The WPJ

Commercial Real Estate News

Top 10 Most Expensive Office Markets in the World Revealed

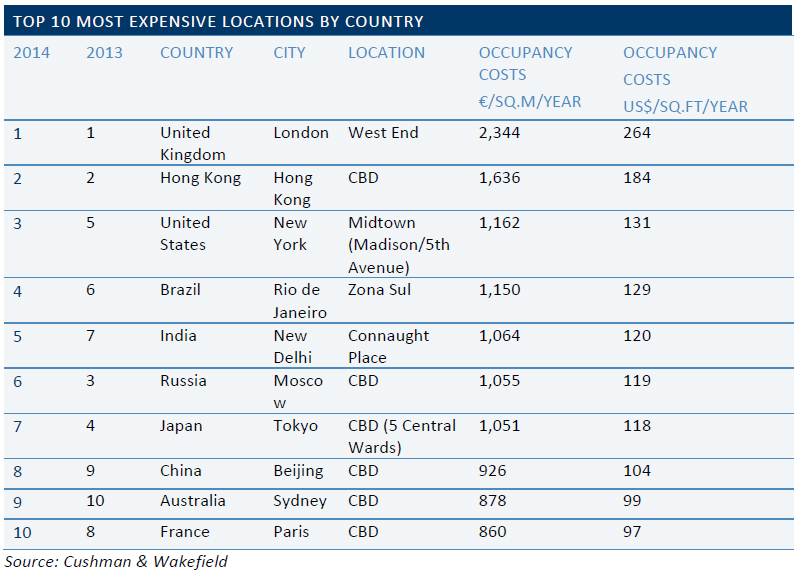

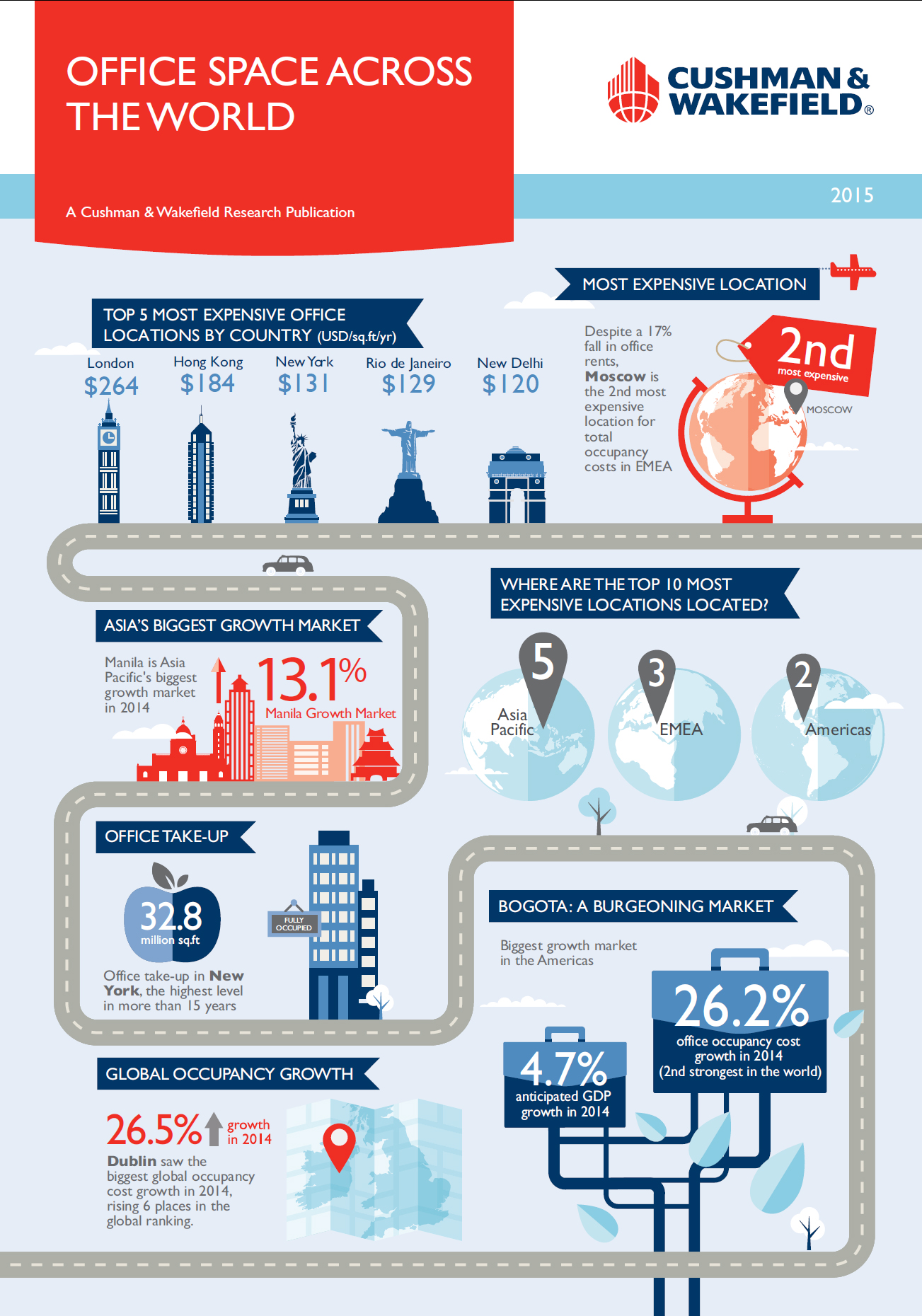

London's West End is the world's most expensive office market for the third consecutive year, retaining its title ahead of runner-up Hong Kong, according to research published today in Cushman & Wakefield's annual Office Space Across the World global rankings.

Prime rents in London's West End have risen 4.6% over the year but are still 13% behind the 2007 peak. However, further positive rental growth is anticipated against a backdrop of limited supply and expected development completions in 2015.

- London confirms its position as the world's most expensive office market for the third consecutive year

- Hong Kong ranks second for the second year in a row

- New York rounds out the top three, moving up two places

- Global rents rose 7% over the 12 months to December 2014

Cushman & Wakefield's head of London markets, George Roberts, said, "With a true global appeal, London continues to attract major international businesses looking to be based there, often using it as a springboard into Europe. As economic conditions in the UK further outperform, there will be heightened demand for London office space in 2015 from across all sectors. With supply heading downwards, further rental growth is expected."

Global office rents rose 7% in 2014, more than double the circa 3% annual compound increase since 2010. Overall, last year saw foundation cities from around the world reaffirm their position in the global hierarchy at the expense of smaller, peripheral markets.

Challenges remain for occupiers, not just in terms of property fundamentals, but also geopolitical risks which some are viewing with understandable caution. These factors are being leveraged by some occupiers to negotiate more flexible lease terms or lower rents, particularly in locations with oversupply.

REGIONAL RANKING: EMEA

Cushman & Wakefield's head of EMEA offices, James Young, said, "A key theme of the European office market is the low level of development delivered over the last two years. Despite a recent uptick in construction activity, the revival is supply-led as occupiers continue to search for quality space that provides the right environment for staff in a highly competitive employment market."

However, there is some divergence in under-supplied markets such as London - in order to secure space some occupiers are moving sooner than expected to secure the larger, more flexible floor plates they need. As quality availability erodes, secondary space is becoming a more realistic option for some and while rents here have been reasonably static an upward swing is expected over the next 12 months.

Further to London cementing itself as a true gateway city at the top of the global ranking, Moscow places second on an EMEA-specific basis, despite seeing a 17% decline in prime rents linked to impose sanctions after the annexation of Crimea and the ongoing civil unrest with Ukraine.

Paris rounds out the top three in EMEA, but also saw rents decline by -6.3% and occupancy costs by -3.9% over the year. Dublin tops the table for the highest percentage growth in 2014, rising six places to 19th position in the global ranking. Meanwhile, Dubai and Doha recorded rises in occupancy costs and jumping four and three places to become the 11th and 13th most expensive cities in the world for offices respectively.

REGIONAL RANKING: ASIA PACIFIC

John Siu, managing director of Cushman & Wakefield in Hong Kong, said: "Leasing activity across Asia Pacific continues to strengthen but to a varying degree. With pent-up demand in some of the core locations and service sector growth positive, 2015 is expected to see further rental growth in most of the gateway cities of the region."

The majority of core markets are seeing vacancy rates below 7% and will therefore be able to sustain some new development as well as maintain rental values. There are however a few exceptions to this: namely certain second tier Chinese cities and key Australian cities where existing supply plus new construction will put pressure on rental growth.

Beyond Hong Kong's second position in the global ranking, New Delhi's Connaught Place is the next highest placed district in Asia Pacific, followed by Tokyo in third. Beijing maintains a solid fourth place in the regional ranking. Manila recorded the largest increase in occupancy costs in the Asia Pacific region with strong growth in outsourcing and offshoring services expected to sustain office demand going forward.

While growth in China is well beyond that of most other global countries, it is slowing and this is weighing in on domestic demand. Beijing is the highest performing Chinese city, maintaining its fourth place in the regional ranking despite a fall in rents over the year.

REGIONAL RANKING: THE AMERICAS

Ron Lo Russo, president, New York tri-state region, Cushman & Wakefield, said: "The accelerating US economic recovery is quickly propelling the Manhattan office market beyond equilibrium in favor of landlords, resulting in falls in the amount of quality space available which should lead to solid rental increases in 2015."

New York's Manhattan (Midtown: Madison/5th Avenue) secures the top spot in the region, followed by Rio de Janeiro and São Paolo in Brazil. There was no movement in the top three cities in 2014, which are consistent with those seen in 2013.

New York City continued to record healthy employment growth and as it has been throughout the recovery, much of the growth in office-using jobs has been in the technology, advertising, media and information industries.

Occupier activity in New York City was powered by large deals with total take-up reaching a staggering 32.8 million sq ft in 2014 - the highest level in more than 15 years. Activity was bolstered by the return of the 'mega-deal', as 28 new deals in excess of 100,000 sq ft were completed, while robust leasing activity pushed vacancy rates to single digits for first time since July 2012.

Houston is a noteworthy market, given its exposure to the oil sector that has seen barrel prices plummet over the last few months. This did not impact rents in 2014 but the effect is expected to be seen in 2015 as companies take a strategic approach on how quickly the recovery will come and what it will look like. Demand for new office space is expected to slow as is the rate of new construction. However, job growth is expected to take place in Houston but just not at the rate of previous years and the current economic situation is expected to be more of a temporary 'pause' than a 'standstill'.

Real Estate Listings Showcase

{kind=link}

{kind=link}

This website uses cookies to improve user experience. By using our website you consent in accordance with our Cookie Policy. Read More