Residential Real Estate News

Federal Reserve Delivers First Rate Cut of 2025 as Mortgage Relief Proves Limited

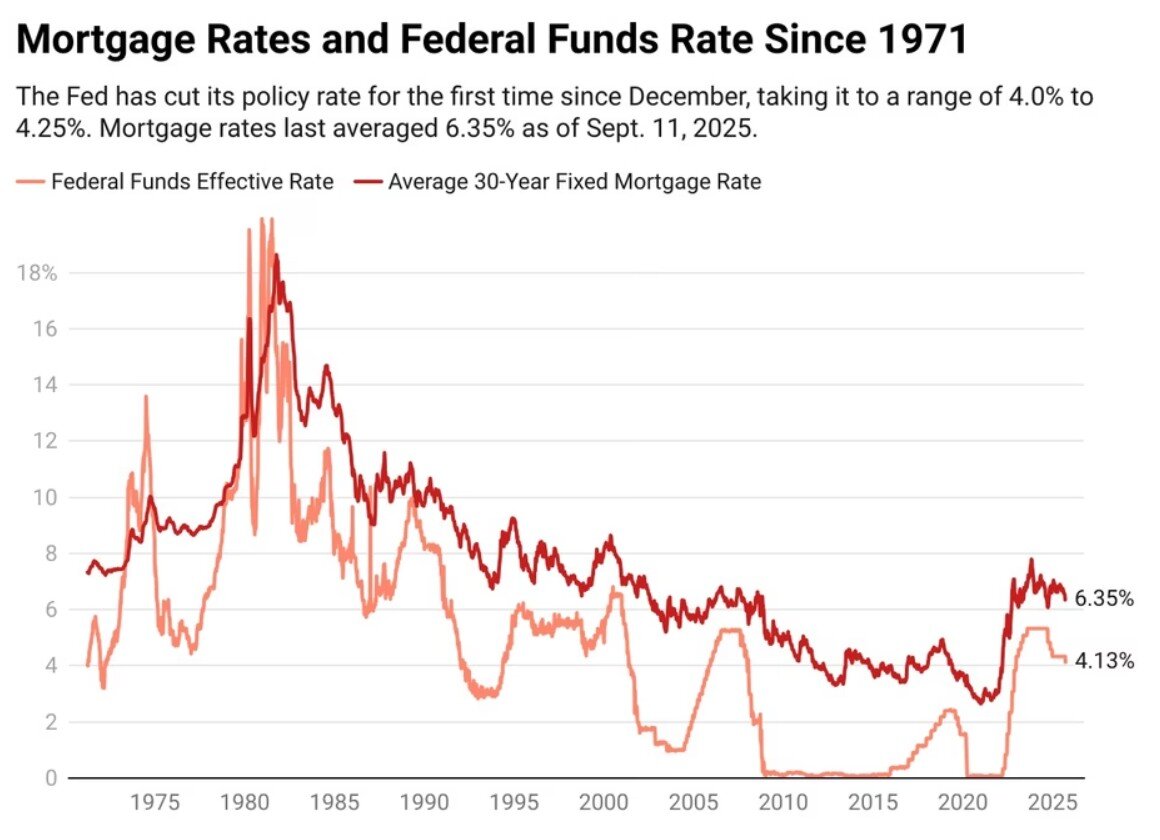

The Federal Reserve lowered interest rates for the first time in nine months this week, trimming its benchmark federal funds rate by a quarter percentage point to a range of 4% to 4.25%. The widely expected move comes as policymakers seek to ease borrowing costs that have strained households and businesses across the economy.

The decision, backed by Fed Chair Jerome Powell and 11 members of the Federal Open Market Committee (FOMC), was not unanimous. Stephen Miran, President Donald Trump's newly appointed Fed governor who was sworn in just a day earlier, cast the lone dissenting vote, calling for a steeper half-point reduction.

While the federal funds rate doesn't directly set consumer borrowing costs, it influences everything from credit card APRs to auto and small business loans. Mortgage rates are more closely tied to Treasury yields and broader market conditions, but they have already retreated in recent months. The average 30-year fixed mortgage stood at 6.13% as of Sept. 16, down from over 7% in January and near an 11-month low, according to Freddie Mac.

For most homeowners, however, the impact will be muted. Those with fixed-rate mortgages won't see lower payments unless they refinance or move. And housing economists caution that prospective buyers should not expect mortgage rates to fall much further solely because of Wednesday's Fed action. Many analysts expect borrowing costs to remain above 6% through the end of the year.

Markets responded swiftly to the policy shift. The S&P Homebuilders Select Industry Index, a gauge of leading U.S. homebuilder shares, climbed more than 2% on the decision, reflecting optimism that lower financing costs could support housing demand.

Still, the trajectory for mortgage rates -- and the broader economy -- will hinge less on a single quarter-point cut and more on how aggressively the Fed signals its willingness to ease policy in the months ahead.