The WPJ

Commercial Real Estate News

Reversing Course: U.S. Commercial Investment Capital Outflows Now Exceed Inflows

For the first time since 2014, says CBRE

With the longest global economic expansion on record, international commercial property investors now face an increasingly complex calculus in identifying cost-effective opportunities for potential downturn protection, and slowing cross-border capital flows.

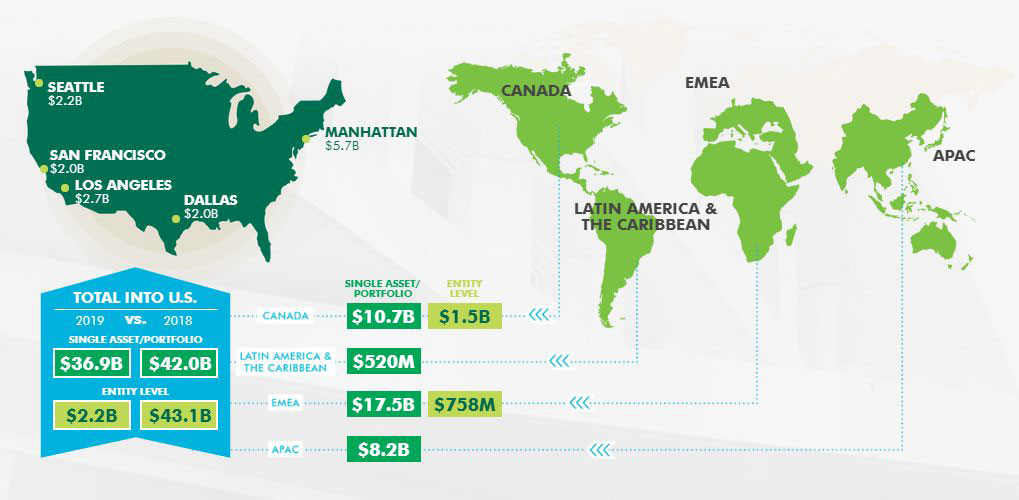

Because of such, CBRE is reporting this week that inbound capital to the U.S. dropped 54% in 2019, largely due to a sharp decrease in entity-level sales that tend to be highly volatile from year to year.

In 2018, rising U.S. interest rates and discounted REIT share prices contributed to entity-level sales' unprecedented 51% share of total inbound volume. But as these trends reversed in 2019, this share dropped to just 6%. Excluding entity-level transactions, 2019 inbound investment decreased by a more moderate 12.1%.

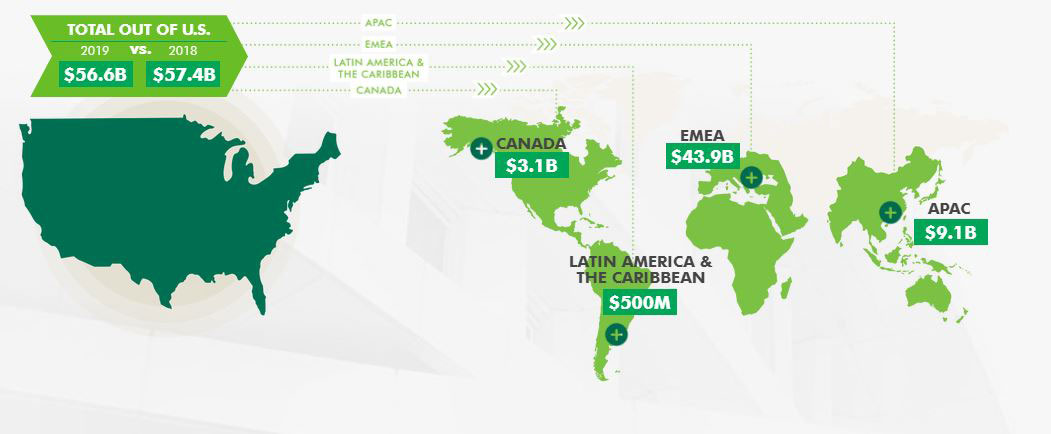

With U.S. capital outflows down by just 1% from 2018, the amount of capital that U.S. investors deployed in foreign real estate markets exceeded inbound capital by nearly $18 billion in 2019.

Sovereign wealth funds, insurance companies and pension funds (SWIP) together accounted for 30% of inbound volume in primary markets during H1 2019 compared with just 3% in secondary markets.

Foreign investors are also venturing into secondary and tertiary locations, though proximity to gateway markets is still preferred. Industrial hubs and demographic-driven multifamily markets are considered attractive now too.

Mirroring cross-border investment trends at home, the share of U.S. outbound investment in foreign multifamily and industrial assets has grown tremendously since the prior cycle. As these sectors expand, the share of total outbound capital devoted to office investment has declined the most.

U.S. investors deployed less capital to all top foreign destinations in H1 2019 than they did in H1 2018, with the exception of the U.K. However, large shifts in outbound volume to these countries have been the norm in the current cycle.

Although U.S. outbound investment to many of the typical top destination countries has slowed, certain markets within those countries like Helsinki, Osaka, Barcelona, Berlin and Shanghai continue to register significant volume growth.

With the longest global economic expansion on record, international commercial property investors now face an increasingly complex calculus in identifying cost-effective opportunities for potential downturn protection, and slowing cross-border capital flows.

Because of such, CBRE is reporting this week that inbound capital to the U.S. dropped 54% in 2019, largely due to a sharp decrease in entity-level sales that tend to be highly volatile from year to year.

In 2018, rising U.S. interest rates and discounted REIT share prices contributed to entity-level sales' unprecedented 51% share of total inbound volume. But as these trends reversed in 2019, this share dropped to just 6%. Excluding entity-level transactions, 2019 inbound investment decreased by a more moderate 12.1%.

With U.S. capital outflows down by just 1% from 2018, the amount of capital that U.S. investors deployed in foreign real estate markets exceeded inbound capital by nearly $18 billion in 2019.

Sovereign wealth funds, insurance companies and pension funds (SWIP) together accounted for 30% of inbound volume in primary markets during H1 2019 compared with just 3% in secondary markets.

Foreign investors are also venturing into secondary and tertiary locations, though proximity to gateway markets is still preferred. Industrial hubs and demographic-driven multifamily markets are considered attractive now too.

Mirroring cross-border investment trends at home, the share of U.S. outbound investment in foreign multifamily and industrial assets has grown tremendously since the prior cycle. As these sectors expand, the share of total outbound capital devoted to office investment has declined the most.

U.S. investors deployed less capital to all top foreign destinations in H1 2019 than they did in H1 2018, with the exception of the U.K. However, large shifts in outbound volume to these countries have been the norm in the current cycle.

Although U.S. outbound investment to many of the typical top destination countries has slowed, certain markets within those countries like Helsinki, Osaka, Barcelona, Berlin and Shanghai continue to register significant volume growth.

Source: CBRE

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More