4 2018, while full-year volume fell by 2% from 2018.

Regionally, EMEA had substantial investment activity in Q4 of 2019, up by 19% year-over-year and compensating for subdued activity in the previous three quarters. Americas investment volume fell by 6% year-over-year in Q4, while APAC saw a 27% decrease.

2019 Global CRE Market FAQs:

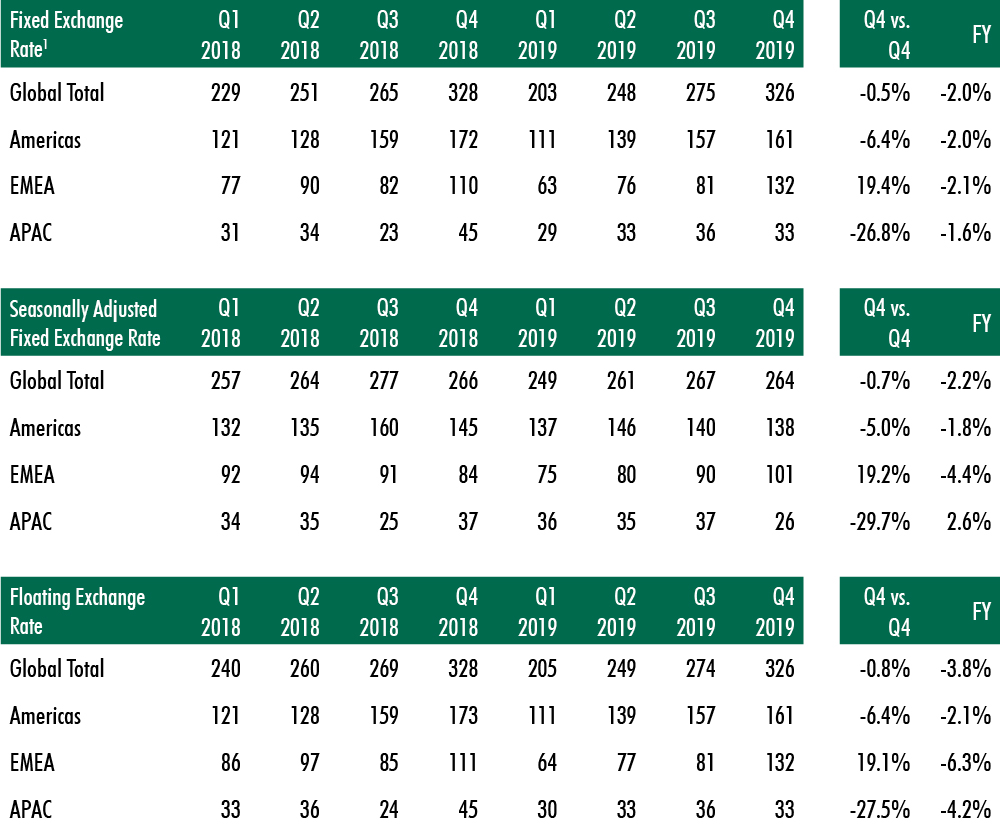

- Global commercial real estate (CRE) investment, including entity-level deals, totaled US$326 billion in Q4 2019, about level (-0.5%) with Q4 2018. For the full year, global volume was down slightly (-2%) from 2018.

- Excluding entity-level deals, global CRE investment volume rose by 9% year-over-year in Q4 to US$324 billion. Full-year global volume, excluding entity-level deals, was up by 5% from 2018.

- EMEA investment activity surged by 19% year-over-year in Q4, with high levels of investment throughout the region.

- In EMEA, Paris emerged as the top destination for foreign capital in 2019. Dublin also gained significant interest from foreign investors.

The U.S. accounted for nearly half of global CRE investment volume in 2019. Despite constrained global market supply, low global bond yield expectations and falling hedging costs, investors should continue to favor U.S. CRE, as well as fuel a possible recovery of the mergers-and-acquisitions market.

EMEA investment volume grew by 19% year-over-year in Q4, while full-year volume fell by 2% to $352 billion. Q4 investment activity fell year-over-year in Spain (-44%) and France (-3%) but grew in the U.K. (27%) and Germany (55%). The U.K.'s full-year volume fell by 19%, largely due to prolonged political uncertainty regarding Brexit, while France (12%) and Germany (8%) saw their full-year volumes rise moderately and reach new highs. Other European markets continued to attract capital in 2019 despite historically low prime yields, with Ireland (58%), Sweden (56%), Austria (39%) and Italy (37%) all seeing double-digit full-year growth.

Big-ticket transactions and renewed investor confidence inflated investment volumes throughout Continental Europe, with deal sizes larger than $100 million increasing 9% year-over-year. Furthermore, office and residential assets remained the most attractive. Investment volumes throughout Europe remained high, with mergers-and-acquisitions deals remaining prevalent. Additionally, the European Central Bank's decision to lower interest rates and restart quantitative easing gave an added stimulus to investment volumes this quarter. In 2020, as Western European markets continue to return low yields, capital likely will look toward a recovering U.K. market and Central and Eastern Europe for higher returns on CRE investments.

APAC investment volume fell by 27% year-over-year in Q4, while full-year volume fell by 2% to $131 billion--above the five-year average of $125 billion. The decline in transaction volume was due to fewer big-ticket transactions than in Q4 2018 and a significant decline in Hong Kong investment volume due to ongoing political turmoil. Hong Kong's Q4 2019 volume was the lowest quarterly total since the global financial crisis in 2008.

Nevertheless, several key APAC markets had increased investment volume in H2 2019. Australia and China had increases from domestic investors, while investment volume in Korea reached a record high, with office and logistics assets in highest demand. Japan continued to attract capital in 2019 largely due to its attractive yield spread offering.

The outbreak of the Wuhan coronavirus poses negative risks to investment sentiment in the region, with Greater China expected to have a slow start in Q1 2020. Investors likely will reduce their pace of investment and wait to determine the full extent of the outbreak.

Global cross-border investment volume rebounded slightly in Q4, but still declined 7% year-over-year. Full-year cross-border investment fell by 20% from 2018--a banner year with three of the five largest quarterly cross-border volumes on record. All three regions had declines in cross-border investment, led by the U.S. (-54%) due to slowing mergers-and-acquisitions activity. In Q4 alone, EMEA saw sizeable growth of 21% in cross-border investment. Paris was the top EMEA destination for foreign capital, after replacing London for the first time on record in Q3 2019. Dublin gained significant investor interest, particularly in Q4, likely on investor optimism regarding the Brexit deal.

Source: CBRE

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More