Commercial Real Estate News

Multifamily Oversupply in U.S. Expected To Be Short-Lived

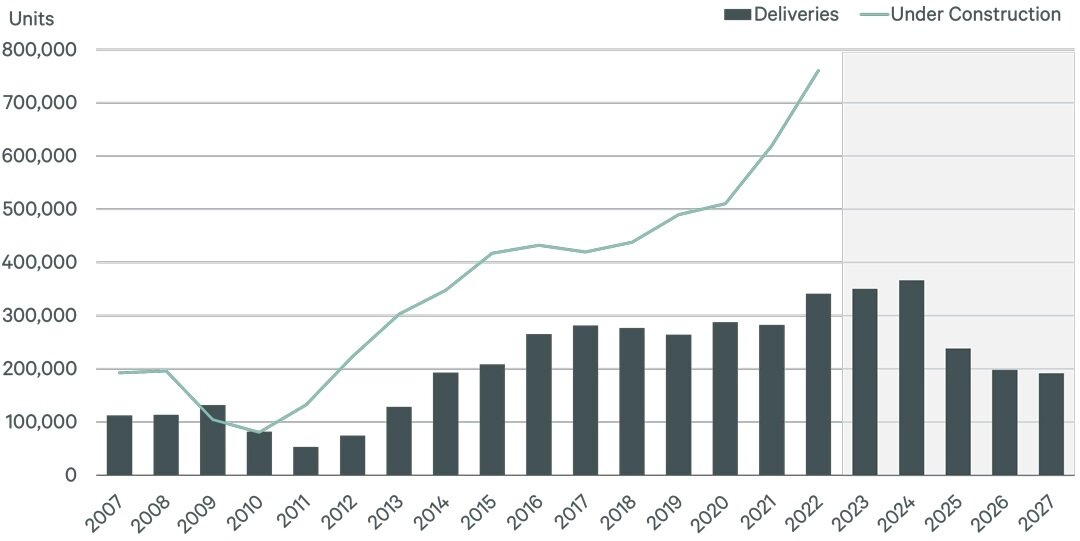

According to the latest research from CBRE, while the delivery of a near-record 716,000 new multifamily housing units in the U.S. over the next two years will create a short-term oversupply, the new supply is needed to keep long-term fundamentals healthy in the sector.

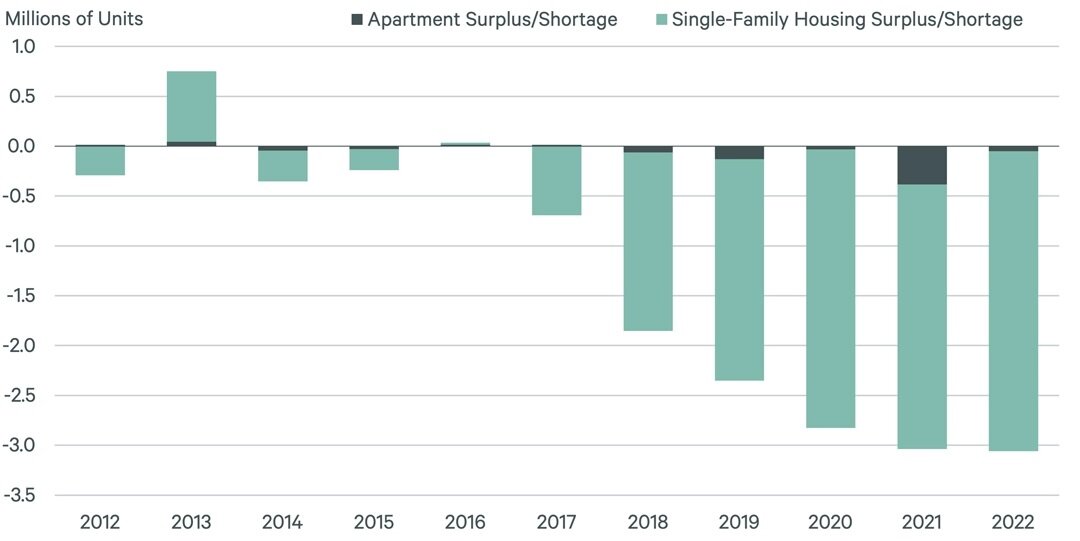

The surge in construction is expected to push the multifamily sector's overall vacancy rate above equilibrium to a peak of 5.2% from 4.6% by year-end. While this may be surprising, given the overall housing shortage in the U.S., the lack of supply is predominantly in single-family homes and not multifamily units. CBRE expects that demand for rental housing will gain momentum this year as vacancy peaks only slightly above its long run average of 5.0%.

Even with a surplus of multifamily units over the short-term, CBRE forecasts that an additional 2.3 million new units will be needed nationwide to maintain healthy market fundamentals over the next 10 years. Once the largest portion of the delivery wave has concluded through 2024, the U.S. will still need nearly 200,000 additional units annually to maintain proper supply and demand balance.

"While a multifamily development surplus in the next 18 months may weigh on market fundamentals in the short-term, new deliveries will be limited beginning in 2025 and will ultimately lay the foundation for a healthy market throughout the next cycle," said Kelli Carhart, leader of Multifamily Capital Markets for CBRE in the U.S.

More than 750,000 multifamily units are currently under construction in the U.S.--the highest amount since the housing boom of the 1980s. Most of these new units are in markets such as Dallas, Austin and Atlanta that experienced the greatest in-migration during the COVID-19 pandemic. Although population growth in these markets is beginning to slow, the rapid increase in construction costs due to inflation and supply chain disruptions has caused multifamily starts to slow as well--meaning that the construction peak is likely occurring now.

The current wave in construction is expected to expand total multifamily inventory in the U.S. by 4.2% over the next two years. Although the sector has recorded negative net absorption--the net change in the total number of apartments leased--over the past three quarters, demand is expected to turn positive in the first half of 2023 and limit the extent to which rising vacancies could slow rent growth. While CBRE expects rent growth of 3.5% for the year--down from 6.7% in 2022 and 13.4% in 2021--this is still relatively healthy when compared with the long-run average of 2.5%

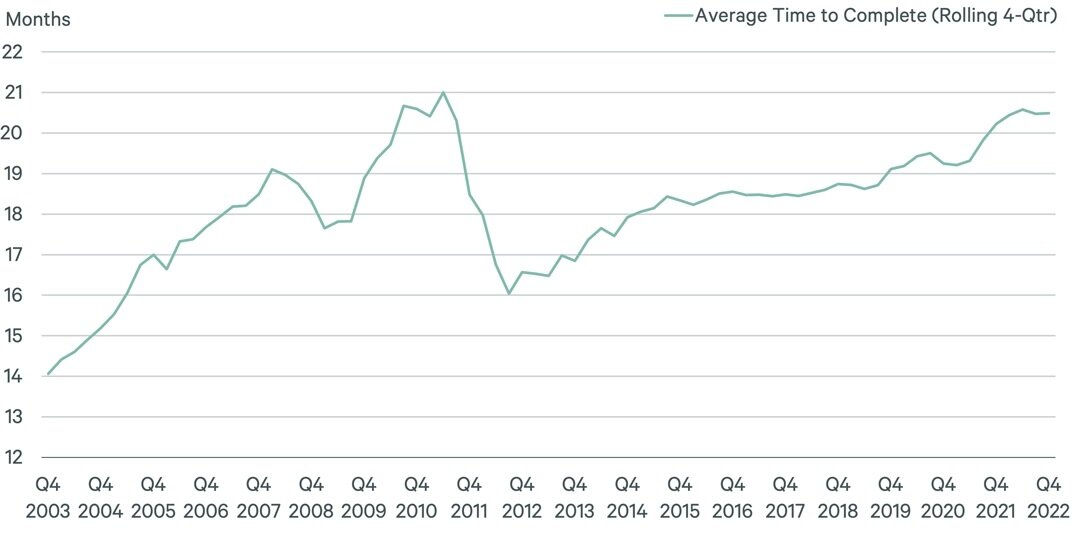

As the market returns to equilibrium, the potential for construction delays and extended timelines due to ongoing labor shortages could also limit the rise in vacancies. Early in the current construction cycle (2013) when the pipeline was approximately 300,000 units (less than half the amount today), the average time of construction from start to finish averaged 16.5 months. Today, that timeline averages 20.5 months--nearly 25% longer. The biggest jump in that expanded timeline occurred in 2021, when units under construction ramped up tremendously.