Commercial Real Estate News

Commercial Cap Rates Edge Lower in U.S., Hinting at Market Turn

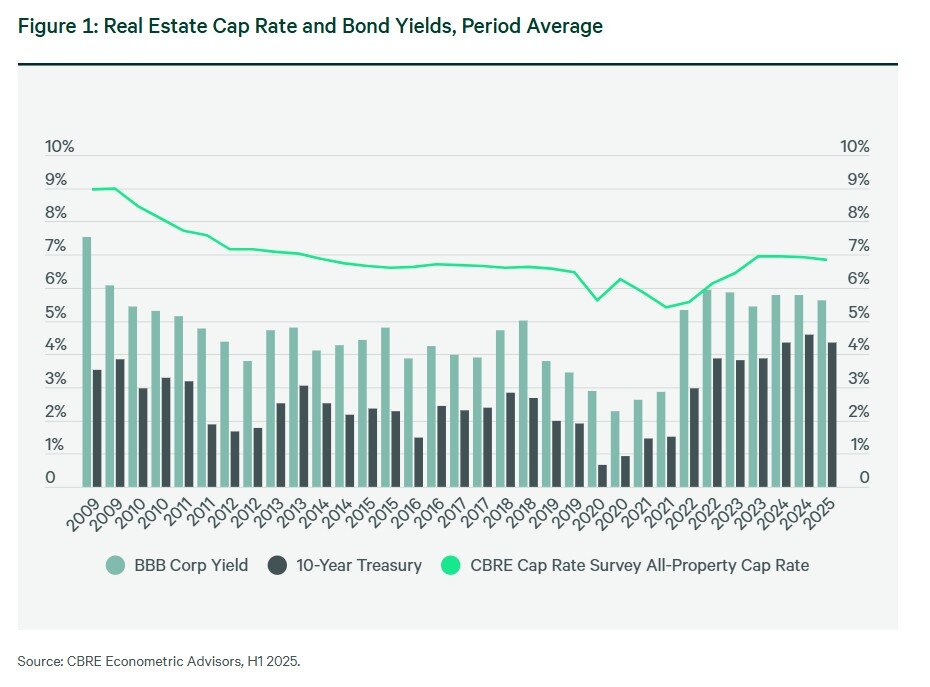

U.S. commercial real estate cap rates edged lower in the first half of 2025, suggesting that yields may have peaked after two years of steady expansion, according to CBRE's latest Cap Rate Survey.

The all-property cap rate fell by 9 basis points from late 2024 levels, with movement across most asset classes pointing to broad stabilization. Unlike prior surveys, which showed divergence among sectors, this round reflected relatively uniform shifts, a signal that pricing may be entering an early phase of yield compression despite persistent macroeconomic uncertainty.

Treasury market turbulence shaped the backdrop. The 10-year yield surged to nearly 4.8% in mid-January before dropping to 4.3% in March, then whipsawed again following the Biden administration's surprise April tariff package. Yields briefly collapsed as equities sold off, only to rebound after the measures were paused and Moody's downgraded U.S. sovereign debt. By the end of June, the 10-year was trading near 4.2%.

Office valuations remain the outlier. While the average office cap rate did not increase, spreads between upper and lower estimates widened further, underscoring investor uncertainty, particularly for Class B and C properties.

By contrast, multifamily has overtaken industrial as the favored long-term performer, while retail continues to show resilience. Regional trends were muted, with cap rates largely stable across major metros.

Key Takeaways from CBRE's H1 2025 Survey:

- Cap Rate Shift: All-property yields declined 9 bps, marking potential inflection from cyclical peak.

- Macro Headwinds: Rate volatility and trade policy shocks weighed on confidence, complicating deal flow.

- Sector Divergence: Multifamily leads in outlook; industrial moderates; retail stable; office still under pressure.

- Risk Signals: Wider valuation spreads for secondary office assets highlight elevated downside risk.