The WPJ

Residential Real Estate News

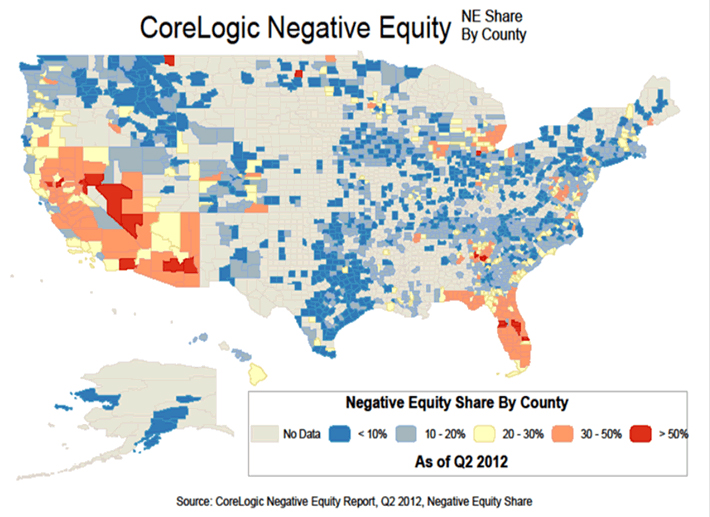

Negative Equity Slows in Q2, Over 600,000 U.S. Homeowners With Mortgage Now Above Water Again

This is down from 11.4 million properties, or 23.7 percent, at the end of the first quarter of 2012. An additional 2.3 million borrowers possessed less than 5 percent equity in their home, referred to as near-negative equity, at the end of the second quarter. Approximately 600,000 borrowers reached a state of positive equity at the end of the second quarter of 2012, adding to the more than 700,000 borrowers that moved into positive equity in the first quarter of this year.

Negative equity, often referred to as "underwater" or "upside down," means that borrowers owe more on their mortgages than their homes are worth. Negative equity can occur because of a decline in value, an increase in mortgage debt or a combination of both.

Together, negative equity and near-negative equity mortgages accounted for 27.0 percent of all residential properties with a mortgage nationwide in the second quarter, down from 28.5 percent at the end of the first quarter in 2012. Nationally, negative equity decreased from $691 billion at the end of the first quarter in 2012 to $689 billion at the end of the second quarter, a decrease of $2 billion driven in large part by an improvement in house price levels.

Most borrowers in negative equity are continuing to pay their mortgages. The share of borrowers that were underwater and current on their payments was 84.9 percent at the end of the second quarter in 2012. This is up from 84.8 percent at the end of the first quarter in 2012.

"The level of negative equity continues to improve with more than 1.3 million households regaining a positive equity position since the beginning of the year," said Mark Fleming, chief economist for CoreLogic. "Surging home prices this spring and summer, lower levels of inventory, and declining REO sale shares are all contributing to the nascent housing recovery and declining negative equity."

"Nearly 2 million more borrowers in negative equity would be above water if house prices nationally increased by 5 percent," said Anand Nallathambi, president and CEO of CoreLogic. "We currently expect home prices to continue to trend up in August. Were this trend to be sustained we could see significant reductions in the number of borrowers in negative equity by next year."

Report Highlights as of Q2 2012:

- Nevada had the highest percentage of mortgaged properties in negative equity at 59 percent, followed by Florida (43 percent), Arizona (40 percent), Georgia (36 percent) and Michigan (33 percent). These top five states combined account for 34.1 percent of the total amount of negative equity in the U.S.

- Of the total $689 billion in aggregate negative equity, first liens without home equity loans accounted for $339 billion aggregate negative equity, while first liens with home equity loans accounted for $353 billion.

- Of the 10.8 million upside-down borrowers, 6.6 million hold first liens without home equity loans. The average mortgage balance for this group of borrowers is $216,000, the average underwater amount is $51,000, and the cumulative underwater value accounts for 18 percent of all negative equity.

- 4.2 million upside-down borrowers possess both first and second liens. The average mortgage balance for this group of borrowers is $300,000, the average underwater amount is $84,000 and the cumulative underwater amount accounts for 38 percent of all negative equity.

- Approximately 41 percent of borrowers with first liens without home equity loans had loan-to-value (LTV) ratios of 80 percent or higher and approximately 60 percent of borrowers with first liens and home equity loans had combined LTVs of 80 percent or higher.

- At the end of the second quarter 2012, just over 17 million borrowers possessed qualifying LTVs between 80 and 125 percent for the Home Affordable Refinance Program (HARP) under the original requirements first introduced in March 2009. The lifting of the 125 percent LTV cap via HARP 2.0 opens the door to another 5 million borrowers.

- The bulk of negative equity is concentrated in the low end of the housing market. For example, for low-to-mid value homes (less than $200,000), the negative equity share is 32 percent, almost twice the 17 percent for borrowers with home values greater than $200,000.

- As of Q2 2012, there were 1.8 million borrowers who were only 5 percent underwater. If home prices continue increasing over the next year, these borrowers could move out of a negative equity position.

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More