Residential Real Estate News

U.S. Housing Market Stalls as Iran War Pushes Rates Up Four Straight Weeks

The long-anticipated rebound in the U.S. housing market is losing momentum, as a fresh uptick in borrowing costs and escalating geopolitical tensions inject new uncertainty into an already fragile recovery.

After entering 2026 with cautious optimism, economists had projected a modest revival in home sales, driven by easing mortgage rates and a gradual increase in housing supply. Instead, renewed volatility--linked in part to a widening conflict involving the U.S., Israel, and Iran--has pushed financial markets back into a defensive posture, lifting Treasury yields and, by extension, mortgage rates.

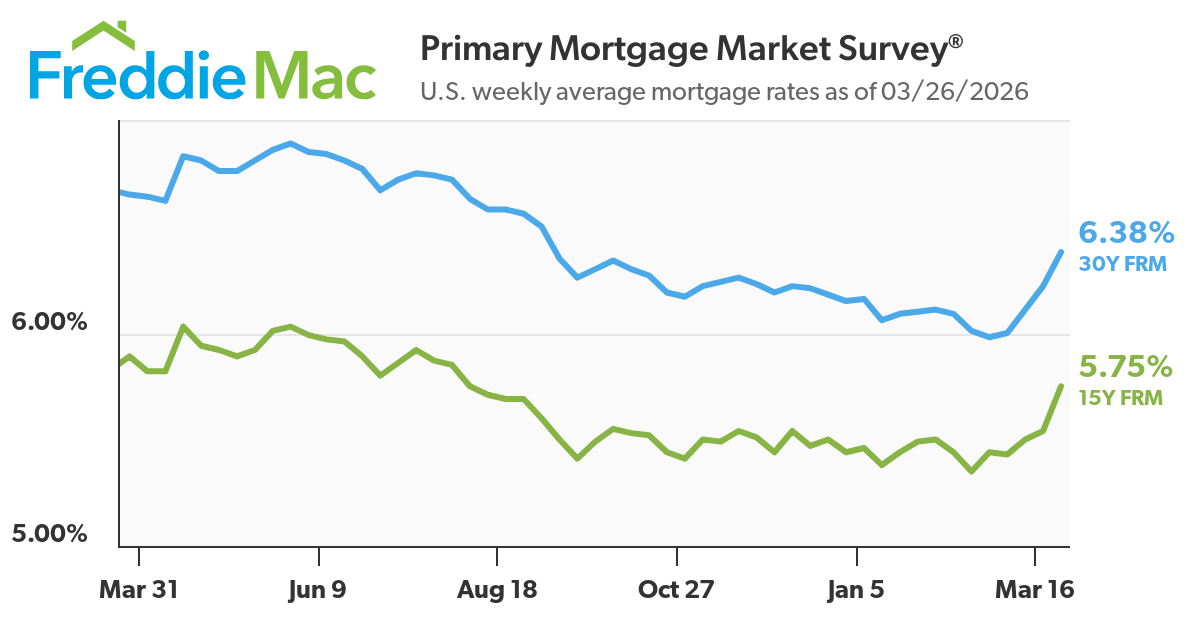

Data released Thursday by Freddie Mac showed the average rate on a 30-year fixed mortgage climbed to 6.38% for the week ending March 26, 2026, marking a fourth consecutive weekly increase. The benchmark rate stood at 6.22% a week earlier and 6.65% during the same period last year.

"Mortgage rates continue to experience volatility, but the broader housing market is showing incremental improvement compared with a year ago," said Sam Khater. He noted that both purchase and refinance applications have risen on a year-over-year basis, suggesting underlying demand remains intact despite affordability pressures.

Shorter-term borrowing costs are also moving higher. The average rate on a 15-year fixed mortgage rose to 5.75%, up from 5.54% the prior week, though still below the 5.89% level seen a year earlier.

The recent climb in mortgage rates reflects movements in the U.S. Treasury market, where the 10-year yield--closely tracked by home loan rates--hovered around 4.38% on Thursday. While the Federal Reserve does not directly set mortgage rates, its policy stance, along with inflation expectations and global risk dynamics, continues to shape borrowing costs.

Those dynamics are proving especially consequential for housing. Elevated rates, combined with still-high home prices, are keeping affordability near multi-decade lows, limiting the pool of qualified buyers. The result is a market caught between improving demand fundamentals and financial constraints that continue to suppress transaction volumes.

Following a year in which home sales dropped to their lowest level in three decades, industry participants had hoped 2026 would mark a turning point. Instead, the path to recovery is becoming increasingly uneven--dependent not only on domestic monetary policy but also on geopolitical developments far beyond the housing sector.