The WPJ

Residential Real Estate News

Fort Lauderdale, Las Vegas, San Francisco Had Most Dramatic Housing Shifts in Last Decade

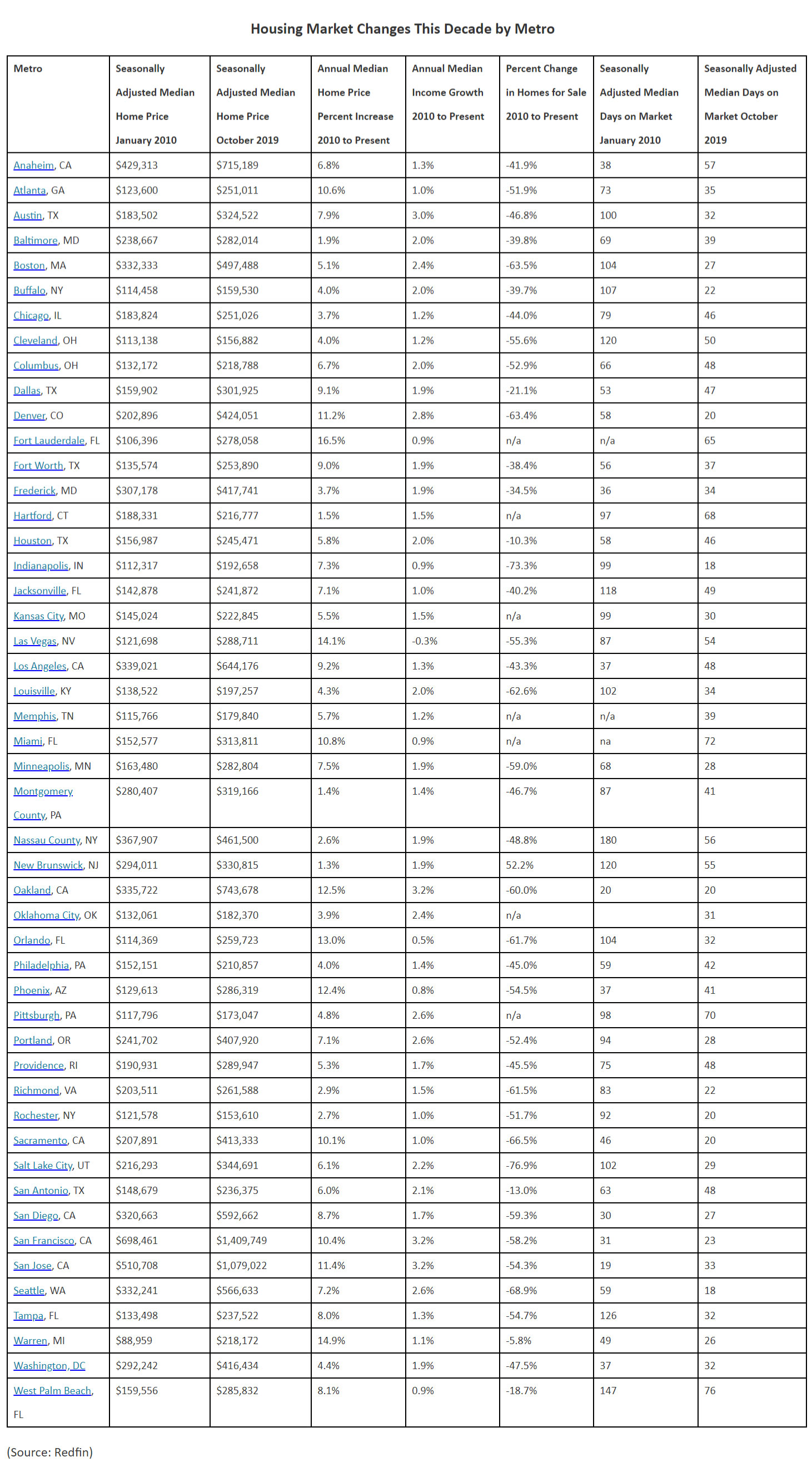

According to a new report from Redfin, Fort Lauderdale, Las Vegas, San Francisco, Salt Lake City, and Nassau County, NY experienced the most dramatic housing shifts since 2010.

"The housing market is ending the decade in a vastly different place than it began," said Redfin chief economist Daryl Fairweather. "In 2010, the market was in the middle of its greatest downturn in history: Home values were plummeting and the share of mortgages in delinquency was at an all time high. Heading into 2020, home values have recovered along with the economy, and now many parts of the country are grappling instead with new challenges like high home prices and a lack of homes for sale."

Highest percent increase in home prices: Fort Lauderdale

Florida was one of the epicenters of the foreclosure crisis and experienced some of the biggest declines in home values leading up to 2010. But as the sunshine state recovered from the housing crash, home values also increased, leading to the nation's largest post-crisis recovery. In Fort Lauderdale, the median home price increased 161% from $106,000 at the beginning of 2010 to $278,000 at the end of 2019. The median home price has more than doubled this decade in Orlando (+127%) and Miami (+106%) as well.

Biggest contrast between increase in home prices and decline in incomes: Las Vegas

Las Vegas, where incomes fell dramatically during the great recession and haven't yet fully recovered, saw the biggest divergence between home prices and incomes. In Las Vegas, the median home price increased at an average annual rate of 14.1% over the decade, while the median income declined at an average annual rate of 0.4%. As incomes fell, residents could no longer afford to own a home, which caused a simultaneous decline in the homeownership rate from 59% in 2010 to a low of 52% in 2016, followed by a slight increase to 53% as of 2017. Even though the homeownership rate remains low, demand from investors looking to rent out or flip homes has supported high home price growth.

Largest dollar value jump in home prices: San Francisco

Eight out of the nation's top 10 metros for home price increases in dollar value were in California. In San Francisco, the median home price increased $711,000--from $698,000 at the beginning of 2010 to $1.4 million by the end of 2019. Two main factors led to San Francisco's large price gains: a booming job market and a lack of homes for sale. By 2015, the unemployment rate in San Francisco was just 3.7% compared to 5.3% for the nation. By October, 2019, the city's unemployment rate was 1.9%. At the same time, there are not enough housing units for all the workers in San Francisco, a reality true across California where home prices have risen dramatically in the last decade.

Steepest drop in home supply: Salt Lake City

Inventory declined by 77% in Salt Lake City over the course of the decade, due to the fact that Salt Lake City homeowners are staying in their homes longer than usual. The typical Salt Lake City homeowner had spent 23 years in their home in 2019, versus 15 years in 2010. The number of homes for sale declined this decade in 95% of the markets we analyzed. The decline in homes for sale has made homebuying much more competitive than it was at the beginning of the decade. Currently, one in three Salt Lake City homes sell for above list price, compared to less than one in four homes at the start of the decade.

Greatest decline in days on market: Long Island's Nassau County

In Nassau County, the median time it takes to sell a home dropped by about four months--124 days--over the course of the decade. At the beginning of 2010 it typically took 180 days to sell a home; it now takes just 56 days. "During the housing crash there were a lot of short sales in Long Island, which are very difficult to close. I don't see that at all anymore," said Redfin agent Peggy Papazaharias. "In the last several years, prices sky-rocketed in Manhattan, which pushed many homebuyers to consider Long Island, and now demand is very strong."

"The housing market is ending the decade in a vastly different place than it began," said Redfin chief economist Daryl Fairweather. "In 2010, the market was in the middle of its greatest downturn in history: Home values were plummeting and the share of mortgages in delinquency was at an all time high. Heading into 2020, home values have recovered along with the economy, and now many parts of the country are grappling instead with new challenges like high home prices and a lack of homes for sale."

Highest percent increase in home prices: Fort Lauderdale

Florida was one of the epicenters of the foreclosure crisis and experienced some of the biggest declines in home values leading up to 2010. But as the sunshine state recovered from the housing crash, home values also increased, leading to the nation's largest post-crisis recovery. In Fort Lauderdale, the median home price increased 161% from $106,000 at the beginning of 2010 to $278,000 at the end of 2019. The median home price has more than doubled this decade in Orlando (+127%) and Miami (+106%) as well.

Biggest contrast between increase in home prices and decline in incomes: Las Vegas

Las Vegas, where incomes fell dramatically during the great recession and haven't yet fully recovered, saw the biggest divergence between home prices and incomes. In Las Vegas, the median home price increased at an average annual rate of 14.1% over the decade, while the median income declined at an average annual rate of 0.4%. As incomes fell, residents could no longer afford to own a home, which caused a simultaneous decline in the homeownership rate from 59% in 2010 to a low of 52% in 2016, followed by a slight increase to 53% as of 2017. Even though the homeownership rate remains low, demand from investors looking to rent out or flip homes has supported high home price growth.

Largest dollar value jump in home prices: San Francisco

Eight out of the nation's top 10 metros for home price increases in dollar value were in California. In San Francisco, the median home price increased $711,000--from $698,000 at the beginning of 2010 to $1.4 million by the end of 2019. Two main factors led to San Francisco's large price gains: a booming job market and a lack of homes for sale. By 2015, the unemployment rate in San Francisco was just 3.7% compared to 5.3% for the nation. By October, 2019, the city's unemployment rate was 1.9%. At the same time, there are not enough housing units for all the workers in San Francisco, a reality true across California where home prices have risen dramatically in the last decade.

Steepest drop in home supply: Salt Lake City

Inventory declined by 77% in Salt Lake City over the course of the decade, due to the fact that Salt Lake City homeowners are staying in their homes longer than usual. The typical Salt Lake City homeowner had spent 23 years in their home in 2019, versus 15 years in 2010. The number of homes for sale declined this decade in 95% of the markets we analyzed. The decline in homes for sale has made homebuying much more competitive than it was at the beginning of the decade. Currently, one in three Salt Lake City homes sell for above list price, compared to less than one in four homes at the start of the decade.

Greatest decline in days on market: Long Island's Nassau County

In Nassau County, the median time it takes to sell a home dropped by about four months--124 days--over the course of the decade. At the beginning of 2010 it typically took 180 days to sell a home; it now takes just 56 days. "During the housing crash there were a lot of short sales in Long Island, which are very difficult to close. I don't see that at all anymore," said Redfin agent Peggy Papazaharias. "In the last several years, prices sky-rocketed in Manhattan, which pushed many homebuyers to consider Long Island, and now demand is very strong."

Real Estate Listings Showcase

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More