The WPJ

Commercial Real Estate News

Asia Property Bond Market Enjoys Strong Momentum from Stock Market Volatility

Chinese Developers Delay Bond Maturity, Debt to Peak in 2020

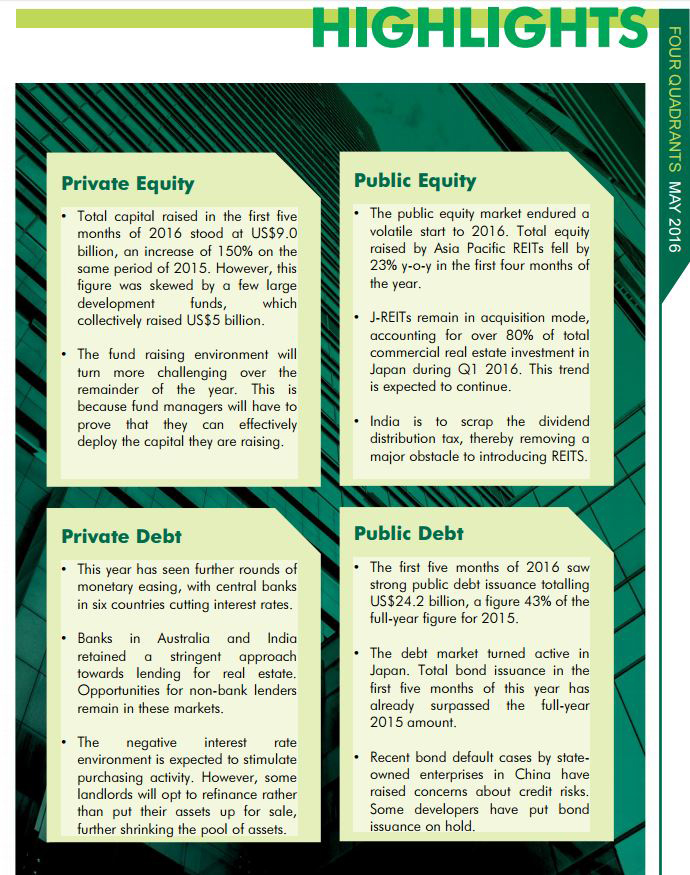

According to CBRE's second-edition of Four Quadrants Asia Pacific, a report that provides a comparative review on the 'four quadrants' of private equity, public equity, private debt and public debt, as several interest rate cuts were recorded across the region, debt financing turned more active while the equity funding market slowed down.

After a record-year of bond issuance by real estate companies in Asia Pacific--reaching $55.7 billion in 2015--the strong momentum continued in the first five months of 2016, registering $24.2 billion, 43% of the total full-year figure in 2015.

For the same period, REIT fund raising (excluding IPO), amounted to $2 billion, a decline of 23% year-over-year, which was impacted by stock market volatility witnessed at the start of the year. For the private equity quadrant, close-ended real estate fund raising reached $9 billion, a substantially increase from $3.2 billion for the same period in 2015. However, the total amount raised was skewed by two logistics development in China and Japan, which collectively raised $3.5 billion.

"The debt market in Asia Pacific is overall demonstrating increased activity, mainly due to further monetary easing from central banks as six countries--Australia, India, Indonesia, Japan, New Zealand and Taiwan--cut their rates in the first five months of the year," said Ada Choi, Senior Director, Research, CBRE Asia Pacific. "The active real estate bond market was mainly driven by the negative interest rate in Japan and the opening of the onshore bond market in China."

The Japanese bond issuance market registered an uptick of $3.2 billion during the review period, yet Chinese developers remain the biggest source accounting for over 70% of the overall total of $24 billion public bonds issued, mostly in mainland China.

"In Japan, with the implementation of the negative interest rate policy by the Bank of Japan, government bond yields turned negative, making bond offerings a more attractive fundraising method for investors. This boosted bond raising activity in the market, particularly from J-REITs as they turned more active in accessing capital from the bond market since the cost of financing is so low. Whilst in China, on the back of a weaker RMB and looser approval processes by the government, Chinese developers turned more active in the domestic bond market, shifting to issuing more onshore bonds than offshore bonds. Developers can access capital with a lower interest rate from the domestic bond market compared to offshore bonds," Ms. Choi added.

Nevertheless, investor sentiment towards Chinese bonds has been negatively impacted by recent bond default cases by state-owned enterprises. This has caused some developers to put bond issuance on hold, which will likely result in slower bond issuance for the rest of the year. However, Chinese developers have less pressure to repay their debt in the short term as they have pushed back their debt maturity to 2020, with around $28 billion expected to be settled by developers.

Appetite of Bank Lending Diverges; Non-bank Lending Opportunities Remain in Australia, India

In an environment of lower interest rates and accommodative monetary policy by central banks, lending conditions in general remain positive for investors and developers as some banks, such as in China and Japan, are relaxing their stance for loan approvals on the back of strong liquidity in the banking system. In Hong Kong, despite a more aggressive stance on lending to commercial real estate investment, banks are adopting a more conservative approach for residential development projects given softening prices in the housing market.

"The appetite for bank lending is diverging across the region as Australia and India retain a more stringent approach towards lending for real estate development and investment, despite the policy rate cuts," commented Nick Crockett, Executive Director, Capital Advisors, CBRE Asia Pacific.

"The high level of bad debt makes Indian banks reluctant to lend whilst in Australia, banks face higher levels of capital requirement from their regulators, which will likely increase their funding cost and erode profit margins. Banks in Australia are also pulling back from lending to overseas buyers of residential purchases, which was a major driver in support of the Australian residential market. Since projects have already started, developers will continue to require funding to finish these projects. This will continue to provide opportunities for non-bank lending in both India and Australia," he said.

In regards to the private equity market, the remainder of the year will become more challenging as fund managers will have to first prove they can effectively deploy the capital being raised, meeting their funds' target returns.

"The lack of investable assets, coupled with investors' increasing interest in real estate debt investment, has prompted fund managers to establish real estate debt focused funds. There are still a number of debt funds raising capital, most of which are focusing on debt opportunities in residential development projects in Australia and India," added Mr. Crockett.

Real Estate Listings Showcase

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More