Residential Real Estate News

Housing Inventory Down 40 Percent from pre-COVID Levels in U.S.

According to Zillow, the housing market appears to already be in full swing in 2022, as anxious buyers outnumbered dwindling new listings and drove inventory to record low levels in December 2021. Limited supply is already pushing price growth up, as Zillow's latest market report shows monthly home value appreciation accelerated for the first time since July 2021.

In addition to not wanting to wade into such a tight market as a buyer, homeowners could be hesitant to list their houses and move due to a resurgence in coronavirus cases and employers' rising uncertainty about post-pandemic working arrangements, according to a recent Zillow survey.

"Home shoppers picked the shelves clean this December, leaving fewer active listings than ever before in the U.S. housing market," said Jeff Tucker, senior economist at Zillow. "Enough determined buyers kept up their house hunt to reignite monthly price appreciation. Rising mortgage rates could be the next potential headwind, but demand has proven persistent; neither high prices nor slim inventories have deterred buyers so far."

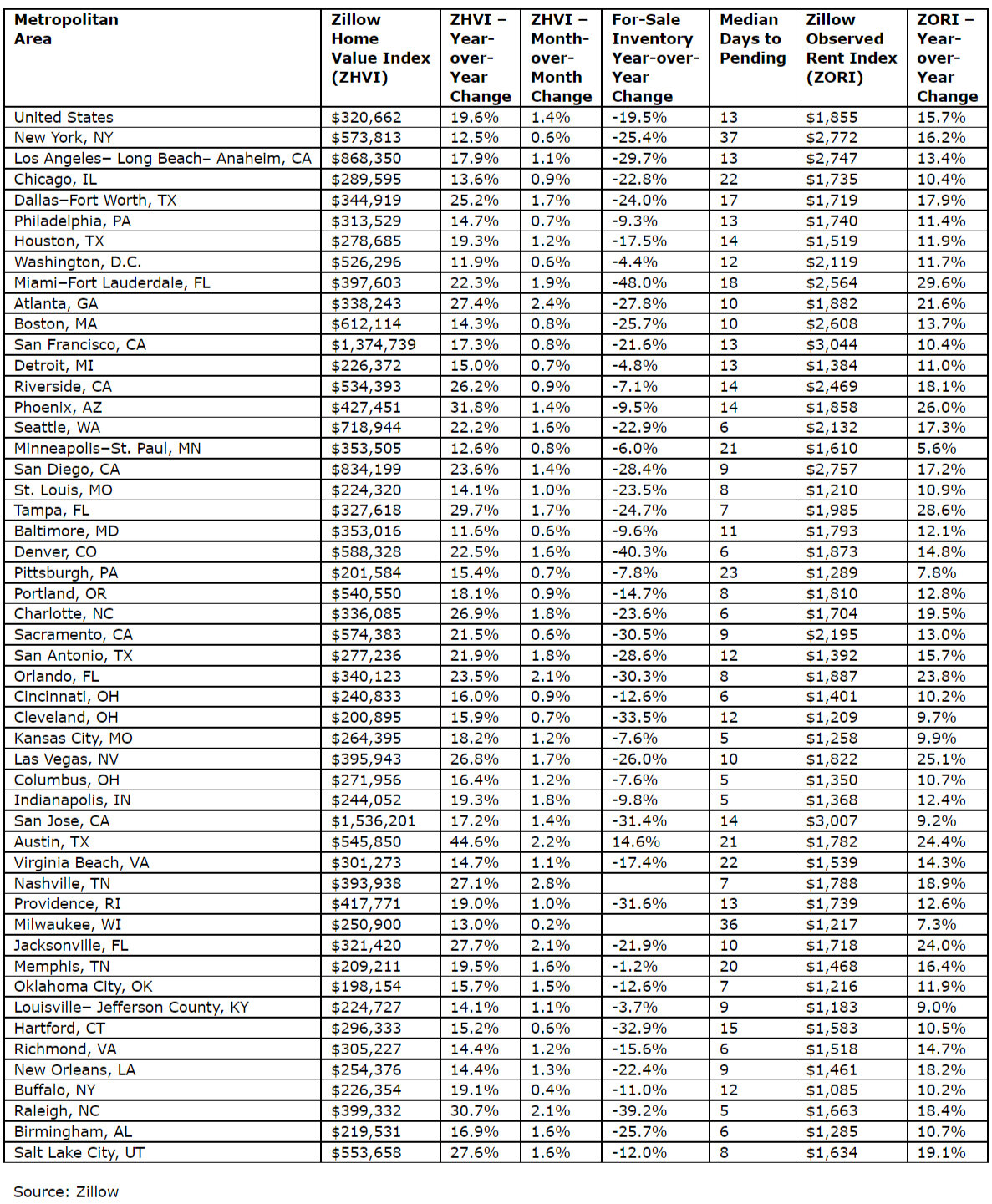

The typical home value is now $320,662, 19.6% above that of December 2020. The annual growth rate represents an all-time high in data dating back more than 20 years. After decelerating since July, month-over-month home value appreciation reignited, jumping from 1.2% in November to 1.4% in December.

The resurgent upward pressure on prices is likely due to astonishingly low levels of inventory this winter. After slipping in November, inventory plunged in December, dropping 11.1% in a month to a new record low of about 923,000 homes. Buyers shopping in December had 19.5% fewer homes to choose from than they did a year before, when inventory was already at a record low. Compared to December 2019, there are now 40.5% fewer homes available for sale.

One bright point for buyers is that the speed of the market has gradually slowed since the frenzied summer. In June, the typical U.S. home spent just one week on the market before going under contract. That has risen every month since, to roughly 13 days in December. This is still an incredibly short time on the market, but those extra few days do give buyers more time to assess their options.

Surge in coronavirus cases could be hampering listings, plans to move

While December typically sees a sharp decline in newly listed inventory, the 18.9% monthly drop seen last month was the largest in the past three years. The rise of the omicron variant of coronavirus could be partially responsible, pushing homeowners to wait for infection rates to subside before listing.

Workers are also less certain about their long-term working arrangements, which could impact their plans to move. A December survey conducted by Zillow found that 52% of workers reported that their employer had announced post-pandemic work arrangements -- a lower share than was reported in June 2021. One possible explanation is that the rise of new coronavirus variants has caused employers to push back in-person start dates indefinitely.

Workers whose employer has announced post-pandemic work arrangements are more likely to say they are considering a move within the next three years: 51%, versus 41% for those whose employers have not lined out a plan.

Rent growth slows

Typical rents rose a record 15.7% year over year in December, to $1,855 per month. However, monthly growth was 0.7% in December, the lowest monthly growth seen since February.

Rents grew year over year in all 50 of the nation's largest metros. Annual rent appreciation was fastest across the Sunbelt, led by Miami (29.6%), Tampa (28.6%), Phoenix (26.0%) and Las Vegas (25.1%).