Commercial Real Estate News

Rents Hit 18-Year High in Tokyo as Japan's Office Market Defies Gravity

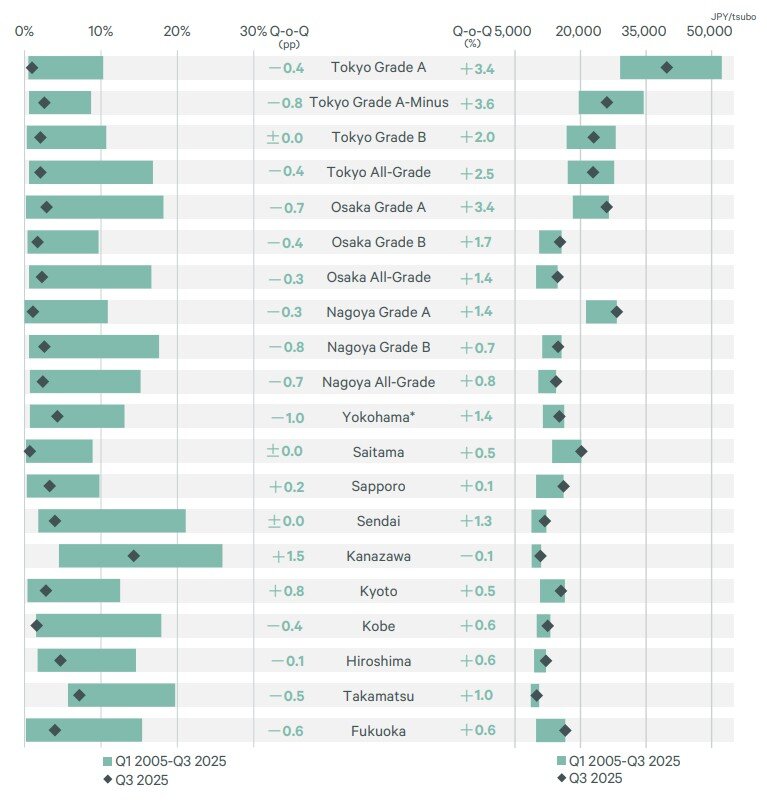

Japan's office market tightened further in the third quarter of 2025, with vacancies falling in half of the nation's major cities and rents climbing to record levels, according to a new report by CBRE. The data underscores a broad recovery in office demand across Japan's regional markets, led by strong absorption in Yokohama, Fukuoka, and Tokyo.

Vacancy Rates Decline Across Major Markets

CBRE reported that all-grade office vacancies declined quarter-over-quarter in five of the 10 cities surveyed, held steady in two, and rose in three. Yokohama once again posted the sharpest improvement, as its vacancy rate dropped by one percentage point to 4.3%. The decline was driven by relocations from company-owned properties and steady demand for expansion and new office openings.

Fukuoka followed with a 0.6-point drop to 4.0%, supported by several relocations into larger spaces exceeding 100 tsubo. Many tenants were moving temporarily to accommodate building redevelopments, while others upgraded or expanded operations--signs, CBRE said, of resilient underlying demand.

Among cities where vacancies increased, new supply was the main factor. Sapporo saw about 3,000 tsubo of new space enter the market, lifting vacancies slightly by 0.2 points, even as tenants continued upgrading into existing prime stock. Kanazawa recorded a 1.5-point increase as new supply equivalent to 3% of existing inventory exceeded take-up. In Kyoto, limited new supply opened fully leased, but downsizing and consolidations elsewhere caused vacancies to rise by 0.8 points.

Rents Climb in Nearly Every Market

Office rents rose in nine of the 10 surveyed cities, continuing a nationwide uptrend. Only Kanazawa posted a marginal decline. Yokohama, Sendai, and Takamatsu saw rents jump more than 1% quarter-over-quarter--the strongest gains in years. For Yokohama and Sendai, it marked their first such increases since early 2020 and late 2019, respectively.

Landlords lifted rents around Yokohama Station and Kannai, while in Sendai, newer high-grade buildings with little vacancy commanded higher rates. CBRE noted that "almost no properties reported lower rents nationwide," with Sapporo, Saitama, and Hiroshima each setting new record highs.

Tokyo Tightens Further as Rents Surge to 18-Year High

Tokyo's office market remains exceptionally tight. The all-grade vacancy rate fell 0.4 points to 2.1%, while Grade A vacancies dropped to just 1.0%. Strong tenant demand for limited large-floor plates pushed Grade A rents up 3.4% to approximately $1,075 per tsubo--marking the sharpest quarterly rise since 2007 and surpassing the pre-pandemic peak of about $1,055 set in Q1 2020.

"Tokyo's premium space is now commanding its highest rents in nearly two decades," CBRE said, noting that competition for top-tier buildings in central wards remains fierce.

Osaka and Nagoya Set New Records

In Osaka, vacancies slipped 0.3 points to 2.3% as existing buildings filled steadily. Average all-grade rents climbed 1.4% to roughly $400 per tsubo--an all-time high. Grade A landlords in both the Umeda district and secondary areas implemented across-the-board increases.

Nagoya also saw record highs, with the all-grade vacancy rate dropping 0.7 points to 2.4%, its lowest since mid-2021. Grade A rents rose 1.4% to about $765, while all-grade rents gained 0.8% to $390, the highest levels since CBRE began its survey.

Market Outlook

CBRE said Japan's office markets continue to demonstrate "remarkable stability," supported by solid tenant demand, limited speculative construction, and expansion-driven relocations. While new supply in some secondary cities may briefly lift vacancies, overall fundamentals remain robust heading into 2026, particularly in Tokyo and other major metropolitan hubs.