Commercial Real Estate News

Commercial Real Estate Lending in U.S. Maintains Momentum in Q1

According to the latest research from CBRE, commercial real estate lending activity edged up in the first quarter of 2022, despite rising inflation and heightened geopolitical risks.

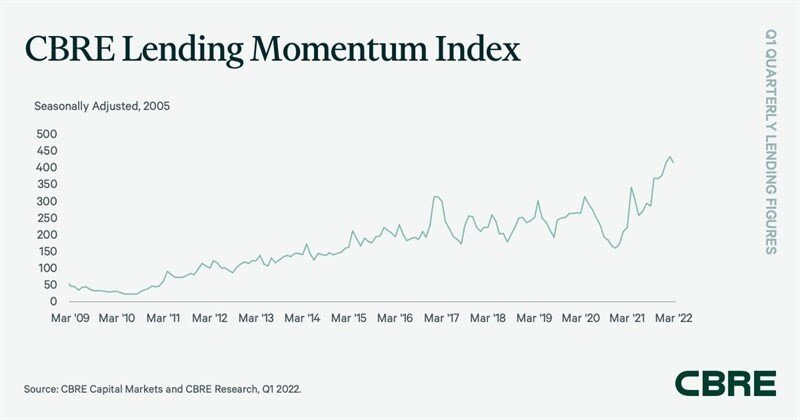

The CBRE Lending Momentum Index, which tracks the pace of CBRE-originated commercial loan closings in the U.S., increased by 69% year-over-year and 5.5% quarter-over-quarter, and is now 50% above its February 2020 pre-pandemic close. The index closed Q1 2022 at a value of 438.

"Lending activity continued to rise in Q1 2022, despite rising inflation, increased interest rates and the war in Ukraine. Following a strong start to the quarter, some lenders initially paused during the early onset of the war as credit spreads and loan indexes widened with the uncertainty. Many are very active again, quoting with generally wider spreads in line with corporate bonds," said Brian Stoffers, Global President of Debt & Structured Finance for Capital Markets at CBRE.

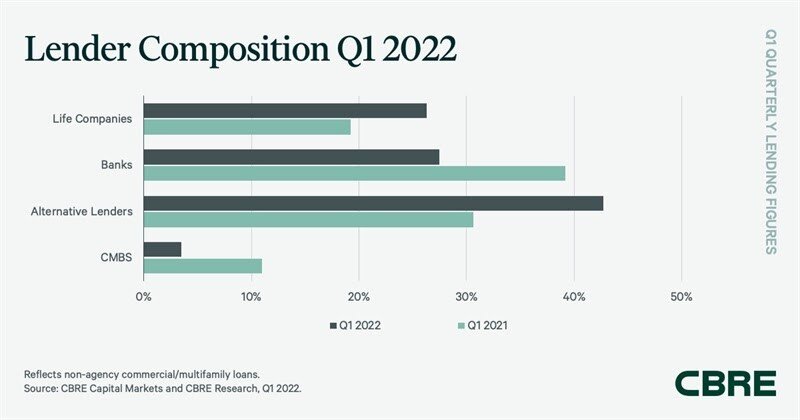

CBRE's lender survey indicates alternative lenders, such as debt funds and mortgage REITs, had the largest share of non-agency loan closings in Q1 2022 at 42.7%--up from 30.6% a year earlier. Transactions involving alternative lenders were primarily floating rate multifamily bridge loans with an average term to maturity of 43 months. Collateralized loan obligations (CLOs), which many alternative lenders use to term finance their loan portfolios, recorded $15.2 billion in issuance in Q1 2022--up from $8.9 billion in Q1 2021.

Banks were the second-most active lending group in Q1 2022, with 27.5% of loan closings in--down from 39.2% a year ago. Bridge and construction loans accounted for two-thirds of bank financing, while permanent loans accounted for the remaining one-third.

Life companies accounted for 26.3% of closed non-agency loans in Q1 2022--up from 19.2% a year ago. The majority were permanent fixed-rate loans with an average term to maturity of 108 months.

CMBS conduit loans accounted for the remaining 3.5% of non-agency loan volume in Q1 2022, down from 11% a year ago. Industry-wide CMBS issuance totaled $20.8 billion, double the amount of Q1 2021.

Loan underwriting criteria fell in Q1 2021. Underwritten cap rates and debt yields ticked down in Q1 2022 on slightly lower LTV ratios. A higher average mortgage interest rate caused the average loan constant to increase slightly. The percentage of loans carrying interest- only terms increased to 68.3% in Q1 from 62.5% in Q4 2021.

Government agency lending of multifamily assets totaled $30.9 billion in Q1 2022, down 12.9% from a year ago. CBRE's Agency Pricing Index, which reflects the average agency fixed mortgage rates for closed permanent loans with a seven- to 10-year term, increased by 20 bps in Q1 2022 and 30 bps from a year ago to average 3.48%.